The latest issue of ‘The Globe’, Eurizon’s publication describing the Company’s investment view. In this issue, a focus is dedicated to “at what point is the revision of consensus?”

Scenario

The overall picture is marred by a complex intertwining of themes that act restrictively on the global economy.

US inflation has probably peaked, but the decline will be slow and non-linear, as proven by April data, still stronger than expected. Price tensions will also be kept in place by the new lockdowns enforced in China and by persistently high commodity prices due to the war.

Q1 2022 hedge fund letters, conferences and more

In May, the Federal Reserve hiked rates by 50bps, announcing its intention to do the same at its June and July meetings. Fed Funds futures are pricing in a peak of near-term rates at 3% in a year’s time. For what concerns the ECB, the market is pricing in a start to the rate hike cycle between June and July, with expectations for higher rates by 120bps in total in the next year.

Economic data, in the US as also in Europe, confirm that the recovery is on track, still supported by post-Covidreopenings, although the tightening of monetary conditions observed over the past few weeks will probably start to become visible in data between the spring and the summer.

Despite the indications of a macroeconomic slowdown, however, investors could find reassurance in confirmation of the inflation peak being overcome, in the drop of commodity prices, or in the easing of the wave of Covidinfections in China.

Macro Economy

- US inflation may have hit a peak, but the new lockdowns in China and high commodity prices are hindering its decline.

- The Fed hiked rates by 50bps in May and plans to do the same in June and July. The markets are pricing in a Fed Funds rate of 3.0% in a year’s time. The initial rate hike by the ECB is forecast in July.

Asset Allocation

- Rising US rates, still high commodity prices, and the new lockdowns in China, imply risks of a slowdown of the global economy.

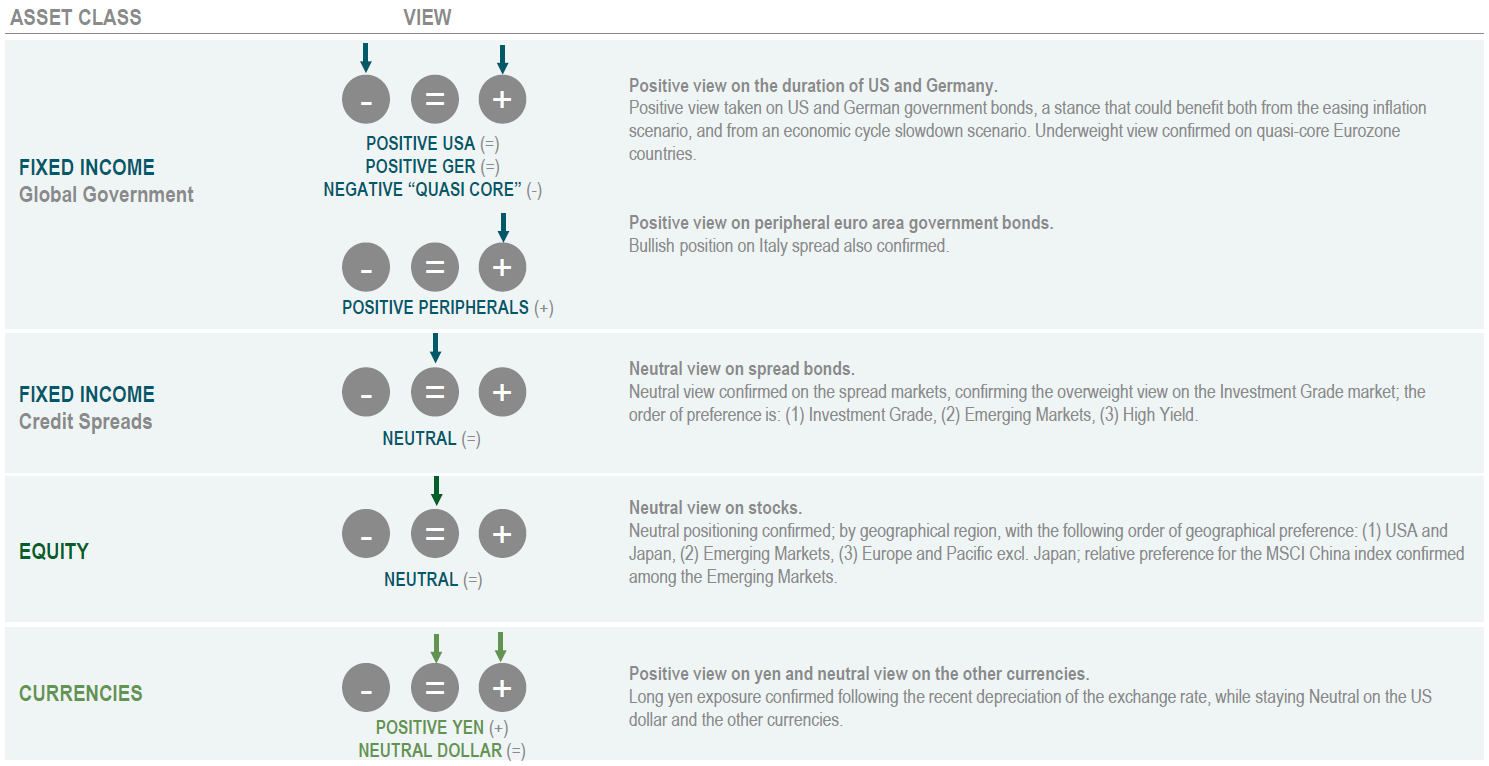

- Portfolio exposure stepped up to US and German government bonds, while confirming a neutral view on stocks and on the other risk assets.

Fixed Income

- Positions increased on US and German bonds, that could benefit both from easing inflation and from the slowdown of economic growth.

- Spread bonds hold greater appeal than core government bonds; portfolio positions taken on Investment Grade issues confirmed, while the picture remains uncertain for High Yield and Emerging country bonds.

Equity

- Stock market valuations have dropped to historically appealing levels, although earnings could be revised down in case of a macro slowdown.

- At the geographical level, Europe could continue to be affected by tensions stemming from the war between Russia and Ukraine. Among the major markets, the US and Japan seem to be better positioned.

Currencies

- The US dollar seems to have largely priced in the Fed’s policy reversal and could put on hold the upswing observed since the beginning of 2021.

- Long yen positions confirmed.

Investment View

The baseline scenario is marred by persistently high commodity prices and the Fed’s policy tightening, a combination that creates uncertainty on the length of the economic cycle. Duration positions have been stepped up, confirming a neutral view on risk assets.

Asset Classes Compared

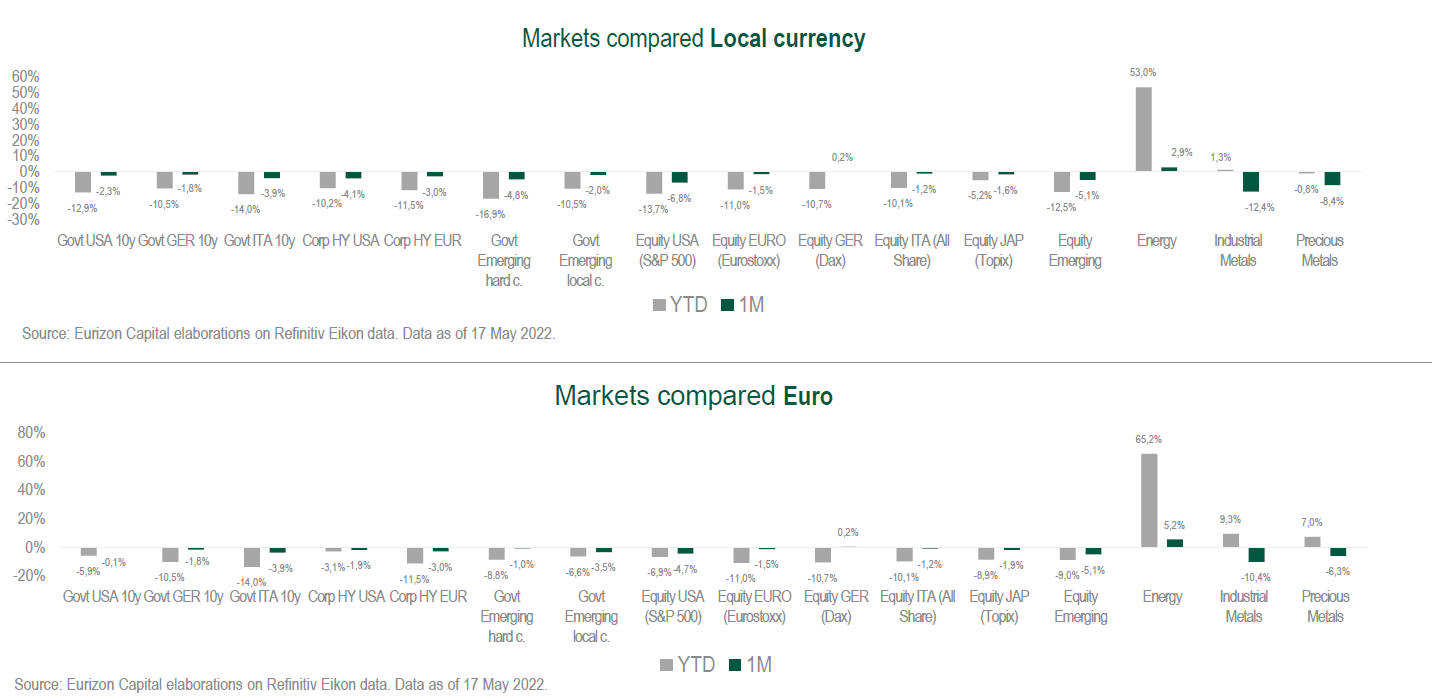

Government rates dipping back down after rising swiftly in March and April, reflecting the concerns over global growth that havebeen affecting the stock markets since the beginning of the year. Spreads widening, especially on the credit markets. Widespread strengthening of the dollar, to 1.04 against the euro.

Theme Of The Month: At What Point Is The Revision Of Consensus?

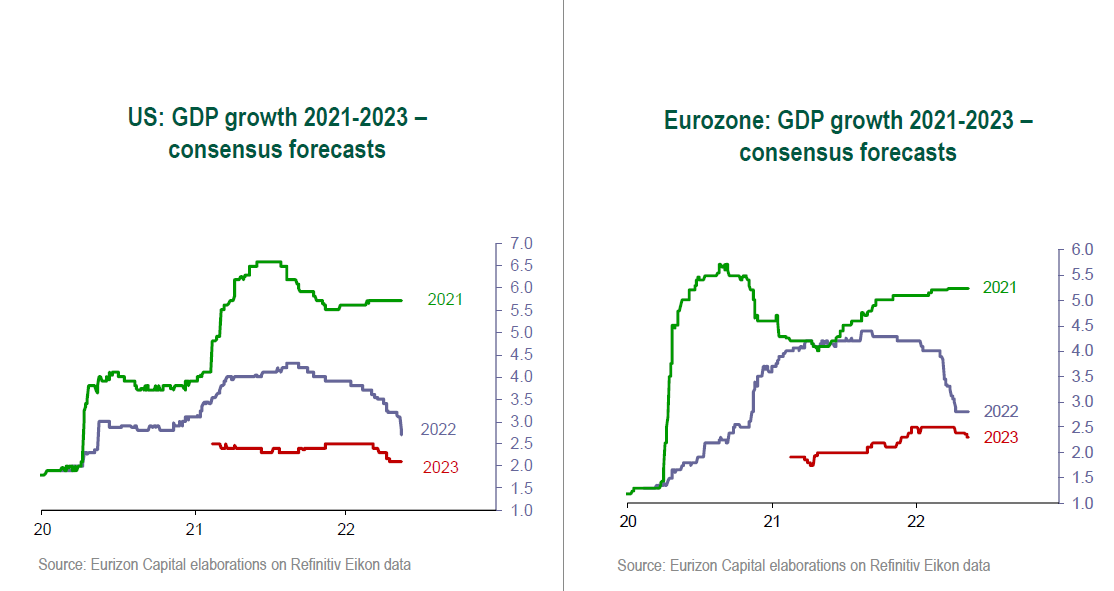

- Twenty-twenty-two was meant to be an orderly transition year from the growth peak hit in 2021 to a return to normal in 2023. While the transition phase is confirmed, it is proving turbulent. The inflation flare-up, that lasted longer than expected, forced the Central Banks to swiftly reverse their courses, leading economists to revise down their growth forecasts.

- In the US, after 5.7% growth last year, the consensus forecast for 2022 is now 2.7%, down from 3.9% at the beginning of the year. Eurozone growth has been revised in much the same was as for the US: growth in 2021 was 5.4% and the forecast for 2022 has been lowered, since the beginning of the year, from 4.2% to 2.8%.

- The revisions are already rather incisive and point for the remainder of the year to a slowdown in the pace of growth, but not a recession. Lastly, it should be said that forecasts for 2023 have been little affected by the current slowdown. Consensus is still firm on the prospect of growth finally reach a cruising speed of around 2% in 2023, after a very turbulent three years.

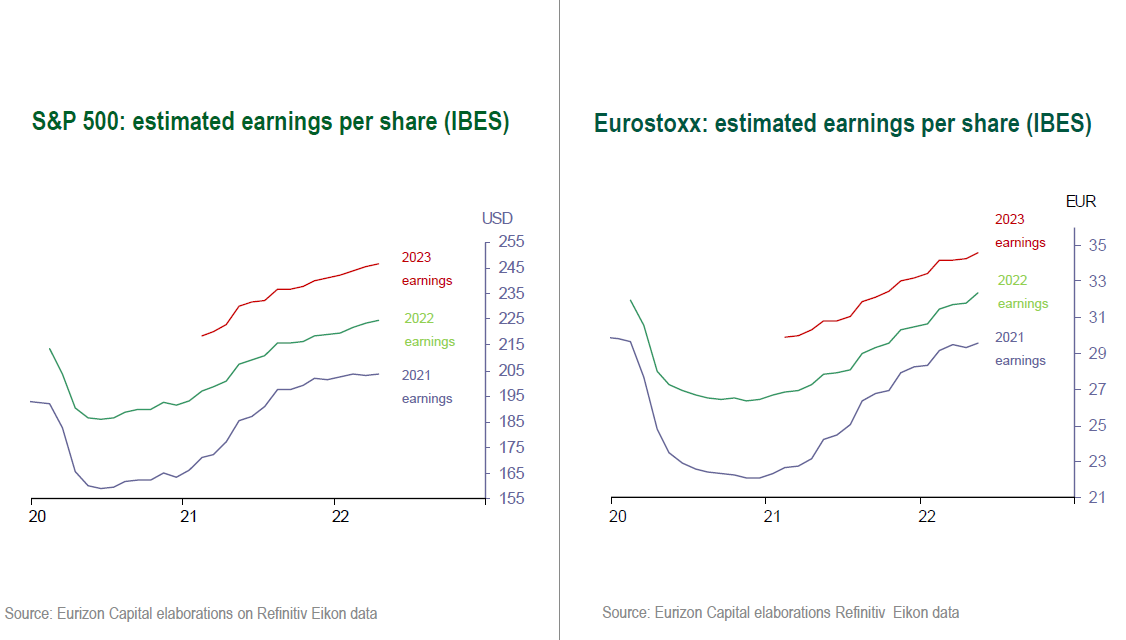

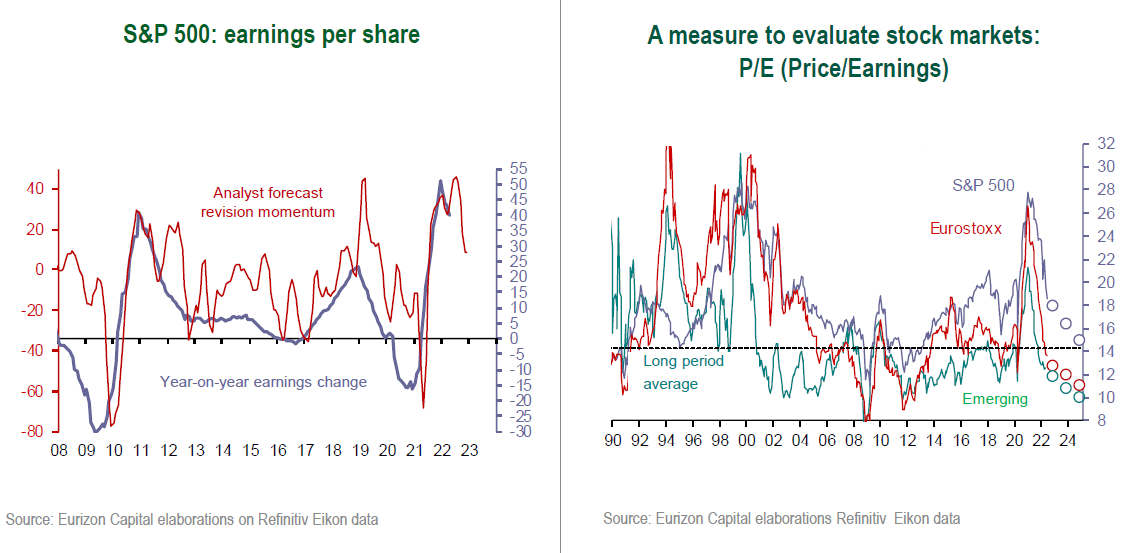

- While substantially lowering economic growth forecasts, consensus has on the other hand continued to revise up its expectations for corporate earnings, both in the US and in Europe.

- S&P 500 earnings growth in 2022 is forecast at 10%, up from around 8.5% at the beginning of the year. On the Eurostoxx index, profits are forecast to increase by 8.5% in 2022, from 8.2% at the beginning of the year. Estimates for 2023 are essentially stable: earnings are forecast to grow by +10% in the US, and by +8% in the Eurozone.

- The discrepancy between macro consensus (economic growth) and micro consensus (corporate earnings) maybe explained by the high level of inflation. Among the different economic agents, businesses are the best equipped to live with a high level of inflation; in fact, in some ways they fuel the inflation trend themselves, transferring to the final consumer upstream price increases.

- Obviously, the safeguarding of high profitability rates cannot continue for ever.If in the next few months the slowdown of economic activity continues, potentially coming close to a recession, a revision of 2022 and 2023 earnings would be inevitable and, in all likeliness, substantial.

- In actual fact, on the earnings front as well, consensus is already turning more conservative. While it is true that in absolute terms earnings forecasts have not come down, it is also true that analysts have already started to “ease back”. Estimates revisions are in fact decelerating, anticipating a forthcoming slowdown in profit growth.

- The real adjustment at the market level lies with multiples. While earnings continued to rise, market indices dropped (MSCI All Country index -15% since the beginning of the year).

- For the Eurozone and the Emerging Markets, P/E ratios have dropped below their long-term averages and are not too far off recessionary levels. The US stock market’s multiples, on the other hand, are stronger, although they have been declining at a faster rate of late.

- In a theoretic qualitative ranking perspective, macro consensus is at a rather advanced stage in envisaging a slowdown, while corporate earnings are lagging well behind.If macro forecasts are lowered further (as could be the case if inflation does not decline and the pace of rate hikes does not slow), corporate earnings will head for a downward revision phase. The impact on stock quotations, however, could be at least in part be buffered by valuations already sharply revised in a conservative sense.