Dear fellow investors,

Q3 2021 hedge fund letters, conferences and more

The Energy Bandwagon

In 2014, famed UK stock picker Terry Smith wrote a piece, titled Shale: Miracle, Revolution or Bandwagon?, in most ways mocking investors excitement in the oil and gas business in the United States of America. In his writing, Monsieur Smith highlights some of the negatives of the oil and gas business like the amount of energy needed to extract the energy, depletion of reserves in wells, and lastly, investor returns. We love his writing because for that time period, he was right. The most sensitive issue an investor should have been focusing on then was the last point: investor returns.

To Smith’s first two points, using energy to produce energy is just physics. There is no way around it. It’s just like sending electricity across lines. You’ll lose 15% of the electricity in long-range transportation. This certainly shouldn’t stop you from wanting to transmit electricity over long distances. These transmission lines provide a dynamic, deep market for consumers and businesses. When it comes to his other point on depletion, this is yet again a natural process for oil and gas. We have become smarter in pad drilling and fracking to get after more oil and gas in particular geographies. The issue then wasn’t the natural depletion. It was the cash flow that would come in the years ahead with that depletion. This points back to Smith’s later point of investor returns.

We were in complete agreement with Smith at that time. Smith finished his piece in the Financial Times saying, “As the late Jimmy Goldsmith was fond of saying: ‘If you see a bandwagon, it’s too late.’ The shale bandwagon may have already passed.” To his point on investor returns, they weren’t there and weren’t going to be there for a while. The cash flows were being pushed at more marginal wells, not the cash cows.

As Buffett has said a multitude of times, “price is what you pay, value is what you get.” In 2014, you didn’t get much value at those prices as the bandwagon was long and very noticeable. Fast forward to 2021, the bandwagon of other energy forms is very noticeable. There are practically religious orders being built up in other forms of energy like solar and other renewables. Are these other forms of energy subject to the laws of economics? Yes. They may end up with the same victim mentality that energy investors in 2014 did.

We are by nature very skeptical of Wall Street and the ideas it peddles. This is because you should always be skeptical of someone selling something that has an incentive attached, particularly when you don’t have similar incentives. Physicist Mark Mills pushed back strongly in his 2019 piece titled The “New Energy Economy”: An Exercise in Magical Thinking. Mills stated in 2019, when speaking about shale versus wind, “The fundamental differences between these energy resources can also be illustrated in terms of individual equipment. For the cost to drill a single shale well, one can build two 500-foot-high, 2-megawatt (MW) wind turbines. Those two wind turbines produce a combined output averaging over the years to the energy equivalent of 0.7 barrels of oil per hour. The same money spent on a single shale rig produces 10 barrels of oil, per hour, or its energy equivalent in natural gas, averaged over the decades.” Mills is pointing out some of the pure physics of this discussion. As George Gilder points out, “time is money.” These resources have vastly different costs in time, thus price. Isn’t it odd this doesn’t stop the bankers from creating a magical story for the bandwagon?

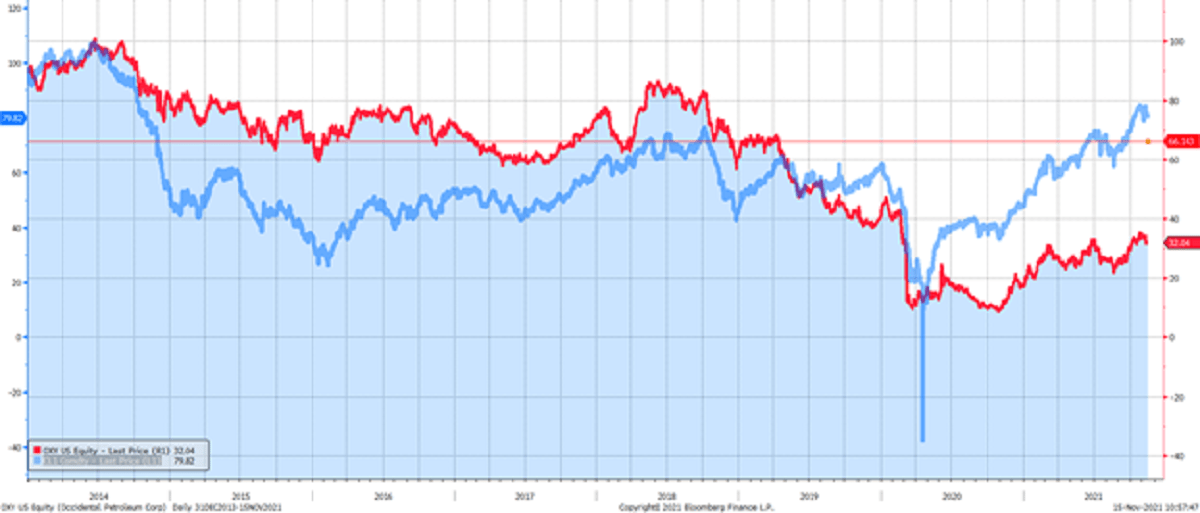

Spot Oil Prices vs Occidental Petroleum

Why would so many people not be aware of the time limitations or why would many investors not care that per pound (mass) hydrocarbons are the most efficient, acceptable (non-nuclear) energy source in the world? It’s because the bandwagon is out there on renewable energy, just as it was in 2014 with shale. In Newton’s third law, for every action there is an equal and opposite reaction. The equal reaction to today’s renewable revolution is that people have immense confidence in its future and that reflects in price. The opposite reaction is that hydrocarbons are left for dead and the price is very low. Below is a chart comparing spot oil prices to Occidental Petroleum Corporation (NYSE:OXY), since 2014.

Investors used to pay $60-$80 per share for Occidental Petroleum at today’s spot WTI price and this was prior to them owning Anadarko Petroleum. This acquisition gave them 30% more production. Our minds spin at the thought of this. While the bandwagon comes and goes in renewables (non-hydrocarbons), we will wait for our investors’ day in the sun with Occidental Petroleum (OXY US), Continental Resources, Inc. (NYSE:CLR), ConocoPhillips (NYSE:COP) and Chevron Corporation (NYSE:CVX). The bandwagon being nowhere near us today makes us very excited for the value we get at today’s prices. To bring it back to Terry Smith, he was right in 2014. Our investors owned zero in energy stocks then, like Terry. Now, he should be elated that the bandwagon is not in the oil and gas business. However, he isn’t buying energy stocks because his discipline doesn’t allow him to own these types of businesses. Between investors unwilling to own these companies (the bandwagon) and the magical banking that these investors have been sold, we are thankful for our investors. Newton’s third law and George Gilder’s principles just reinforce the truth.

Fear stock market failure,

Cole Smead, CFA

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Cole Smead, CFA, President and Portfolio Manager, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2021 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.