DCF Myth 3.1: The Margin of Safety – Tool for Action or Excuse for Inaction?

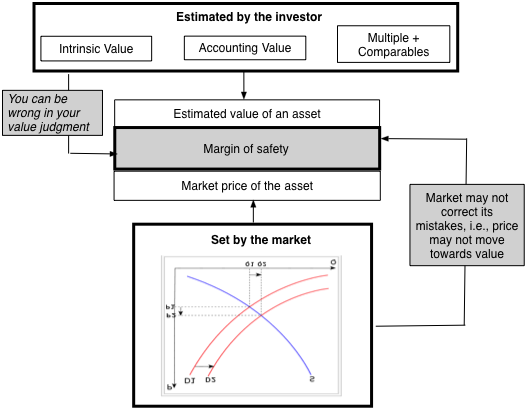

- Valuation Basis: While MOS is often defined it as the difference between value and price, the way in which investors estimate value varies widely. The first approach is intrinsic value, either in its dividend discount model format or a more expansive DCF version. The second approach estimates value from accounting balance sheets, using either unadjusted book value or variants thereof (tangible book value, for instance). The third approach is to use a pricing multiple (PE, EV to EBITDA), in conjunction with peer group pricing, toestimate “a fair price” for the company. While I would contest even calling this number a value, it is still used by many investors as their estimated value.

- Magnitude and Variability: Among investors who use MOS in investing, there seems to be no consensus on what constitutes a sufficient margin. Even among investors who are explicit about their MOS, the follow up question becomes whether it should be a constant (say 15% for all investments) or whether it should be greater for some investments (say in risky sectors or growth stocks) than for others (utilities or MLPs).

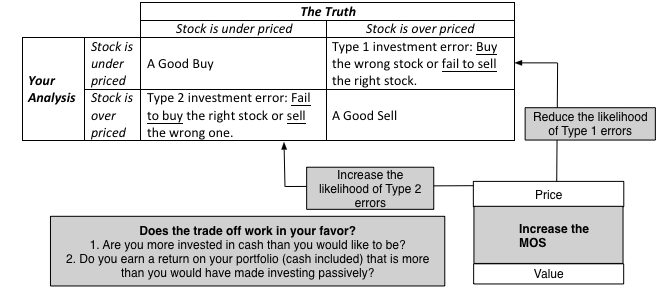

Many risk averse value investors would accept this trade off but there is a cost to being too conservative and if that cost exceeds the benefits of being careful in your investment choice, it will show up as sub-par returns on your portfolio over extended periods. So, will using a MOS yield a positive or negative payoff? I cannot answer that question for you, because each investor has to make his or her own judgment on the question, but there are simple tests that you can run on your own portfolios that will lead you to the truth (though you may not want to see it). If you find yourself consistently holding more of your overall portfolio in cash than your natural risk aversion and liquidity needs would lead you to, and/or you don’t generate enough returns on your portfolio to beat what you would have earned investing passively (in index funds, for instance), your investment process, no matter what its pedigree, is generating net costs for you. The problems may be in any of the three steps in the process: your valuations may be badly off, your judgment on market catalysts can be wrong or you may be using too large a MOS.

Value investors who spend all of their time coming up with the right MOS and little on valuation are doing themselves a disservice. If your valuations are incomplete, badly done or biased, having a MOS on that value will provide little protection and can only hurt you in the investment process (since you are creating type 2 errors, without the benefit of reducing type 1 errors). Given a choice between an investor with high quality valuations and no/little MOS and one with poorly done valuations and a sophisticated MOS, I would take the former over the latter every single time.

[drizzle]I am also uncomfortable with investors who start with conservative estimates of value and then apply the MOS to that conservative value. In intrinsic valuation, conservative values will usually mean haircutting cash flows below expectations, using high discount rates and not counting in growth that is uncertain. In asset-based valuation, it can take the form of counting only some of the assets because they are tangible, liquid or both. Remember that you are already double counting risk, when you use MOS, even if your valuation is a fair value (and not a conservative estimate of value), because that value is computed on a risk-adjusted basis. If you are using a conservative value estimate, you may be triple or even quadruple counting the same risk when making investment decisions. If you are using this process, I am amazed that any investment manages to make it through your risk gauntlets to emerge as a good investment, and it does not surprise me that nothing in the market looks cheap to you.

I know that those who use MOS are skeptics when it comes to modern portfolio theory, but modern portfolio theory is built on the law of large numbers, and that law is robust. Put simply, you can aggregate a large number of risky investments to create a relatively safe portfolio, as long as the risks in the individual stocks are not perfectly correlated. In MOS terms, this would mean that an investor with a concentrated portfolio (who invests in three, four or five stocks) would need a much larger MOS on individual investments than one who spreads his or her bets across more investments, sectors and markets.

Expanding on this point, using a MOS will create biases in your portfolio. Using the MOS to pick investment will then lead you away from investments that are more exposed to firm-specific risks, which loom large on an individual company basis but fade in your portfolio. Thus, biotechnology firms (where the primary risk lies in an FDA approval process) will never make your MOS cut, but food processing firms will, for all the wrong reasons. In the same vein, Valeant and Volkswagen will not make your MOS cut, even though the risk you face on either stock will be lowered if they are parts of larger portfolios.

I know that many investors abhor betas, and believe it or not, I understand. In fact, I have long argued that there are replacements available for portfolio theory-based risk measures and that not only is intrinsic value robust enough to work with these alternative risk measures but that the discount rate is not (and should not) be the ultimate driver of value in most companies. That said, there are some in the value investing community who like to use their dislike of betas as a bludgeon against all financial theory and after they have beaten that straw horse to death, they will offer MOS as their alternative risk measure. That suggests a fundamental misunderstanding of MOS. To use MOS, you need an estimate a value and I am not aware of any intrinsic value model that does not require a risk adjustment to get to value. In other words, MOS is not an alternative to any existing risk measure used in valuation but an add-on, a way in which risk averse investors can add a second layer of risk protection.

There is one possible way in which the MOS may be your primary risk adjustment mechanism and that is if you use a constant discount rate when doing valuation (a cost of capital of 8% for all companies or even a risk free rate) and then apply a MOS to that valuation to capture risk. If that is your approach, you should definitely be using different MOS for different investments (see Myth 3), with a larger MOS being used on riskier investments. I would also be curious about how exactly you make this MOS adjustment for risk, including what risks you bring in and how you make the conversion.

- Self examination: Even if you believe that MOS is a good way of picking investments, it is not for everyone. Before you adopt it, you have to assess not only your own standing (including how much you have to invest, how risk averse you are) but also your faith (in your valuation prowess and that markets correct their mistakes). Once you have adopted it, you still need the effects it has on your portfolio, including how often you choose not to invest (and hold cash instead) and whether it makes a material difference to the returns you generate on your portfolio.

- Sound Value Judgments: As I noted in the last section, a MOS is useful only if it is an addendum to sound valuations. This may be a reflection of my biases but I believe that this requires intrinsic valuation, though I am willing to concede that there are multiple ways of doing it right. Accounting valuations seem to be built on the twin presumptions that book value is an approximation of liquidation value and that accounting fair value actually means what it says, and I have little faith in either. As for passing of pricing as value, it strikes me as inconsistent to use the market to get your pricing number (by using multiples and comparable firms) and then argue that the same market misprices the asset in question.

- A Flexible MOS: Tailor the MOS to the investment that you are looking at: There are two reasons for using a MOS in the first place. The first is an acceptance that, no matter how hard you try, your estimate of value can be wrong and the second is that even if the value estimate is right, there is uncertainty about whether the market will correct its mistakes over your time horizon. If you buy into these two reasons, it follows that your MOS should vary across investments, with the following determinants.

- Valuation Uncertainty: The more uncertain you are about your estimated value for an asset, other things remaining equal, the larger the MOS should be. Thus, you should use a smaller MOS when investing in mature businesses and during stable markets, than when putting your money in young, riskier business or in markets in crises.

- Portfolio Tailoring: The MOS that you use should also be tailored to your portfolio choices. If you are a concentrated investor, who invests in a four or five companies, you should use a much higher MOS than an investor who has a more diversified portfolio, and if you the latter, perhaps even modify the MOS to be larger for companies that are exposed to macroeconomic risks (interest rates, inflation, commodity prices or economic cycles) than to company-specific risks (regulatory approval, legal jeopardy, management flux).

- Market Efficiency: I know that these are fighting words to an active investor, red flags that call forth intemperate responses. The truth, though, is that even the most rabid critics of market efficiency ultimately believe in their own versions of market efficiency, since if markets never corrected their mistakes, you would never make money of even your canniest investments. Consequently, you should settle for a smaller MOS when investing in stocks in markets that you perceive to be more liquid and efficient than in assets, where the corrections will presumably happen more quickly than in inefficient, illiquid markets where the wait can be longer.

- Pricing Catalysts: Since you make money from the price adjusting to value, the presence of catalysts that can lead to this adjustment will allow you to settle for a lower MOS. Thus, if you believe that a stock has been mispriced ahead of an earnings report, a regulatory finding or a legal judgment, you should demand a lower MOS than when you invest in a stock that you believe is misvalued but with no obvious pricing catalyst in sight.

Finally, if MOS is good enough to use when you buy a stock, it should be good enough to use when you sell that stock. Thus, if you need a stock to be under valued by at least 15%, to buy it, should you also not wait until it is at least 15% over valued, to sell it? This will require you to abandon another nostrum of value investing, which is that once you buy a great company, you should hold it forever, but that is not just unwise but is inconsistent with true value investing.

Would I prefer to buy a stock at a 50% discount on value rather than at just below fair value? Of course, and I would be even happier if you made that a 75% discount. Would I feel even more comfortable if you estimated value very conservatively. Yes and I would be delighted if all you counted was liquid assets. That said, I don’t live in a world where I see too many of these investments and when I do, it is usually the front for a scam rather than a legitimate bargain. That is the reason that I have never formally used a MOS in investing. I did buy Valeant at $32, because my valuation of the stock yielded $45 for the company. Would I have still bought the stock, if my value estimate had been only $35 or if it was a big chunk of my portfolio? Perhaps not, but I have bought stocks that were priced at my estimated fair value and have held back on investments that I have found to be under valued by 25% or more. Why? That has to wait for my coming post on simulations, since this one has run its course.

YouTube Video

Uncertainty Posts

- DCF Myth 3: You cannot do a valuation, when there is too much uncertainty

- The Margin of Safety: Excuse for Inaction or Tool for Action?

- Facing up to Uncertainty: Probabilities and Simulations

DCF Myth Posts

Introductory Post: DCF Valuations: Academic Exercise, Sales Pitch or Investor Tool

- If you have a D(discount rate) and a CF (cash flow), you have a DCF.

- A DCF is an exercise in modeling & number crunching.

- You cannot do a DCF when there is too much uncertainty.

- The most critical input in a DCF is the discount rate and if you don’t believe in modern portfolio theory (or beta), you cannot use a DCF.

- If most of your value in a DCF comes from the terminal value, there is something wrong with your DCF.

- A DCF requires too many assumptions and can be manipulated to yield any value you want.

- A DCF cannot value brand name or other intangibles.

- A DCF yields a conservative estimate of value.

- If your DCF value changes significantly over time, there is either something wrong with your valuation.

- A DCF is an academic exercise.