Broyhill Asset Management’s commentary for the fourth quarter ended December 2020, discussing their new position in Equity Commonwealth.

[soros]Q4 2020 hedge fund letters, conferences and more

For the year ending December 31, 2020, Broyhill generated positive returns that varied widely depending on individual account asset allocations, legacy positions, and capital flows. Detailed quarterly reports, including account and benchmark performance, portfolio holdings, and transaction history, have been posted to our investor portal.

While 2020 was a year most of us would like to forget, given the circumstances, we have much to be thankful for. We are thankful that we didn’t lose any loved ones. We are thankful for the opportunity to step back and reconsider what’s important. And we are thankful for the incredible resilience and resolve demonstrated by our friends and families. We hope some of these lessons stay with us as we get back to business as usual. And we hope other aspects are not revisited for a very long time. COVID took a toll on all of us. We are fortunate that we survived and pleased that we made some money for investors along the way. Your support throughout such a challenging year was a key factor in helping us navigate through the crisis with a rational, long-term perspective.

All that being said, we are glad to put the year behind us. Looking back on our performance, I’d say that we earned a passing grade, but certainly nothing to write home about. This was precisely the type of year where Broyhill should shine. Volatility was extraordinary. Return dispersion was exceptional within and across asset classes. The market dropped into bear market territory faster than ever before and recovered to new highs in record time. This extreme volatility and dispersion provided investors with plenty of opportunity to generate large profits. We managed risk well during the first quarter, capturing only a fraction of the market’s downside. We capitalized on early dislocations and benefitted from the initial recovery. But we reduced many of these investments too soon and failed to participate in the final stages of the market’s euphoria.

Our largest contributors for the second half were investments in LatAm Airports, Anheuser Busch InBev, and Dollar Tree Stores. There were no material detractors from performance. Portfolio turnover remained high. We liquidated positions in Sysco (SYY), Five Below (FIVE), and Bookings (BKNG), as shares approached our estimates of intrinsic value despite ongoing economic challenges. We established a new core position in Equity Commonwealth (EQC) during the second half (discussed below) and began accumulating positions in two additional companies, which we’ve continued buying into the first quarter. At year-end, our top five holdings in alphabetical order, which made up the majority of our invested capital, were Altria (MO), Anheuser-Busch InBev (BUD), Dollar Tree (DLTR), Equity Commonwealth (EQC), and McKesson (MCK).

Am I Being Too Subtle?

“Business is easy. If you’ve got low downside and big upside, you do it. If you’ve got big downside and small upside, you run away.” – Sam Zell

Simple enough. But simple and easy are two very different things. The average investor finds it almost impossible to run away from rising asset prices as expected returns diminish. Fortunately for us, Sam Zell is not “average” by any definition of the word. Zell is a self-made billionaire who earned the nickname “The Grave Dancer” from his highly profitable purchases of distressed assets in the aftermath of the 1970s’ commercial real estate crash.1

Zell showed his willingness to “run away” from big downside risk when he sold Equity Office Properties (EOP) to Blackstone for $39 billion at the peak of the housing market in 2007. That capped a two-decade run since EOP’s 1997 IPO, which generated a ~ 15% compound annual return on capital, almost three times better than the S&P 500 index over the same period.

Equity Commonwealth

Since installing his management team at Equity Commonwealth (EQC), Zell has once again been running away from big downside risk in property prices. Or, in this case, it’s more like he’s taken a leisurely stroll. As opposed to a single headline-grabbing transaction, management has liquidated 164 assets for $7.6 billion over the past six years and used the proceeds to repay $3.3 billion of debt and preferred stock, distribute $1.2 billion to shareholders, and repurchase $266 million of stock. As a result, EQC currently holds a war chest of $3 billion in cash—or $24 per share—nearly 90% of the company’s current market capitalization.

Needless to say, this type of situation does not attract a lot of attention. It can be a challenge for Wall Street to drum up excitement for a growing pile of cash managed by a patient investor literally willing to wait years for the right opportunity. No wonder Equity Commonwealth is covered by all of two sell-side analysts.

Zell’s style is a perfect complement to Broyhill. And his management team is exactly the type of skilled capital allocator we look to partner with. We’ve followed the company closely since an activist campaign put Zell’s team at the helm. We’ve watched with excitement as the team capitalized on record prices and sold assets to build its cash hoard. All the while, the competition paid higher and higher prices to expand their empires on the backbone of cheap credit. With that same competition now on its knees, we expect Zell to fully capitalize on the situation.

The downside here can be easily quantified. With $24 in cash and a few additional dollars per share in the four remaining properties held by Equity Commonwealth, it’s going to be difficult to lose money on our investment aside from someone lighting it on fire (note that we don’t actually expect anybody to light this cash on fire and all investments carry the risk of less; we just think that risk is much lower here). Like Zell, we move quickly and aggressively when we find a mispriced asset with capped downside and the potential for significant upside. Consequently, we established a large position in the stock during the third and fourth quarters, after watching patiently from the sidelines for years.

It turns out that value investing is equally effective in real estate. The principles are the same. Buy with a margin of safety and wait for the market to realize that value. Here’s Sam Zell on liquidation value as a margin of safety. “I have never suffered from any transaction turning out to be too good. The real issue is ‘What is the downside?’ My formula is very simple. It starts and ends with replacement cost because that is the ultimate game. In the late 1980s and early 1990s, I was the only buyer of real estate in America. People asked me, ‘How could you buy it?’ How could you project yields? Rents? For me, it came down to these issues: Is the building well built? Is it in a good location? How much less than the cost of replacement is its price?”

COVID hasn’t made that math any different today. But it has provided Zell and company with the buying opportunity of a lifetime. While most investors are looking at the current situation and extrapolating it far into the future, Equity Commonwealth is positioned to take the other side of that trade. Management is targeting a variety of asset classes that have been hit hard by investor sentiment. The team is contrarian in their thinking, evaluating out-of-favor sectors, such as lodging, retail and office.

In the past, the company has avoided discussing the type of transactions they were reviewing, but given the increasing likelihood of potential new investments, management shed light on their approach on last week’s investor call.

We’ve been consistent in our investment approach, targeting portfolios, platforms, and companies rather than individual assets. Given the optionality we’ve earned through the successful execution of our $7.6 billion of dispositions, we believe it’s prudent to focus on transactions that will help define our future rather than one-off deals.

It would seem that we are getting closer to a deal. And given the company’s history as an orphaned equity, we believe the announcement of a large, transformative acquisition would immediately spark a rerating in the stock driven in part by a regular dividend and broader ownership through REIT and other income-oriented investors. Longer term, we see the potential for shares to double assuming Equity Commonwealth levers up in line with peers to buy assets at distressed prices.

Everything Is Fun And Games(top) Until Somebody Gets Hurt

“I bought $6 billion worth of tech stocks, and in six weeks I had lost $3 billion in that one play. You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basket case and couldn’t help myself.” – Stanley Druckenmiller

Few would argue that Stan Druckenmiller is one of the best investors of all time. He managed money for George Soros from 1988 until 2000, when he took a beating chasing tech stocks. Like many investors today, he just couldn’t help himself. Even the best are susceptible to the siren songs of the market.

Market tops are a process. They take time to unfold. They don’t happen overnight. Greenspan first warned of irrational exuberance in 1996, but the Nasdaq didn’t break down until four years later. Housing prices peaked in 2006, and Bear Stearns bailed out its related hedge funds in 2007. But the market didn’t completely break until Lehman’s failure in 2008.

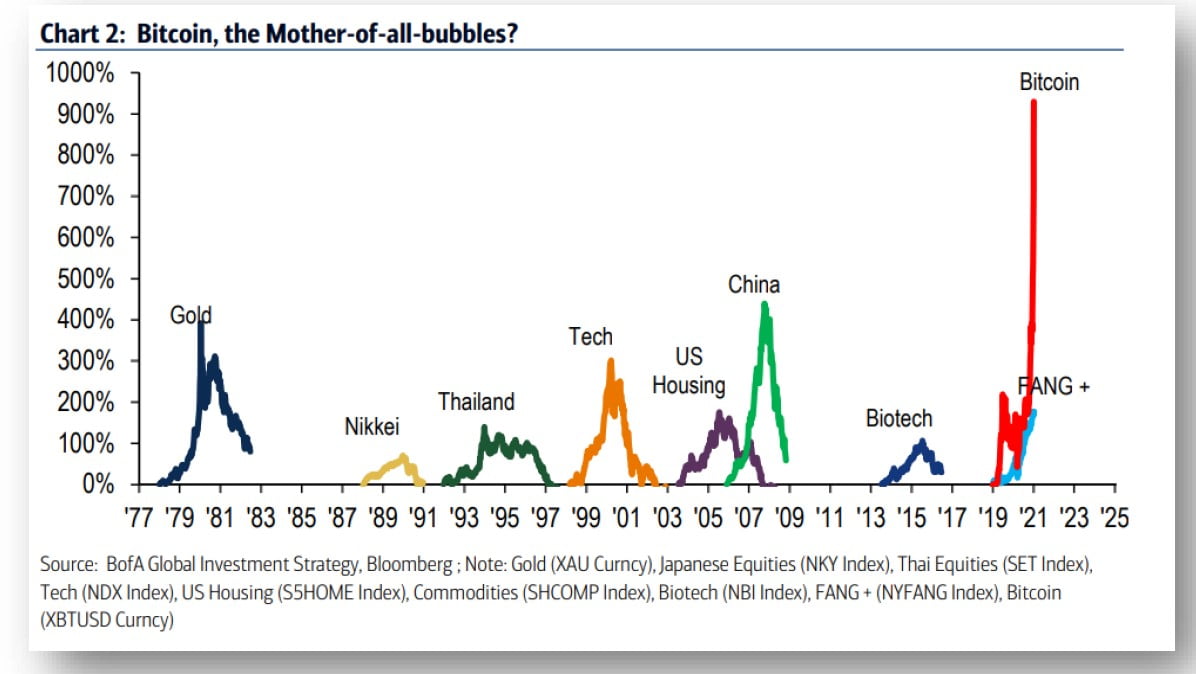

Every financial market mania is different. Each has its own unique flavor and speculative excesses that manifest in different ways at different times. But mania also share many common characteristics. This is the third speculative episode we’ve witnessed in our career. After you’ve seen a few, you notice similarities in investor sentiment, financial market activity, and corporate behavior. They are not always the same and not always apparent each time, but when you put enough of them together, you can get a good sense of where things stand if you’re willing to pay attention. As Henry David Thoreau suggested, “It’s not what you look at that matters. It’s what you see.” And today, we see exuberance everywhere we look.2

To start, there is bitcoin. The way finance works today, according to Bloomberg’s Matt Levine, is that things are valued on their proximity to Elon Musk rather than their cash flows. So naturally, Bitcoin surged 15%, hitting its all-time high, after Tesla invested $1.5 billion in the controversial cryptocurrency and said it would accept the digital token as a payment for its electric cars.

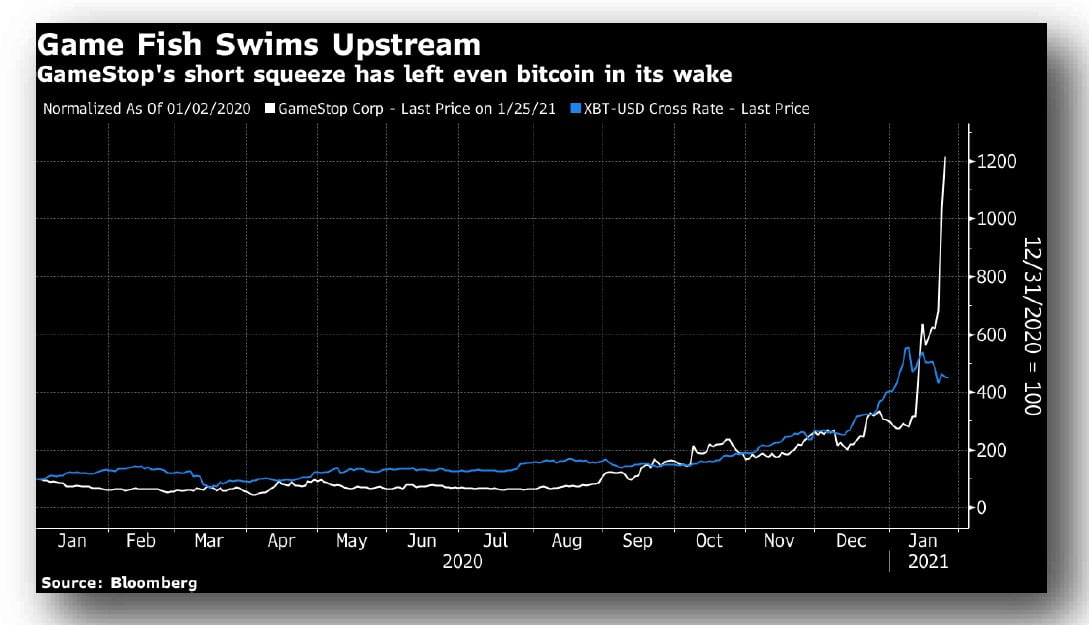

Elon is the richest person in the world, so naturally, if he tweets “Gamestonk!” then you too can become the richest person in the world if you buy it.

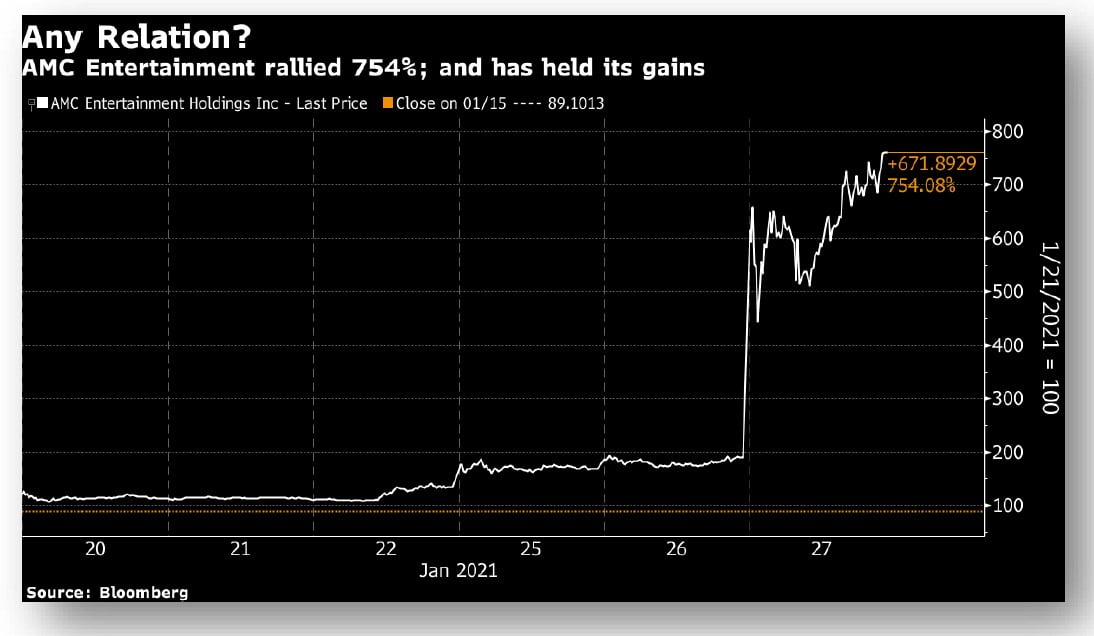

GameStop is an extreme example, but it is certainly not an isolated one. Stocks with the highest short interest have been on a tear this year. So have many of those teetering on bankruptcy. AMC Entertainment (AMC) is a large movie theater chain that has been crushed by the pandemic. In the last week of January, its stock ripped about 750% over a few days.

We’ve seen a number of short squeezes in our time, but nothing like what we just saw. In the past three months, a basket of the fifty most heavily shorted stocks in the market roughly doubled. The next biggest move outside of this cycle occurred in 1999 and 2000. It’s up ~ 350% since March after tacking on another ~ 60% last month.

Squeezing the movie theater shorts may or may not be a good idea. But we doubt buying a totally different company on the same premise will turn out to be a smart move. Shares in AMC Networks (AMCX) gained 70% in less than a week as retail investors piled into the similarly named stock.

At the start of this year, the median S&P 500 stock had short interest of just 1.5% of market cap, matching the lowest level reached since 2000. One difference between the typical short squeeze and the recent rally is the degree of retail involvement, investors who have a thing for penny stocks, for firms with negative earnings, and for extremely high-growth, high-multiple, story stocks.

Such violent moves come with consequences as unsustainable excess in a small corner of the market can ripple throughout the pond. Crowding and concentration can create turmoil when the big fish are forced to deleverage. According to Goldman Sachs, recent weeks saw the largest hedge fund de-grossing since the financial crisis.

Money chases performance, which explains why we are mesmerized by the handful of stocks soaring into the stratosphere. But there is no better example of this herd behavior than investors chasing the hot hands of Cathie Wood, CIO of ARK Investment Management. Ark managed $3 billion this time last year. At year end, the firm’s assets stood at $58 billion. Only Vanguard experienced more capital inflows.3 According to FactSet, nearly half of ARK’s equity holdings are invested in stocks that the firm owns at least a tenth of all shares. We wonder what happens if those capital flows reverse.

It has become the norm to attribute what is going on in the markets to low interest rates. Low yields may justify lofty valuations, but they don’t justify the flash mobs piling into bankrupt stocks. This type of fun and games is more about excess liquidity sloshing around looking for a home.

The following chart from Goldman Sachs shows the market cap and trading volumes for ridiculously expensive stocks. In a normal market, there aren’t many companies trading above 20x sales. Today, there are enough for everybody to enjoy. In fact, these stocks accounted for nearly a quarter of trading volume and almost 10% of the US equity market.

For those trafficking in such high-flying story stocks, we wish them luck. But they might be better served taking a clue from corporate insiders who are dumping shares at a record pace.4 Most CEOs are terrible allocators of capital when spending shareholders’ money. Buybacks are more common at higher prices than at lower prices. And M&A really heats up around market tops. Ironically, those same CEOs are much more prudent when investing their own money. Insider buying usually picks up near the market’s low point (as we saw back in March) while insider sales always surge as we approach market tops.

Perhaps the most common clue of late-stage manias is a surge in new offerings. This is when retail investors claw and scratch their way to get their hands on the latest and greatest hot new issue that Wall Street is selling. While a new issue’s first day pop and short-term returns can be extraordinary, most of these over-hyped and over-inflated businesses fizzle just as spectacularly. Notably, last year was the best year for IPOs since the dot-com boom, and it was followed by the busiest start to a year with over 200 companies coming to market in January 2021.

New offerings typically come to market dressed to impress but even the best lipstick won’t turn a pig into a princess. Despite the street’s best efforts, the princess always ends up in the mud. But it hasn’t stopped them from trying. Today’s Special Purpose Acquisition Companies are covered in lipstick. SPACs can be raised by virtually anyone.5 The SPAC manager raises capital from retail investors for investment in hot sectors like Cannabis, Electric Vehicles, Space Travel, or Online Gambling.67 They are heavily incentivized to invest that capital as quickly as possible to generate fees, creating enormous misalignment of incentives and, to no one’s surprise, poor long-term performance. Of the 107 SPACs that have gone public since 2015 and executed deals, the average total return has been a loss of 1.4%, according to Renaissance Capital.

We suspect that this time will be no different. And once again, individual investors, who make up nearly half of all SPAC trading, are likely to bear the brunt of the damage. One study found that hidden fees and costs are so large that for every $10 raised in a SPAC IPO, less than $7 in cash remains by the time the average SPAC acquires a target.

Given the magnitude of the capital raised, future losses are likely to be even greater than the poor returns posted on average. These “blank-check companies” raised more money in 2020 than all the capital raised in the last ten years combined.8

Signs of widespread speculation are everywhere, but perhaps the most disturbing is the surging confidence of retail investors with limited or virtually no investment experience.9 Retail activity follows rapid market gains. But last year was exceptional even by the standards of the early 2000s’ day traders. Robinhood and other game-like trading apps have facilitated off-the-charts trading volume, with several instances of major retail brokerages facing capacity issues on the back of record order flow.

The volume of speculative call options traded has doubled since the pandemic. About 20% of this volume comes from orders of 10 contracts or less – i.e. retail traders with too much time (and stimulus money) on their hands. Record call option volume in the most speculative stocks reflects the widespread interest of retail investors in short-dated, highly levered positions. It appears that everybody has become an options expert overnight.

Valuing companies that don’t make money can be somewhat of a challenge for fundamental investors tied to reality or to old ways of doing things. One way around this pesky challenge is to get creative and value businesses on other metrics like sales, or eyeballs, or clicks. One good thing about this approach is that you can use your own rules and your own measuring stick. Perhaps this explains the surge in non-profitable companies which has reached meteoric proportions.

The upside is that once a stock reaches a silly price, there’s nothing stopping it from reaching 2x or even 10x a silly price. Given the growing cohort of stocks trading at silly prices, it’s worth revisiting this interview with Sun Microsystems’ CEO Scott McNealy, who made the following comments about his firm’s valuation in 2000.

At 10x revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are?

One thing is for sure. If markets ever decide to fall again, a lot of investors are going to look back at all of these red flags and wonder WTF they were thinking?!?!?

A New Year

In January 2000 a conservative Fidelity Fund Manager resigned after outperforming the market for two decades. ”Hanging up his spurs today probably signals that he is exhausted from banging his head against that momentum wall.” Mr. Vanderheiden said he thought a value revival might be just around the corner, noting that the end of other investing crazes — the run-up in the Japanese stock market during the 1980s, the biotechnology craze of 1991 and the rise of the Nifty 50 in 1972 — all fizzled around the start of a new year. ”What I’ve found over a lot of years is that a lot of these manias seem to end at the end of the year.”’

It’s a new year, but the insanity continues. For now.

If you look closely enough, a sea change has already begun beneath the market’s surface. Word of an effective vaccine sent the world’s cheapest stocks surging the most on record relative to their faster-growing peers. We think they have a long way to go as value is poised to benefit from several catalysts ahead. Depressed earnings are all but certain to rebound from the temporary lows reached during the height of lockdowns. At the same time, multiples are likely to expand alongside increasing margins as corporations cut operating expenses and maximize cash flow by drawing down working capital, suspending buybacks, dividends, and capital expenditures. As a result, for the first time in a long time, consensus expectations for earnings growth generated by “value” stocks are higher than the growth of “growth” stocks.

This is a stark change from recent years and from the previous twelve months. In 2020, Russell 1000 Growth earnings rose by 6% while Russell 1000 Value earnings fell by 20% for the year. But unless you are one of the fortunate investors at Hindsight Capital last year’s numbers don’t offer much in the way of forward returns. For those of us looking to allocate capital today, you might note that consensus expectations for the Russell 1000 Growth Index are ~ 17% annual earnings growth over the next two years while the earnings power of Russell 1000 Value Index is expected to grow at 23% annually over the same period. You might think that was something value investors would get excited about. Yet, growth stocks still trade at 27x next year’s earnings, nearly twice the multiple of value stocks, which are trading at 15x estimates. Which would you rather own going forward?

Many investors (present company included) have anticipated the re-emergence of value for years. And many have been habitually disappointed. So why are we so confident that Lucy won’t snatch the football away from Charlie Brown again this time? Simply put, the fundamentals have changed. Value is poised to benefit from extremely easy comparisons this year in contrast to almost impossible comparisons for growth stocks. As such, it seems increasingly likely that the current mania’s expiration date is past due. If correct, history suggests that such rotations can run further and last longer than even the most bullish expectations.

Given the striking similarities to the tech bubble, a look at that cycle may prove informative. The underperformance of value relative to growth over the past five years is almost identical to the five years ending February 2000. After underperforming by nearly 150% in the five years prior to the tech bubble’s peak, value went on to trounce growth as the bubble deflated. Despite the early pain, patient investors were ultimately rewarded for their perseverance – value outperformed over the full period by a wide margin. As it turns out, the price you pay does matter.

If we are correct, the performance of the overall market might not be the big story for the new year. The market may be up or down, but we suspect the big story will be the turn in the tide toward value that most investors have failed to prepare for or even imagine. Big cap growth at any price is likely to take a back seat to shorter duration, asset-heavy, cyclical stocks that have been left in the dust.

With the gap between the “haves” and the “have-nots” never so wide, the market is made up of businesses trading at extraordinary rich valuations at the same time many others trade at historically low prices. On the one hand, we have the Horizons Marijuana Life Sciences Index which rallied 140% in the first few weeks of the new year. The top five stocks in this index generated $1.6B in sales over the last twelve months and trade at a combined $37.3B market capitalization or more than 23x sales. In contrast, Reduced Risk Products (RRPs) at Philip Morris (PM) generated over $6.8B in sales last year, which is a multiple of less than 20x on PM’s current $135 billion market capitalization. So one can buy the top five marijuana companies that burned a cumulative $1.2 billion in free cash flow over the last year for 23x sales, or Phillip Morris’ RRPs for less than 20x sales and get over $9 billion in free cash flow generated by their traditional business for free! As a bonus, we’d note that RRPs already account for a quarter of total revenues at PM growing at ~30% annually and with higher margins than combustible cigarettes. Hard to believe this is reflected in today’s price at half the market multiple. Naturally, we favor the latter.

Bottom Line

“What is a cynic?” “A man who knows the price of everything, and the value of nothing.” – Oscar Wilde

According to Oscar Wilde’s definition, there is no shortage of cynics in today’s market. Price is all that matters. Nobody knows value because many of today’s valuation multiples are nonsense.

In one corner, we’ve heard rumors of traders being fired on the spot for even whispering the “F” word – “Fundamentals.” And in the other corner, we have an irrational, speculative casino where bankrupt stocks get bid up on Robinhood and Reddit. It’s a disaster waiting to happen. It will end in tears. Or worse.10

This is not the time to chase soaring prices in the hopes they go even higher. When sentiment is stretched and assets are priced for perfection, there is a lot of room for disappointment. Layer on technical factors like quant programs, factor-based models, and forced selling, and we see even greater potential for dislocations in individual securities.

Looking ahead, we think prospective returns for traditional portfolios look low. Unfortunately, returns on cash don’t look any better, and we’re not willing to bet against this avalanche of liquidity only to learn the lesson so many short sellers learned over this past year. Fortunately, we think our prospects are as good as ever, and going forward, we think value investing is a decent bet in a world full of bad bets.

There is value hiding in plain sight. It just requires the patience, discipline, and willingness to stand apart from the crowd. Remember. It’s not what you look at that matters. It’s what you see.

We see opportunity. And we are putting capital to work when we find it. Our pipeline remains full of interesting puzzles to put together. We are no longer drinking through the firehose, but a steady flow of new situations is keeping us busy.

We love what we do and we are fortunate to be able to do it with such a wonderful group of partners. You are the reason we come in every day with a child-like curiosity and a passion for the hunt. We’ve had quite a ride over the last decade. We are even more excited about the next. When we look at our portfolio today compared to every other alternative, we think you’ll be pleased to come along for the ride.

Sincerely,

Christopher R. Pavese, CFA

Chief Investment Officer

Broyhill Asset Management

As the opportunities to add value increase so does the personal risk, the career risk, and the business risk, until finally there will be incredible opportunities to make money . . . that no one will dare to take advantage of. We would like at least to be the last ones trying. – Jeremy Grantham

See the full commentary here.