S&P 500 stopped consolidating in the 4,340s shortly after the open, and went largely one way since – except for the run up to the closing bell, which I used to grab short profits off the table. The overnight pump is at work today – not vigorously, but still. Given the credit market posture (yields not rising much on the day), a brief retracement in tech can be expected – especially since yesterday‘s outage news were what powered it in the first place.

Q2 2021 hedge fund letters, conferences and more

VIX has gone nowhere yesterday, and looks unwilling to spend much time below 21 really. We‘re at crossroads where the supports I mentioned on Thursday, are giving way one after another. 4,260s are next in line, followed by 4200s – it would take time to get there, and Friday‘s non-farm payrolls could be the catalyst. Unless they come in outrageously weak, the Fed is likely to announce taper in Nov – monetary policy deceleration into a weakening economy while inflation expectations are rising, supply chains increasingly strained to the point that the International Chamber of Shipping has issued a red alert warning of a global transport systems collapse – make you go hmm.

Something tells me the Fed won‘t be as successful jawboning inflation as in June – its favorite metric, the PCE deflator, isn‘t yielding, and the realization that inflation is here to stay, is creeping in. I don’t know how so much of the financial universe could have been duped by the transitory narrative… for so long.

The energy squeeze is on – I cashed in sizable oil profits yesterday (check at my site the portfolio performance at fresh highs!) – the dollar is stalling, cryptos are rising and adding to open profits too, while precious metals are waking up. I‘m looking for silver to lead and be more resilient – the gold to silver ratio falling first below 73 would be a welcome confirmation of the budding broad recognition of inflation across the markets.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

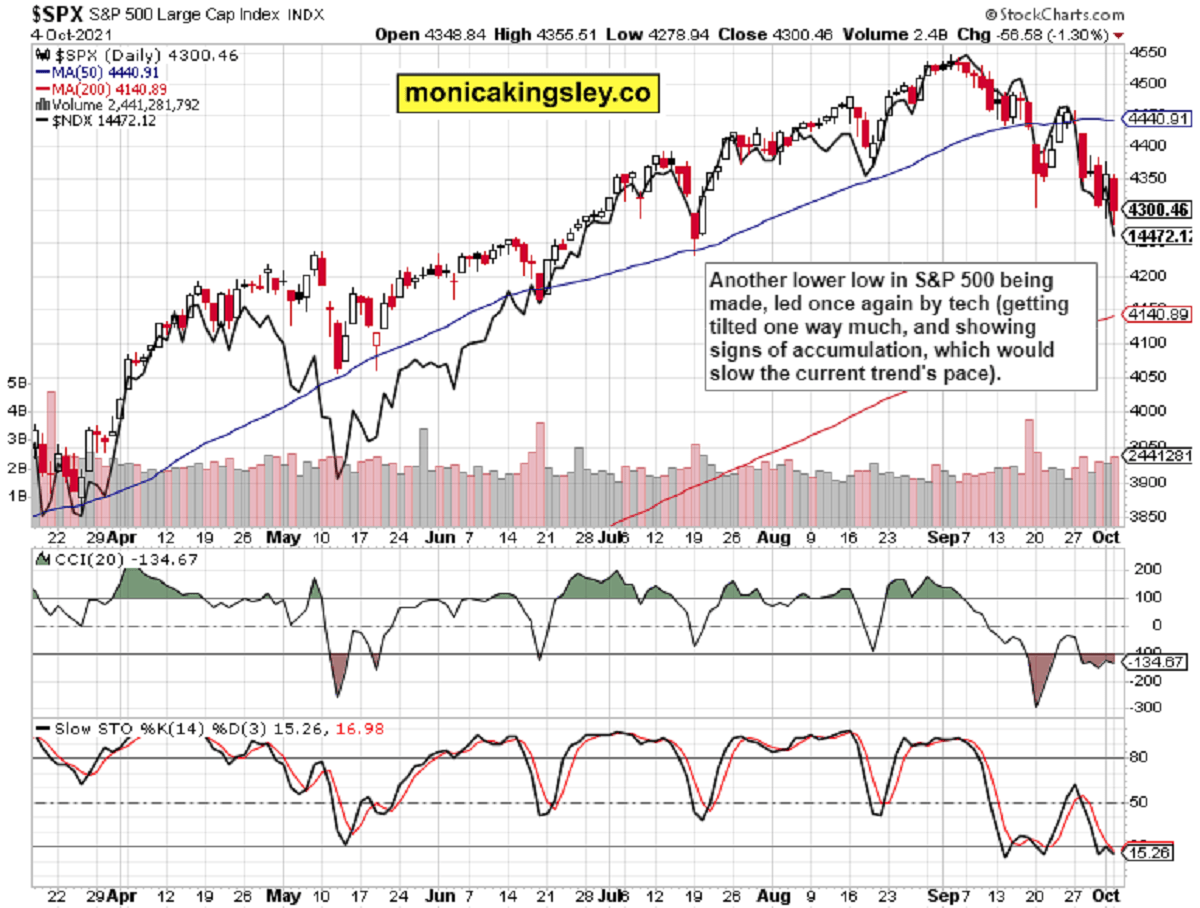

S&P 500 and Nasdaq Outlook

S&P 500 volume doesn‘t show the buyers are serious here. This downswing isn‘t over.

Credit Markets

HYG was really weak yesterday, but the quality debt instruments positioning hints at a reprieve, at a risk-off led S&P 500 pause next.

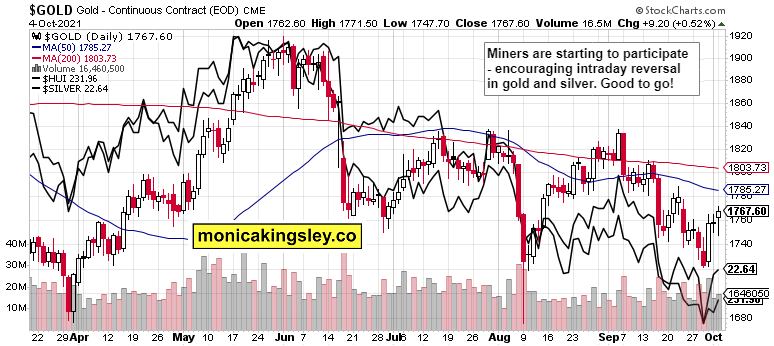

Gold, Silver and Miners

Gold and silver upswing was finally joined by the miners – the sentiment is warming up to further gains.

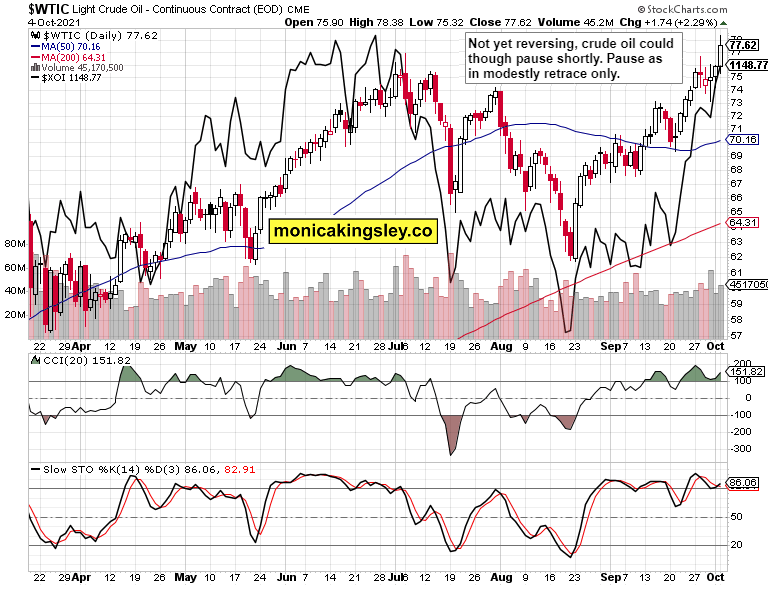

Crude Oil

The crude oil elevator hasn‘t stopped yet, but I wouldn‘t be surprised by a consolidation of gained ground next.

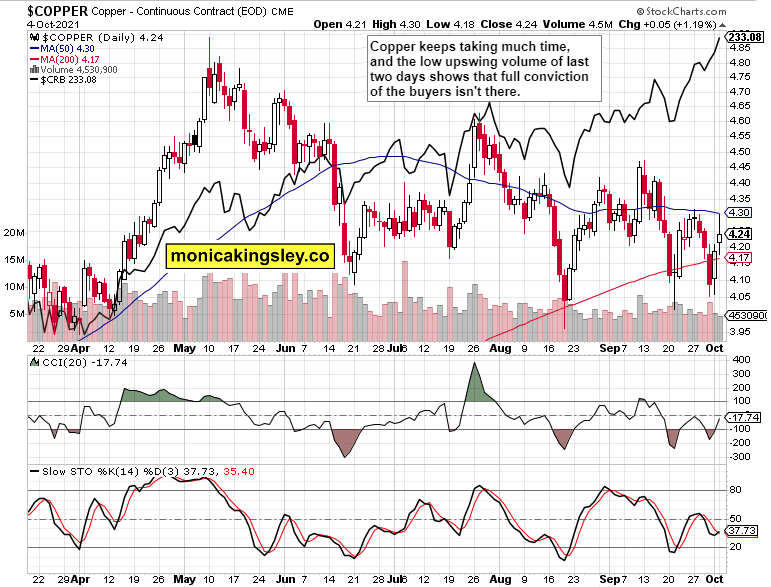

Copper

Copper upswing was a bit too readily sold into, and the volume wasn‘t stellar. This long sideways trend isn‘t over yet.

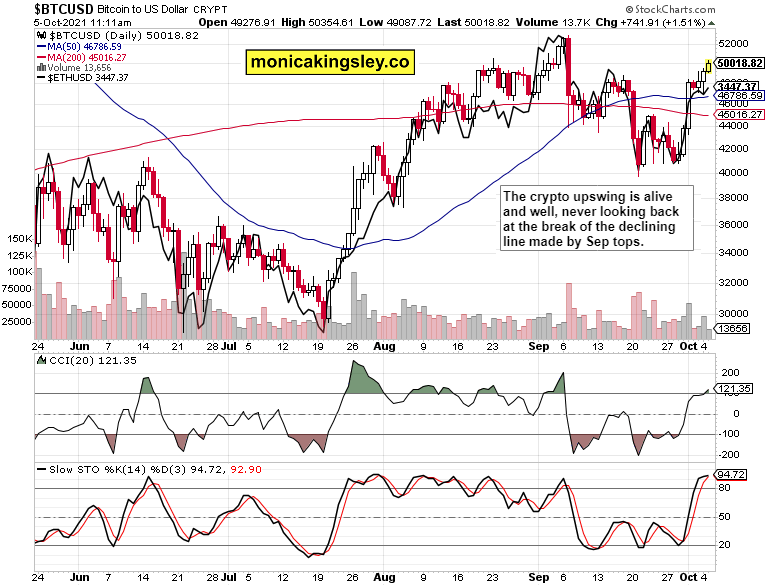

Bitcoin and Ethereum

Bitcoin and Ethereum are approaching the early Sep highs – and look likely to overcome them.

Summary

Stock market bears still have the upper hand, and credit markets are signalling caution. None of the intraday reversals to the upside have stuck, and we haven‘t reached a local bottom yet. Coupled with the stagflationary undertones, the cyclically sensitive commodities have a harder time than oil. The dollar is likely to come under increasing pressure, which would underpin precious metals and commodities alike.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for all the five publications: Stock Trading Signals, Gold Trading Signals, Oil Trading Signals, Copper Trading Signals and Bitcoin Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

Oil Trading Signals

Copper Trading Signals

Bitcoin Trading Signals

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.