Excerpt from Stanphyl Capital’s letter to investors for the month ended August 2020, discussing the size of their QQQ short.

Q2 2020 hedge fund letters, conferences and more

Friends and Fellow Investors:

What the happened this month, and for that matter, the first eight months of 2020?

The short answer is: I’m a “long value/short bubbles” investor in a market where “the bubbles” are hugely outperforming “the value,” and thus losses from our short positions overwhelmed the gains from our longs, which on their own are up considerably.

Now, here are the long answers, and why I think things are about to turn around for us…

First, here is the approximate year-to-date (for stocks we’ve held since January 1) or “since purchase” (for stocks bought during 2020) performance for our longs; these figures are approximate because I’ve added to or trimmed these positions along the way, sometimes booking profits at higher or lower levels:

ASYS: +43%

AVNW: +54%

DAIO: +23%

EVOL: +14%

(I also took profits on approx. 40% of our EVOL on a no-news spike into the $1.30s, +40% from our basis)

GLD: +14%

JCS: +0%

(I also sold a substantial part of our JCS position this year in the $5s, for a small gain.)

WSTL: +19%

(Except for a tiny stub position I sold our WSTL this summer.)

Reduction In The The Size Of QQQ Short

Meanwhile, year-to-date the Russell 2000 Value ETF (ticker IWN), the nearest benchmark for these positions excluding GLD, is down over 18%, so our microcap long stock picking skills have been solid. However…

Against these positions (due to the market’s tremendous decoupling from economic reality), we carried (primarily as a hedge against our longs) a QQQ short position averaging around 20% larger than the size of our combined longs (as the microcaps tend to be more volatile), and year-to-date QQQ is up 39%. (In late August I reduced the size of our QQQ short—more on that below.)

Additionally, we’ve carried a Tesla short position that averaged only around 1/5th the size of the QQQ short (i.e., approximately 10% to 15% of the fund), but year-to-date Tesla (the biggest bubble in modern stock market history) is up an astounding 495% (to a fully diluted market cap of approximately $515 billion vs. $523 billion for Toyota, VW, GM, Daimler, BMW, Ford, Fiat-Chrysler, Honda and Nissan combined), and that hurt us significantly. So our short positions have obliterated the profits from our long positions, and yet when this bubble pops we’ll be glad we have them.

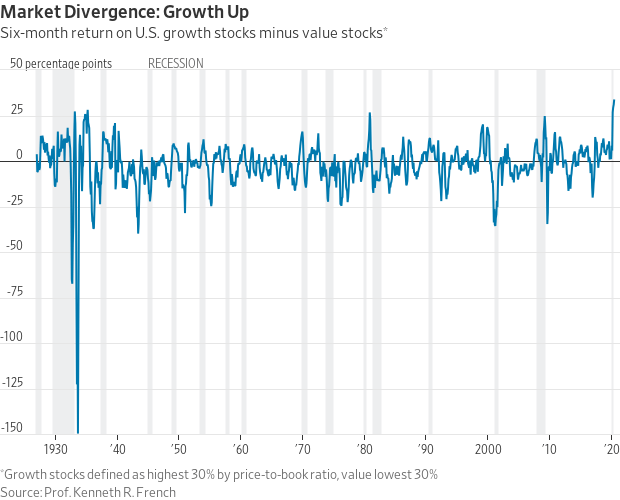

The dichotomy between our longs and our shorts is well illustrated in this chart showing a record divergence between the performance of “growth stocks” vs. “value stocks,” yet I believe that as has always happened in the past, this will mean-revert in our favor:

As mentioned above, in late August I did reduce our QQQ short, to the point where it’s now approximately 2/3 the combined value of our longs; this leaves us a bit more “naked long” than I’d like to be in the current environment, but a Federal Reserve pledging to leave rates at zero for years so it can ruin Americans’ purchasing power has been a hell of a painful headwind.

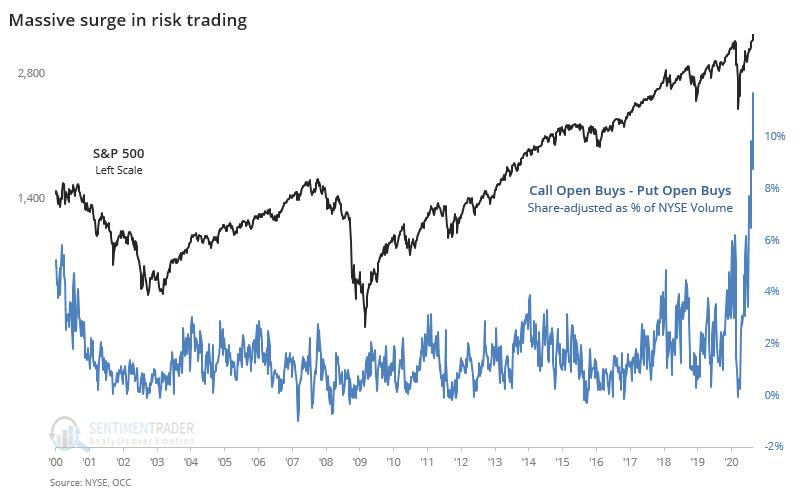

Why, then, maintain this QQQ short at all? I have a “near-term reason” and a “long-term reason.” Near-term, bullish speculation is (literally) off the charts: for the last two weeks the Put-Call ratio for Nasdaq 100 constituent stocks closed at the extremely low (i.e., “complacent”) level of 0.42 and intra-day today it hit 0.21, which may be the lowest level ever. Meanwhile, @SentimenTrader points out that call option buying as a percentage of NYSE volume far exceeds that of the 2000 bubble era…

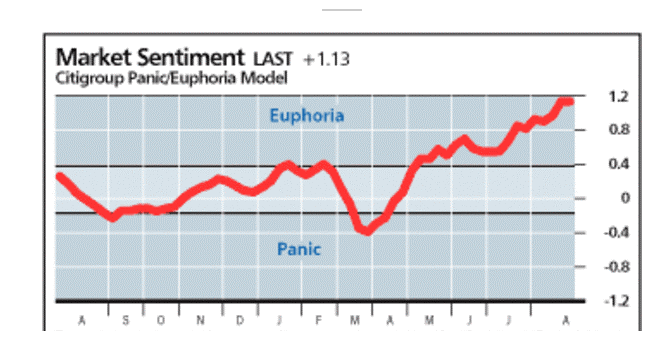

…while @hmeisler shows us that Citi’s Panic/Euphoria index is well into “Euphoria” mode—by far the highest it’s been since the bubble peak in 2000 (when it hit approximately 1.5):

Valuation-wise, on a forward PE basis, the S&P 500 is now at the peak of the 2000 bubble…

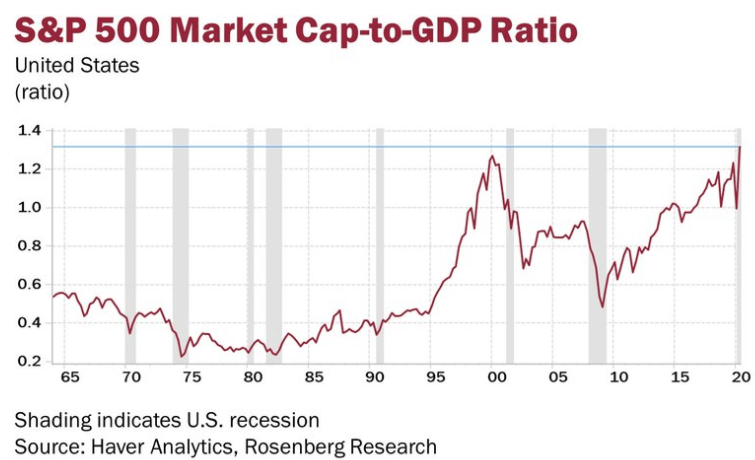

…while as a percentage of GDP the S&P 500 now exceeds the 2000 bubble’s peak…

…and the broader stock market (the Wilshire 5000) hugely exceeds the 2000 peak:

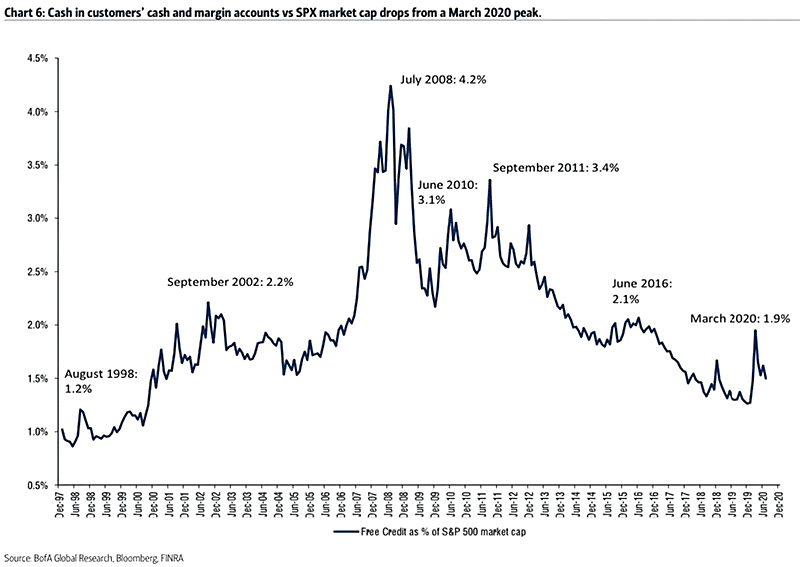

And from @ISABELNET_SA we can see that available buying credit (cash) in customer accounts as a percentage of S&P 500 market cap is down near the level it was at the peak of the 2000 bubble…

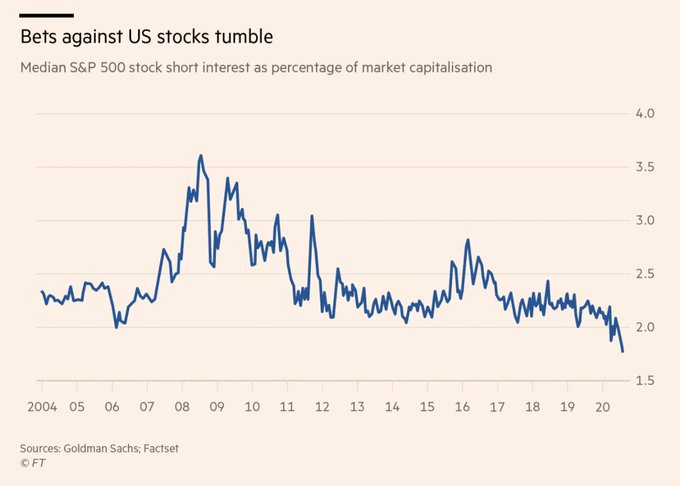

…while as @Fxhedgers points out, there are almost no shorts left:

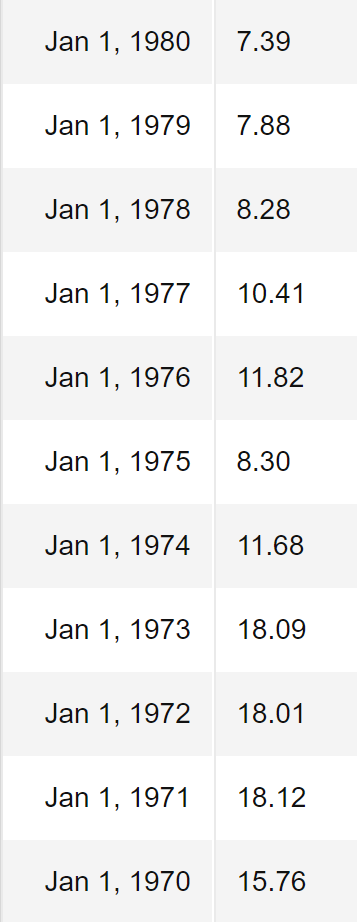

So “excessive bullishness & complacency” is the near-term reason why I maintain our QQQ short position. Medium-to-longer-term I believe the Federal Reserve’s endless money-printing combined with massively profligate deficit spending from both parties in Washington and growth-retarding levels of debt will return us to an environment similar to the stagflationary 1970s; i.e., slow growth and high inflation (which we got a hint of this month). In that environment, high-flying stocks (such as the QQQ we’re short) will suffer massive PE multiple compression, and gold (which we’re long) will climb steadily. Have a look at what happened to S&P 500 PE ratios during the decade of the 1970s, beginning in 1974 when inflation really took off:

By way of comparison, the current TTM GAAP PE ratio on the S&P 500 is approximately 36, and it’s 38 on the Nasdaq 100.

Growth Makes People Pay Up Not Interest Rates

For those who believe that a 38x Nasdaq PE ratio is justified because interest rates are currently so low and “there is no alternative,” I’ll point out that Japan has spent decades with similar rates yet PEs there are far lower (currently around 23x on the Nikkei 225), and in that time Japan has experienced multiple bear markets. Why? Because ultimately it’s growth not interest rates that get people to “pay up” for stocks. For example, as recently as May 2004 the Fed Funds Rate was just 1%, yet the GAAP PE ratio for the S&P 500 was just 20x, which is 44% lower than today’s 36x. In other words, money can always find “an alternative,” and if real-world inflation takes off there will be alternative places to invest regardless of how artificially low the Fed caps Treasury rates—real estate, floating rate private-sector lending, commodities, etc., will all offer far better returns than those “capped” (until the Fed eventually loses control) Treasury rates.

As one last example of what a bubble this market is, let’s have a look at earnings “improvement” since 2015 for Apple, which is now Nasdaq’s (and the world’s) largest company by market cap. Although we have no direct position, it’s the largest constituent of QQQ:

- Apple’s 2015 net income: $53.4 billion

- Apple’s August 2020 TTM net income: $58.4 billion

- Five-year increase in Apple’s net income: 9.4%

- Compounded annual increase: 1.8%

So in five years Apple’s net income is up just 9.4% (and that’s likely entirely due to Trump’s large corporate tax cut, much of which a Biden administration would rescind). Yet during that same period Apple’s market cap increased from roughly $650 billion to approximately $2.2 trillion! (Yes, a somewhat higher percentage of today’s revenue is considered to be “recurring,” but nowhere NEAR enough to justify that kind of craziness!)

So in summary, I continue to maintain significant short positions in this environment and hope you’ll stick with the fund despite its awful performance; if nothing else, we’re a partial hedge against the overwhelmingly long bias of most stock portfolios.

Portfolio Holdings

Here then are the fund’s specific positions, beginning with the longs; please note that we may add to or reduce position sizes as stocks approach or recede from our target prices…

We continue to own Aviat Networks, Inc. (ticker: AVNW), a designer and manufacturer of point-to-point microwave systems for telecom companies, which in August reported a solid Q4 for FY 2020, with COVID-affected revenue down slightly vs. the year-ago quarter but earnings, EBITDA and backlog up substantially, with management guiding to meaningful growth on both the top and bottom lines for FY 2021 (which began this past July). In January Aviat’s board (controlled by activist investor Warren Lichtenstein) appointed a new CEO and the accompanying press release made it quite clear (based on his experience) that he was brought in to dress up the company and get it sold. Meanwhile, Aviat’s closest pure-play competitor Ceragon (CRNT) sells at an EV of approximately 0.65x revenue. If we assume $240 million in annual revenue for Aviat, $33 million of net cash and a (very conservative) $10 million valuation on a combination of $404 million of U.S. NOLs, $8 million of U.S. tax credit carryforwards, $189 million of foreign NOLs and $2.6 million of foreign tax credit carryforwards, we get a current fair market valuation of 0.65 x $240 million = $180 million + $33 million net cash + $10 million for the NOLs = $223 million divided by 5.4 million shares = $37/share; presumably, an acquisition would be at a higher price due to the “control premium.”

We continue to own Data I/O Corporation (DAIO), a manufacturer of semiconductor programming devices. We previously owned this stock in 2016 when we bought it in the $2s and sold it a year later in the $4s and $5s (it eventually ran to the $16s before collapsing, as it got way ahead of itself as new holders failed to account for its cyclicality), and now we’ve repurchased it for another run. In 2019 (a year that without 2020’s COVID would have marked a cyclical low for the company) DAIO did $21.6 million in revenue with a 58% gross margin. In August it reported a COVID-affected Q2, in which it did $4.7 million in revenue (still with a 52.4% gross margin) accompanied by an $878,000 operating loss, but negative free cash flow was only $438,000 and the company ended the quarter with $13.3 million in cash and no debt, and with its increased backlog & bookings should be able to return to profitability within a couple of quarters. Using 2019’s revenue and valuing DAIO at 2x that cyclically low figure (this company is much more levered to customer technology cycles than economic cycles), then adding in $13 million of cash would make this stock worth around $6.80/share.

We continue to own Amtech Systems, Inc. (ASYS), a manufacturer of semiconductor production and automation systems, which in August reported a breakeven Q2 that was down (revenue-wise) 28% year-over-year (due to COVID) and roughly flat with Q1. Disappointingly, the company guided to no revenue improvement in Q3 and a decline in earnings. Nevertheless, this is a mid-30% gross margin company that does around $80 million a year in normalized (ex-COVID) revenue with around $4 million/year in operating income (again, ex-COVID), and has around $39 million in net cash and over $80 million in NOLs. If we subtract $1 million from Amtech’s cash to account for two more quarters of “COVID hit,” then value the company at 1x normalized revenue with $8 million for the NOLs, we get fair value of around $9/share. The biggest risk here (other than underestimating “the COVID effect”) is that management—which *is* acquisitive—blows that cash pile on something stupid.

We continue to own Evolving Systems, Inc. (EVOL), a small telecom services marketing company that in August reported a solid Q2 (considering the COVID situation), with revenue up a tiny bit vs. both year-over-year and the previous quarter. EVOL generates over $1 million/year in free cash flow on $25 million of 65% gross margin revenue and would make a great buy for a strategic acquirer, as $1.5 million/year in savings from eliminating the C-suite and cost of being a standalone public company would mean around $2.5 million/year in free cash flow. Thus, at an acquisition price of just $2.25/share (a more than 100% premium to the current price) a buyer would be paying only around 10x free cash flow and 1x revenue (inclusive of .25/share in net cash).

We continue to own Communications Systems, Inc. (ticker: JCS), an IOT (“Internet of Things”) and internet connectivity & services company, although I reduced the position size considerably when in August it reported Q2 revenue up a very nice 5% sequentially, but accompanied by a very ugly $1.6 million operating loss. Although this company is still cheap on an EV-to-revenue basis (it has around $2.60/share in net cash), a combination of that Q2 operating loss plus management’s headline in the earnings release that it’s “seeking new acquisitions” (which I read as “potentially blowing a beautiful balance sheet on something stupid”) mean that I now have a “wait and see” attitude and no longer want to carry a position that’s as large as it was previously.

As discussed in last month’s letter, in July Westell Technologies Inc. (WSTL) announced the most shareholder-unfriendly move I’ve ever seen, a “go-dark” transaction whereby it plans to delist from Nasdaq and stop filing SEC statements without buying out any shareholders except “odd-lot” owners of fewer than 1000 shares (at $1.48/share). This forced us to sell our entire position to “odd-lot arbs” at a considerable discount (low $1s) ahead of the proposed September transaction, and we’re now out of the stock completely except for our own remaining “odd lot” of 999 shares.

Finally on the long side, as central banks increase their money-printing to ever higher levels in order to fund multi-trillion-dollar annual deficits, we continue to hold a substantial long position in the gold ETF (GLD); the likelihood of negative real interest rates for years to come adds a substantial tailwind to this position.

Thanks and stay healthy,

Mark Spiegel