Logos LP commentary for the first quarter ended March 31, 2020, discussing the greatest buying opportunities for the patient long-term investor.

[klarman]Q1 2020 hedge fund letters, conferences and more

“Nature does not hurry, yet everything is accomplished.” – Lao Tzu

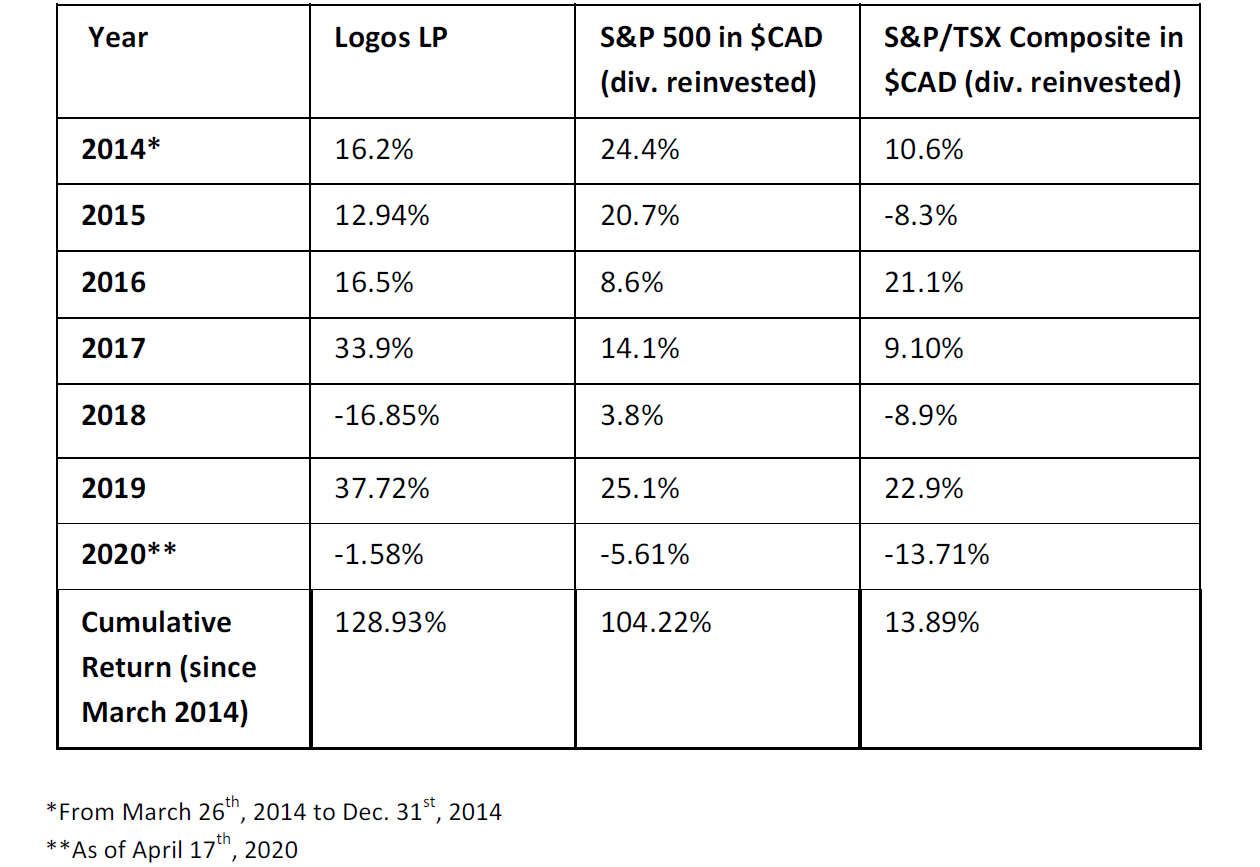

The following table represents Logos LP’s YTD return1 compared to a basket of relevant indexes. The price per unit as of April 17th, 2020 is $28.67 compared to $29.12 as of December 31st, 2019:

The Greatest Buying Opportunities

It is no secret that markets rolled over this past quarter from the COVID-19 shutdown creating what looks to be the deepest recession since 2008-09. Over 17 million North Americans are now unemployed (a 35 sigma event) and businesses of all sizes have grinded to a halt in a matter of weeks. As a result, Q1 was by far the most active period in the history of the fund as we experienced what we believe to be one of the greatest buying opportunities for the patient long-term investor since the Great Recession of 2008-2009 and perhaps one of the greatest buying opportunities in the history of the capital markets.

While we monitor specific stocks on our watchlists, we also dive deep into the data using evidence-based research which helps to provide insight regarding sentiment. This view of investor sentiment can increase the probability of deploying cash with a more favorable risk/reward profile.

Although it is an impossible task to time markets, understanding the temperature of the market and thereby making informed inferences as to the market’s probability of swinging from one extreme of the pendulum to the other is possible. It is during these times of great short-term pricing dislocations brought on by sudden economic shocks that high quality stocks trading at what we believe to be below their intrinsic value can be identified. While we have found several data points suggesting a near-term bottom, the following represent a list of those we found of most interest (courtesy of our friends at Sentiment Trader and Tom Lee from Fundstrat) during the Q1 selloff:

- Over 23 days in the past 7 weeks we have seen the S&P 500 move more than +/- 3%. The previous records were Oct. 1932 and Nov. 2008. In those 2 cases, the S&P 500 staged rallies of +40% and +27%, respectively, over the next 12 months.

- MSCI Emerging Market Index price-to-book ratio hit under 1 on April 2nd, 2020. The only other times the index hit those levels were bottoms in 2002 and 2008.

- March 2020 saw the 2nd largest one month change in aggregate cash holdings in AAII survey history.

- On March 31st, 89% of S&P 500 stocks have triggered a MACD buy signal, which at the time was the highest in recorded history. This has only occurred 10 times in the last 30 years and every time this happened, the Nasdaq Composite has rallied 6 months later by a median of +18%.

- As of March 20th, the average 5-week percentage change of 21 developed markets was – 31.3%. This was the worst 5 weeks ever for global stock investors, beating 2008-09 Great Recession.

- On March 25th, more than 90% of NYSE issues were positive. The S&P 500 is up 100% of the time over the next year by a median of +29% every time this happened.

- The S&P 500 is at 2,845 (which is well above 50% retracement loss level). In the 1987, 2003 and 2008 crashes, “bear market rallies” fail at 33% retracement decline. For all three previous bear markets, the bottom was confirmed with a 50% retracement.

Does this mean that we have hit a bottom and things go straight up from here? Unlikely, as we have to consider the current situation in the context of unprecedented uncertainty and the weakness of analogies to the past.

Patient Long-Term Investors Shouldn’t Worry About Hitting A Bottom

Furthermore, the answer to this question of whether we have hit a bottom should not overly pre-occupy the patient long-term investor. Why?

We never know when we have hit a bottom as a bottom can only be recognized in retrospect. As Howard Marks has recently written:

“The old saying goes, “The perfect is the enemy of the good.” Likewise, waiting for the bottom can keep investors from making good purchases. The investor’s goal should be to make a large number of good buys, not just a few perfect ones.”

“So it’s my view that waiting for the bottom is folly. What, then, should be the investor’s criteria? The answer is simple: if something’s cheap – based on the relationship between price and intrinsic value – you should buy, and if it cheapens further, you should buy more.”

Successful long-term investing isn’t about buying only at bottoms and selling only at tops. It is instead about the gradual re-adjustment of one’s portfolio as a function of the significant price movements of individual stocks.

This is precisely the approach we have tried our best to stick with during these unprecedented times. We were able to re-position the fund into stocks that we have been monitoring for some time at what we believe to be good prices. The future is uncertain, the economic shutdown remains a very fluid situation and the amount of unprecedented fiscal and monetary action that has occurred in such a short period of time is unlike anything we have ever seen in human history (balance sheets of G4 central banks – the Bank of England (BOE), the Bank of Japan (BOJ), the Federal Reserve (FED), and the European Central Bank (ECB) – have expanded to 40% of gross domestic product). We don’t know what the precise long-term implications of this shutdown will be past 2020, but one thing we can predict with a degree of certainty is that certain businesses will continue to thrive long after the dust has settled.

Activities

As of April 17th 2020, the fund has realized a 1.58% loss leading to a compounded annual return of 14.81% since inception. Currently, there are 22 names in the portfolio with our top 10 making up 65.17% of the fund’s net asset value and software now makes up over 85% of the fund’s industry exposure. Our portfolio has become more concentrated and we have now been able to take a shot at some of the highest potential growth stocks that have been on our watchlist for over 2 years. Below you will find the top 10 names in the portfolio as of April 17th, 2020:

- ALTERYX INC. (AYX)

- SERVICENOW INC. (NOW)

- TRADE DESK INC. (TTD)

- JOYY INC. (YY)

- ZSCALER INC. (ZS)

- ANAPLAN INC. (PLAN)

- PAYCOM SOFTWARE INC. (PAYC)

- ADOBE INC. (ADBE)

- BAIDU INC. (BIDU)

- BAOZUN INC. (BZUN)

Most of the buys occurred late March and early April when the vast majority of our data triggers flashed green. We are continuing to monitor these purchases as we still have a large cash balance to take advantage of any further dips in the coming months. A number of these stocks were purchased at multiples we never thought possible (enterprise-level recurring revenue software businesses growing at 47% topline per annum with ~80% gross margins at under 10x sales) and we think that the risk/reward profile for these kinds of stocks is more attractive at these levels than other sectors of the economy (ie. airlines, oil and gas, automotive, hospitality) which we think will not see normalized earnings for some time.

Other portfolio moves include the liquidation of all Canadian equity positions. We believe Canada is less attractive for investment than other jurisdictions for a variety of reasons the most significant being: 1) Lack of diversification: real estate is its largest sector accounting for 15 per cent of economic output last year and energy accounted for 9 per cent; 2) Lack of a business friendly government and population: highly unionized, unfavorable tax and regulatory environment and political animosity/indifference towards business; and 3) Highly leveraged citizens.

In fact, we believe that Canada will be one of the worst hit economies post-COVID as its complacency and idealistic tendency to avoid the diligent assessment of the health of its economy have made it uniquely vulnerable to shock. Post COVID we believe that economic growth will no longer be able to be taken for granted. It will no longer be an entitlement in the developed world. We hope that a silver lining of COVID will be a return to rigor and pragmatism for Canadian politics. We shall see…

For now, we think that there are significantly more attractive growth opportunities within the US and emerging markets.

Greatest Buying Opportunities Going Forward: Outlook

Over the past few weeks we have seen the typical torrent of crystal ball forecasting with predictions flying around on just about everything from personal consumption habits to global supply chains. It reminded us of a great quote:

“He who lives by the crystal ball will eat shattered glass.” –Ray Dalio.

Looking back at all the predictions that were made during and after the crisis of 2008 that things would “never be the same” and that “things would change forever” it is important to recall one of the great lessons of this current crisis: humility has been in short supply for a while now.

Who could have predicted much of what has occurred? Just like who can predict much of what will occur?

Instead, we will be modest with our outlook and focus only on one high-conviction trend we believe will have a large impact on the post COVID business climate: the accelerated adoption of new technologies. The planet is currently having a crash course in remote working, digital productivity and automation, e-commerce, digital payments and online social interaction. Technological adoption in such areas is still quite low and thus the growth in these areas which was fueling the bull market pre COVID still has plenty of room to run.

As mentioned in our COVID-19 update on March 15th, 2020 we are thinking of this accelerated technological adoption through the following 3 key themes:

- The rise of the emerging market Millenial/Gen Z — ie. Joyy Inc, Baozun, MasterCard, Baidu etc.;

- The continued expansion of the ‘virtual’ economy as certain transformative digital workflows are likely to stick (fintech, video, e-commerce, virtual purchasing, cloud networking, IT management) – ie. Atlassian, Adobe, Paycom, Zscaler, Trade Desk etc.;

- Mission critical cloud computing and related applications as well as advanced artificial intelligence (and quantum computing) for the enterprise – ie. Alteryx, Anaplan, ServiceNow, F5 Networks etc.

Greatest Buying Opportunities: Conclusion

After this period of “forced” adoption or large-scale “testing” of such technologies, individuals from managers, shareholders, employees to citizens will realize that they had much more to offer than previously thought. Restrictions put in place during the SARS outbreak of 2003 helped accelerate China’s embrace of e-commerce and COVID is having a similar effect globally. The pandemic will highlight the convenience and ease of online life and will expose opportunities for cost savings through increased technological adoption that will be too difficult for managers and shareholders to ignore.

We hope that you and your families are safe and healthy and that optimism and hope for the future has not slipped away. On our end this health crisis has reminded us that we all too often try to insulate ourselves against any discomfort before it even arrives. We seek to avoid pain by trying to control our external conditions to suit our comfort zones. This perception of control is alluring yet we risk losing the potential joy of discovery and the freedom of finding that we can learn and even be happy, within a much greater range of experiences than we thought. This period of pain has been difficult for us, but we are confident that we will look back upon it fondly as a period of exceptional personal growth.

We are grateful for your continued support and will continue to dedicate our time and effort on your behalf. In the meantime, if there are any questions please feel free to reach out to us and we would be more than happy to answer.

Sincerely,

Peter Mantas

General Partner, Logos LP

Matthew Castel,

General Partner, Logos LP