Bonhoeffer Capital Management commentary for the first quarter ended March 31, 2019, proividing a case study of Ashtead Group plc (OTCMKTS:ASHT).

Dear Partner,

Bonhoeffer returned 4.0% net of fees in Q1 2019, compared to 10.5% for the MSCI ACWI ex-US, an international benchmark. As of March 31st, our securities have an average earnings/free cash flow yield of 20.0% and an average EV/EBITDA of 3.3. The difference between the portfolio’s market valuation and my estimate of intrinsic value is at one of the largest gaps since inception. I do not know when this gap will close but, over time, the gap should converge.

Q1 hedge fund letters, conference, scoops etc

As we settle into spring after a harsh winter in terms of both the weather and the financial markets, I am hopeful that the rest of 2019 will be more stable than the past six months.

Bonhoeffer Fund Portfolio Overview

Bonhoeffer’s investments have not changed significantly in the last quarter. Our largest country exposures include: South Korea, Italy, South Africa, Hong Kong, Norway, and Philippines. The largest industry exposures include: distribution, consumer products, telecom, transaction processing, real estate, and media.

Since my last letter, we have added to one position in an equipment rental firm. I am excited about some firms we are investigating in Mexico, Philippines, South Korea, and South Africa.

Local Businesses

Local businesses are a fertile ground for ideas in the internet age. One of the key advantages of internet businesses is scalability; and the market pays high multiples for this scalability. One area overlooked is less-scalable local businesses. These include dealerships/distributors (car and other equipment), local media (radio and TV stations), restaurants, homebuilders, and leasing businesses. These businesses require more employees and capital as they expand than internet firms do, but they also have valuable economies of scale. Many of these local businesses are going through a consolidation phase which can provide growth in a slow-growing mature market. Local consolidation typically generates real cost synergies and thus higher margins as these firms expand. Another important differentiation is capital-light or capital-heavy businesses. Capital-light businesses are nice in that growth from consolidation can occur with little additional investment. Capital-light firms have been the focus of Bonhoeffer to date.

An example of a local consolidating business is car dealerships. As dealers become larger, economies of scale of fixed costs (such as dealership upgrades and IT) across a larger revenue base increase margins. One key metric for car dealerships is inventory turnover. A dealer that can turn cars at a faster rate than competitors can charge a lower price than competitors and simultaneously generate higher returns on equity. High turnovers are the result of knowing what customers want and providing these cars to their customers faster than their competitors. Other key metrics for auto dealers include percentage of sales that are service, financing/leasing, or used cars. In each of these categories, the services have higher margins and returns on capital and lower volatility than new car sales and thus dampen the volatility associated with new car sales.

One issue for auto dealerships is the transition from internal combustion cars to electric cars. This transition will affect service revenue the most, as electric engines should require less maintenance than internal combustion engines. However, in Scandinavia, where electric cars have the highest penetration, the reduction in service revenue has not been observed. This may in part be due to the fact that, while the electric cars require less servicing, the customers use the dealer more than third-party providers.

Examples of high turnover dealerships in the Bonhoeffer portfolio include Cambria Automobiles in the UK and Combined Motor Holdings in South Africa. Both of these high-quality/high-ROE firms were purchased at very reasonable multiples of 8x and 6x earnings.

Another example of local businesses that are interesting are local radio/TV firms. Although the internet, YouTube, and Netflix are providing competition in the scalable part of the business, local content is still being primarily provided by local radio/TV. This local advantage has carved out a niche for these “dying” businesses. Both TV and radio firms receive cost synergies when they merge in a given market due to consolidation of back-end functions. In addition, local TV stations in the US have affiliation agreements which reset to the most favorable rates when an acquisition occurs. Local TV stations are now receiving re-transmission fees from cable companies. Since the stations own their spectrum, they can sell underperforming stations to other firms—thereby developing local clusters—and the local TV stations receive political advertising bumps every two years. Most small cable bundles also include local TV stations; this validates the value-add of local coverage of these firms.

A current example of this type of business is Gray Television. Currently, the firm is selling for 5.7x the projected next-two-years’ free cash flow despite almost doubling in value over the past six months. The firm has the largest collection of #1 or #2 market share stations in rural/suburban areas of the US and sells at 50% of the free cash flow multiples of its closest comparable, which is Nexstar Media Group. Gray Television does have leverage, but it is manageable. The current coverage ratio is 4.0x and Gray is rated BB by S&P. The debt currently yields 5%, and the free cash flow debt spread is almost 15% with a growing free cash flow yield.

In the capital-heavy type of local businesses, we have looked at equipment rental and homebuilders/developers. Ashtead, a recent portfolio addition, is an equipment rental firm that has the ability to moderate capital investment based upon demand, which makes it more like a capital-light business than a capital-heavy business. Homebuilders/developers are typically capital-heavy businesses with large land holdings. There are some homebuilders/developers, however, that have developed capital-light models, like NVR, Inc. in the US (which utilizes land options), Maisons France Confort SA in France (which builds houses after customers buy lots) and Shinoken Group Co in Japan (which sells completed homes to a realty fund). We are investigating these alternative models to find opportunities that fit with our capital-light preference in otherwise capital-heavy industries.

BCM Case Study

In past letters, I have laid out the theses of some of our holdings in the BCM Case Study section of our letter. In this letter, I am happy to present my thesis on the Ashtead Group plc—primarily a US-based equipment leasing firm—as this quarter’s case study.

As always, if you would like to discuss any of the philosophy or investments in deeper detail, then please do not hesitate to reach out. Until next quarter, thank you for your confidence in our work and have a fun spring.

Warm Regards,

Keith D. Smith, CFA

BCM Case Study: Ashtead Group PLC

Business Description

Ashtead rents construction and industrial equipment, providing various types of construction equipment for non-residential construction markets and facilities management equipment for the maintenance and repair of facilities. It also offers disaster relief equipment, power generation, lighting and other equipment, climate control equipment, scaffolding solutions, and portable traffic systems. It serves construction, industrial, and homeowner customers, as well as government entities and specialist contractors. Ashtead offers its equipment through 658 stores in 47 states in the United States, 54 stores in Canada, and 187 stores in the United Kingdom.

Ashtead is the largest equipment leasing firm in the UK and Canada and the second largest in the US. In the US and Canada, Ashtead operates under the Sunbelt Rentals name. In the UK, Ashtead operates under the A-Plant brand. The US business represents the largest portion of revenues at 87% and 92% of operating profit (EBITA).

Business and Service Analysis (The Power of Clusters)

The equipment leasing business in the US is primarily a local business servicing local and some national construction contractors, facility management firms, entertainment venues, and disaster relief organizations. Ashtead is organized around local “clusters.”

In local “clusters,” equipment is rented and used for construction, maintenance, or clean-up activities. The clusters are local networks of branches/locations working together to increase product selection and equipment density closer to client locations. Clusters typically include a large store with a focused product line, a group of smaller stores with a broader product selection, and specialty stores.

Ashtead has expanded via greenfield expansions and acquisitions in its local clusters that service its customers in each local area. In 2016, Ashtead developed a plan called the 2021 Plan in which the number of locations was to be increased from 546 (in 2016) to 900 (in 2021). Currently, Ashtead is ahead of schedule. Creating equipment density via clusters is a key part of the 2021 Plan. This plan was expected to result in an estimated organic growth rate of 15% per year (4% from market growth and 11% from increasing market share) but has generated about 16% per year so far.

Ashtead’s business plan is based upon developing and maturing clusters. For each cluster, Ashtead has a growth plan that is driven by a mix of the bolt-on acquisitions and greenfield growth. Ashtead’s growth is primarily generated by greenfield sites where Ashtead has high market share and by bolt-ons where Ashtead has low market share. Ashtead divides clusters into groups based upon maturity (early, mid-term, and mature). The current mix of clusters in the US is 49% mature, 31% mid-term, and 19% early. Initially, clusters have a high growth rate as Sunbelt expands in a given region. Typically, the initial customers are primarily construction firms (80%) and the EBITA margins are around 32% with pre-tax ROIs around 19%. As a cluster matures, more non-construction customers become larger parts of the customer mix and the economies of scale kick in. By the time the cluster is mature, seven years after launch, the construction customer mix is 40%, the EBITA margins are 41%, and the pre-tax ROIs are 29%. Two specialty areas of Ashtead’s focus—climate control and flooring systems—have only 54% and 37% penetration into Ashtead’s clusters, so increased penetration should continue to enhance revenue growth.

The largest firms in each cluster have both revenue advantages and cost advantages over smaller firms. The revenue advantages include wider equipment selection and more efficient sharing of equipment (utilization) within and amongst clusters which can result in higher “surge” pricing. The cost advantages include the fact that more revenue can spread across a semi-variable cost structure and equipment purchasing discounts. As the clusters grow, moats are being developed in each market. Technology is being used to enhance efficiency via the use of customer data that the largest players possess. IT use is a differentiator for large firms (such as Ashtead) which can use it to provide more targeted products and services and tracking of equipment than smaller firms. Clusters also facilitate more effective utilization/sharing of equipment within the clusters.

Ashtead is increasing product diversification by leasing climate control and flooring systems and increasing geographic diversification via the larger geographic reach. This is making Ashtead less risky as it grows.

A nice aspect of the cluster model is that, when new rental services are provided in a cluster, the incremental ROl is very high due to utilization of the infrastructure in each cluster. This leads to a situation where Ashtead becomes more profitable as it grows, and its moat also grows. Management has provided an example in the DC/Baltimore cluster, where climate control has EBITA margins of 49% and ROIs of 69%. Also, as these clusters mature, they are becoming more diversified away from construction; thus the overall cash flow of Ashtead is becoming less cyclical. This can be seen on a company level in the increase of Ashtead’s EBITDA margin from 38% at the last cyclical peak (2008) to 47% in the current situation (2018) and also in Ashtead’s ROI, from 14% in 2008, to 18% in 2018.

The equipment rental business in the US is a consolidating and fragmented market. The largest three providers have a 23% market share, with the next four providers having a combined 4% of the market. The US is a $63 billion addressable market. The overall equipment growth rate is 3% per year, but the rental growth rate has been closer to 5% per year as rental penetration in the US has been increasing. The current US rental penetration is 55%, versus 75% to 80% in more penetrated markets like the UK and Japan.

The 10-15% organic growth is supplemented by a historically determined 10% growth associated with accretive acquisitions and share buybacks. What is unique about Ashtead is the ability to re-invest cash flows at high rates of return into the core business via equipment purchases, greenfield location or tuck-in acquisitions, or via buybacks (if the stock price is low). Cash flows can be re-invested at the current level of pre-tax ROIs of 18%.

ROI can be decomposed into two components—EBITA margins generated from leasing of equipment and how many times the equipment is leased per year. Over the past five years, Ashtead’s EBITA margin has increased from 21.3% to 28.0% (the highest amongst its competitors), and the sales/PP&E have increased from 0.73 to 0.80. At the same time, EBITA margins and PP&E turnover have declined for United Rental (URI), Ashtead’s closest competitor.

Ashtead also has the highest BV and dividend at 36%, sales and earnings growth rates at 36%, and ROIs amongst equipment lessors. This is, in part, due to the consolidating market and the cluster strategy described above. The other large equipment lessor in the US (URI) also has strong growth and ROE numbers from the consolidating North American market.

Equipment Rental Business

In the US market, Ashtead has an 8% market share which has doubled since 2007. Ashtead has a goal of a 15% market share by 2021. URI is the largest firm, with a 12% market share. Herc Rentals has a 3% market share, HD Supply has a 2% market share, and 1% each for Ahern Rentals and BlueLine Rental. Recently, URI has gained market share via large acquisitions, and Ashtead has grown via tuck-in acquisitions. In the Canadian market, Ashtead has a 3% market share, with a goal of a 5% market share by 2021.

In the UK market, Ashtead has the largest market share at 8% and has a target of 12% by 2021. Other market participants include HSS Hire at a 6% market share, Speedy at a 6% market share, Vp plc at a 4% market share, and GAP Group at a 4% market share.

What makes the US market different from other markets such as Europe and Japan? The US market has some nice characteristics versus other markets, namely its low rental penetration of 55% versus 75-80% in Japan and the UK, and the unconsolidated nature of the market (20% market share in the top two companies and 4% market share in the next four largest competitors). If the US penetration approaches the UK’s and Japan’s over the next ten years and the market grows at GDP levels of 2-3% per year, then a sustainable 6-7% revenue growth is attainable in the US market. Given the economies of scale of the larger players and the augmentation of additional rental services like climate control and flooring, it is possible to pick up an additional 8-10% growth per year as Ashtead has versus average rental revenue growth over the past five years.

If we look at more penetrated and consolidated markets (such as Japan), then the growth rates are more dependent upon penetration and market growth versus gains in market share. Even in the slow-growing markets, double digit ROEs and BV plus dividend growth are currently being achieved.

Since construction is the largest portion of Ashtead’s revenue (40%), the construction industry is an important driver of Ashtead’s cash flows. According to “2019 FMI Overview,” the US construction put in place is expected to grow by about 3% per year over the next five years. It has grown by 7% per year over the past five years. This slowdown would reduce Ashtead’s historical growth rate by about 5% over the next five years to a rate closer to 17%.

Downside Protection

Modest leverage allows for aggressive share repurchases if share price declines dramatically. Ashtead has a debt level of 2.8x EBITA versus 5.1x for URI. Another nice aspect of equipment leasing is that, when a slowdown occurs, the leasing firm can cut back on capital expenditures and generate large amounts of free cash flow which can be used to repurchase shares if the firm is not too levered. This can be seen in the free cash flow from 2008 to 2010 in the historical financial profile below. In addition, JP Morgan estimates that Ashtead would generate ₤1 billion in a downturn in the next few years because of this characteristic. The contracyclical aspect of the business allows a modestly levered firm to either buy its struggling competitors or buy back a meaningful portion of the firm’s equity.

Although Ashtead is in a cyclical business, it has defensive characteristics. These include the contracyclical cash flows and the increasing returns to scale described above. Another way to look at Ashtead is as a specialized financing firm that has operational and balance sheet advantages which protect it from bank competition. In many capital equipment firms, the financing arm is the most profitable.

Management and Incentives

Historically, Ashtead has been led by UK management, but the person in line to become the CEO is the current head of Sunbelt Rentals, the US subsidiary of Ashtead. Ashtead management has incentives tied to pre-tax profit for the CEO and operating profit for the heads of Sunbelt and A-Plant, total shareholder return, return on investment, and earnings per share growth and leverage. The targets for these incentives are: total shareholder return (median to upper quartile of competitors), 6-12% earnings growth, a pre-tax return in investment of 10-15%, and a leverage ratio of less the 2.5x EBITDA.

Brendan Horgan is the current CEO of Sunbelt and is in line to become the next CEO of Ashtead. The management team owns a material amount of common stock directly which ranges from 2.8x to 11x their

salaries. The current CEO (Geoff Drabble) and the CEO-to-be (Brendan Horgan) directly hold 392,219 shares (a value of ₤8.1 million pounds) and 318,874 shares (a value of ₤6.6 million pounds), respectively.

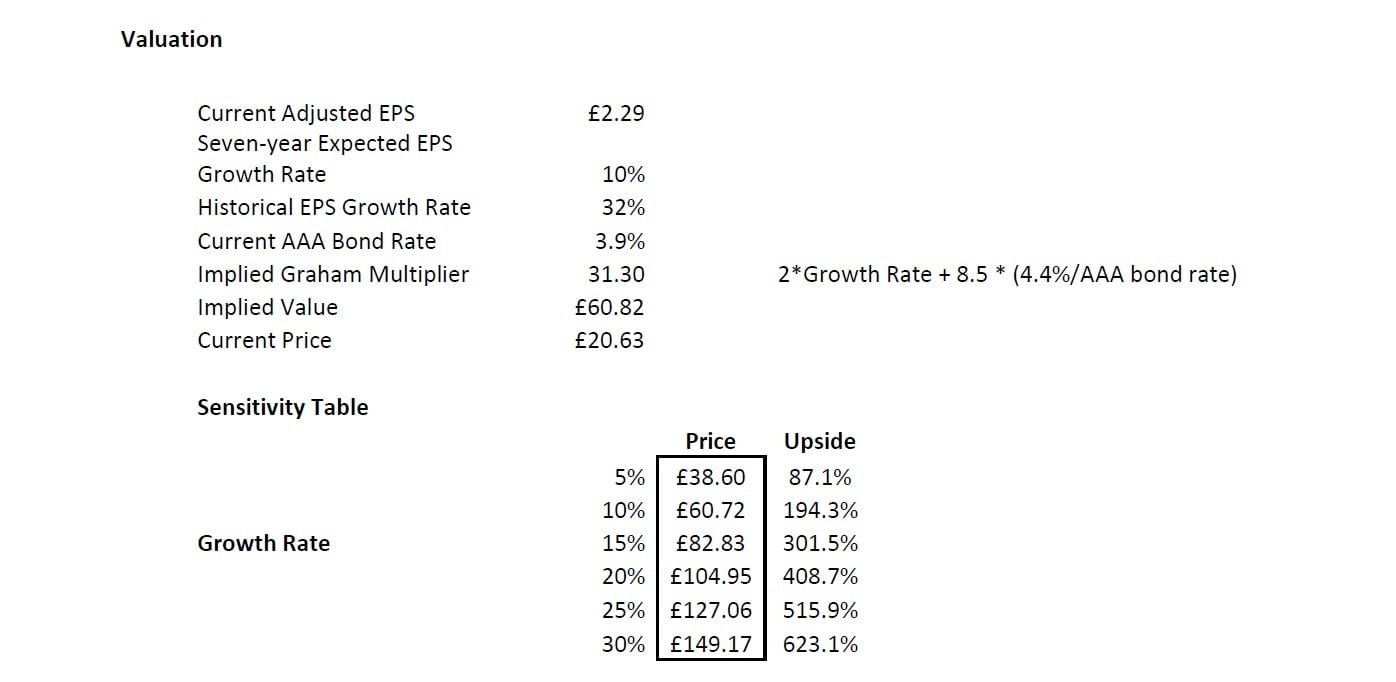

The valuation of Ashtead is an interesting exercise because of the fact that is has higher growth and margins than most all of its competitors due to the clustering strategy described above, the characteristics of the US market, and its position as a large player in the US market. The implied growth using the Graham formula adjusted to today’s interest rates ((8.5 + 2g)*(4.4/AAA bond rate)) and the current P/E is -0.3%, clearly implying a mispriced security. Some historic benchmarks for growth are the historic EPS and BV and dividend growth rates of 32-35% or the five-year average ROE of 33%. The firm has a goal from its 2021 growth plan of growth of earnings of 20%.

The question is whether this growth rate is sustainable over the next five to seven years. Given the history of outperformance and the remaining penetration potential of US markets, I think the 20% growth is sustainable. If 20% is used in the Graham formula for seven years of future EPS growth, then the resulting P/E is 54.1x. If we reduce the growth rate to 15%, then we get a multiple of 42.7x. Now if we reduce the growth to the market revenue growth rate of 5%, then we get 19.9x, almost double from the current price. Two firms that have similar historical growth to Ashtead are Sixt and AMERCO. Both of these firms trade at an earnings multiple of almost 20x. So a 20x multiple on ₤2.29 EPS yields a value of ₤46, which I believe is a reasonable 12-month target. If, over the next five years, a 15% EPS growth is attained, then the earnings will be ₤4.60. Applying a 17.6x multiple to these earnings (implying a 4% growth rate over the subsequent seven years) then a value of ₤80 is obtained. This results in a five-year IRR of about 30%.

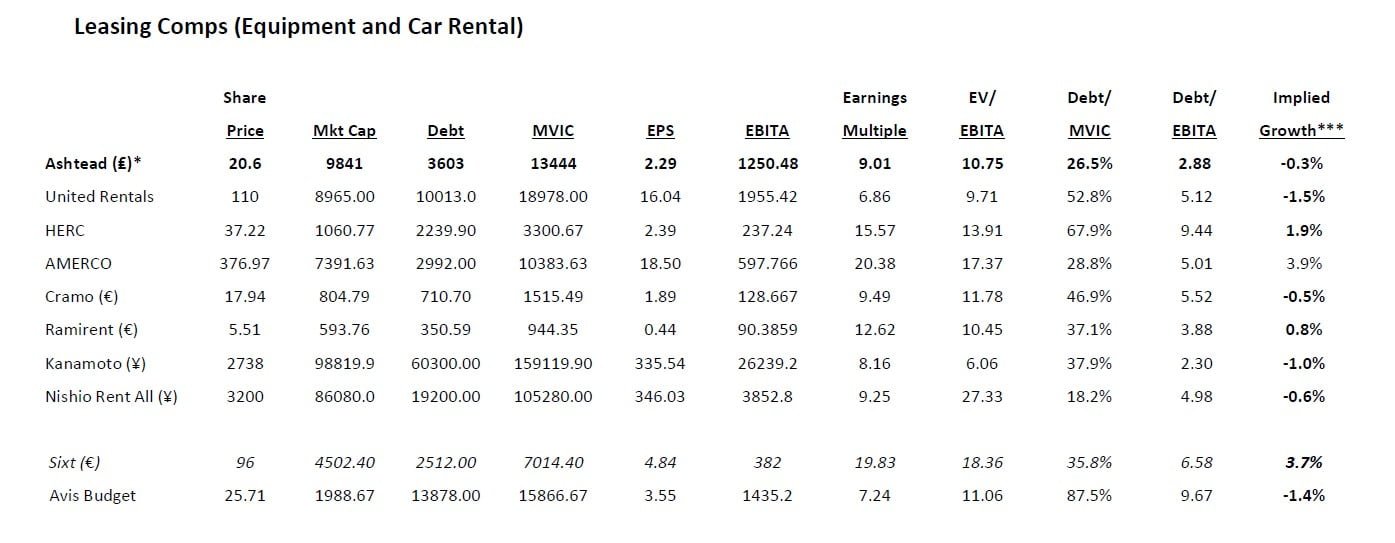

Comparables

The following represents both international and related leasing group (car leasing) comparables. One item to note is the valuation of firms in lower growth markets (Japan and Europe), as these are the valuations that Ashtead should trade at after the period of high growth/consolidation over the next seven to ten years.

Benchmarking

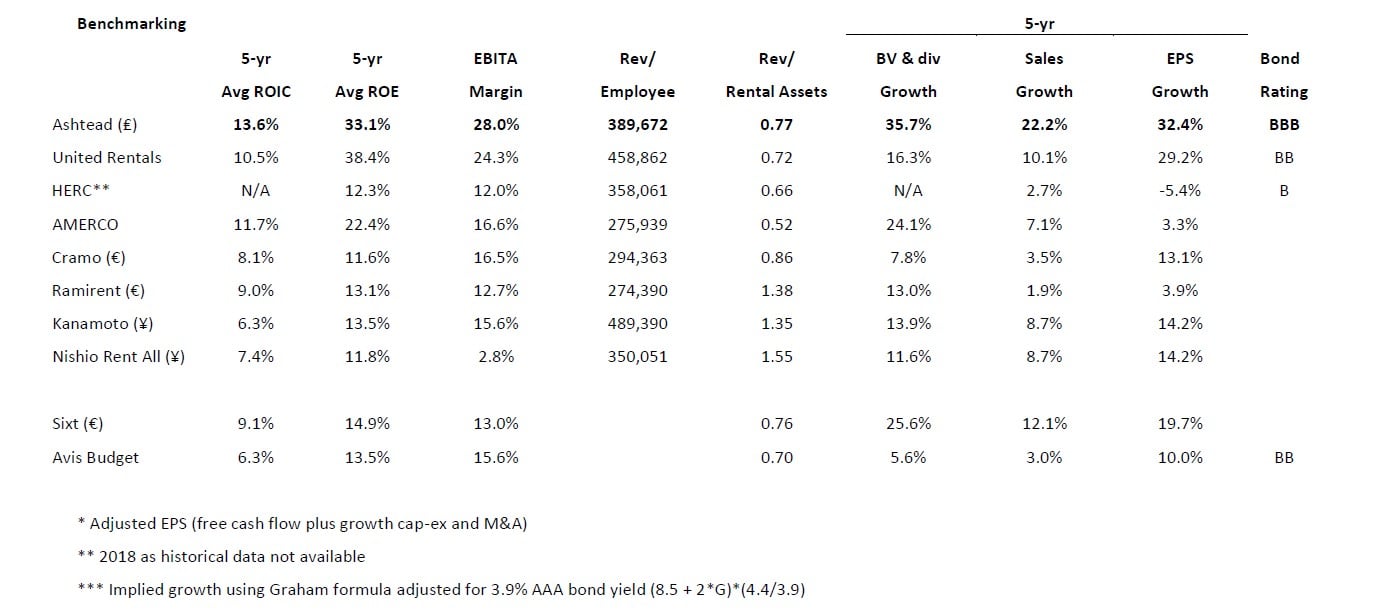

In comparison to other publicly traded equipment leasing firms, Ashtead has the highest ROIC and EBITDA margin and growth rates. The growth rates have occurred in an environment of high construction growth in the US of 7% versus a projected rate of construction growth of 3%. Lower growth rates for construction will reduce Ashtead’s growth rates by about 5% to a range in the high teens. Ashtead also has the lowest ratio of debt to EBITA and thus is the least leveraged. The lack of leverage provides Ashtead with opportunities to either acquire competitors when a slowdown occurs or buy back more stock than more leveraged competitors. The low leverage also allows Ashtead to have the youngest fleet amongst its peers.

Risks

The primary risks to achieving a target valuation of ₤46 per share for Ashtead include:

- A slowdown in the US construction market

- A large cyclical downturn which would reduce the equipment leasing firm multiple

Potential Upside/Catalysts

- An upturn in the US construction market due to US infrastructure spending

- Continued increase of scale in the UK and Canadian markets

- Addition of more specialty products to lease such as flooring and climate control systems

Timeline/Investment Horizon

The short-term target is ₤46 which is double today’s price. I think the investment thesis can play out over the next three to five years. By this time, Ashtead’s net income and earnings should have appreciated by at least two times and the fair multiple could double with a 5% increased growth rate. If that is the case, then Ashtead will be an almost 4.0x return to ₤80 over five years. This is similar to a “Davis double” where both underlying earnings increase along with the fair value multiple.

This article first appeared on ValueWalk Premium