McIntyre Partnerships letter for the first quarter ended March 31, 2019.

Dear Partners,

I hope you are having a pleasant start to spring. Below I provide an analysis of GTX’s asbestos indemnity, which is the fund’s largest position. However, as I prepared to distribute our letter this morning, an interesting development came out in Honeywell’s 10-Q:

[klarman]Q1 hedge fund letters, conference, scoops etc

In our ongoing communications with Garrett with respect to the Agreement and Garrett’s associated material weakness disclosure in its Form 10-K for the year ended December 31, 2018, Garrett has taken the position that (i) Honeywell has not satisfied all of its obligations under the Agreement, and (ii) the Agreement is unenforceable either in whole or in part.

It appears GTX has challenged the indemnity in some form. While the outcome is far from clear, it highlights the wide discrepancy between the Street’s overly punitive estimates and the fund’s view on eventual payouts.

A man must believe in himself and his judgment if he expects to make a living at this game.” – Edwin Lefèvre (Jesse Livermore)

Performance Review – Q1 2019

Through Q1 2019, McIntyre Partnerships returned approx. 14% gross and net. This compares to S&P 500 and S&P 600 returns including dividends of 14% and 11%, respectively.

The partnerships started 2019 on a strong note but pulled closer to a market performance following our March returns. However, in the time it took to finalize our March numbers, the fund had already “made back” our March “loss,” which highlights why I consider monthly numbers noise which should be taken with a grain of salt. Several of the large cyclical bets I placed in the second half of last year have begun to show results. As I believe the stocks still present significant upside with limited risk of long-term loss, I have maintained our positions and, in some cases, added.

In Q1, CC and LILAK each contributed >500bps of PNL, while CBS/DISCA, GTX, and FBHS produced ~100-300bps each. Excluding hedges, our only >100bps loser in Q1 was Permanent TSB, which lost ~100bps.

Portfolio Review – Exposures and Concentration

As of March end, our exposures are 133% long, 34% short, and 99% net. Our five largest positions were 89% gross exposure and our ten largest were 124%.

Our five largest positions are GTX, CC, LILAK, FBHS, and uranium.

International stocks and uranium account for 27% of the portfolio. Non-cyclical businesses (cable, beer, cell towers, etc.) are 57%. “Hard catalyst” (spinoff, merger, asset sale, etc.) and “soft catalysts” (earnings beats, price increases, etc.) stocks account for 56% and 59%, respectively.

Portfolio Review – Existing Positions

SMTA

In January, SMTA reported mixed news. SMTA’s largest tenant, Shopko, filed for bankruptcy. In the nine months prior to bankruptcy, SMTA had successfully monetized significant value in Shopko, providing downside support, but the bankruptcy effectively removes the 200% upside bull case I had targeted. However, the filing accelerated the timeline for SMTA to realize value in the remainder of its portfolio, and the company has announced they are pursuing strategic alternatives. Rather than a three-year liquidation play, SMTA is now a risk arb play with a resolution likely sometime in 2019.

From here, the upside thesis is simple, and I believe probable. Spirit now has three assets: cash, a small portfolio of distressed assets, and the equity tranche of the Master Trust (MTA). The cash and distressed assets are worth roughly the value of the SMTA’s liabilities, and the MTA will determine shareholder returns. The MTA has ~$180MM in NOI from a triple-net portfolio where the assets are individually worth a tighter than 7.5% cap rate and maybe tighter than 7.0% – the portfolio was appraised at a 6.75% when spun last year and triple-net rates have tightened since then. A 7.5% or tighter cap rate yields a 40% or greater return on SMTA. It’s worth mentioning that the Master Trust funding structure, which many equity analysts view as a substantial negative, could be unwound promptly for ~$60-$70MM in prepayment penalties, enabling the portfolio to be sold in pieces if no buyer emerges for the entire trust.

On the downside, if no buyer emerges, SMTA’s stock is likely to react poorly, probably falling 10-30%. The question is then “what do we own without a buyer and would we want to own it at that price?” In the event of no deal, SMTA is likely to pay off their preferred equity and buyout their (overpriced) management contract with their former parent (SRC). Depending upon the new management contract, I estimate ~$1.40-$1.60 in pro-forma AFFO/share. The MTA’s structure has an amortization payment that cuts the cash available for distribution (CAD) to $0.75 in 2019; however, the amortization drops substantially in H2 2020 bringing CAD closer to a $1.50/sh. run rate. At the low end of my downside range, a ~30% fall yields a share price of ~$4.70, or ~3x run rate CAD. Beyond that, the event path is less clear. SMTA will be highly levered, financials will be messy, the MTA works better as a growing portfolio than a dividend play, etc. But I believe 1) you will likely receive $2-$3 in dividends in the next three years and 2) management will continue to seek an eventual deal and/or unwind the portfolio even if no deal transpires this year. Given the substantial dividend and optionality to sell the assets at a later date, I am comfortable with the downside.

GTX Asbestos Liability

GTX shares have rallied since we began purchasing them last year, and I roughly doubled our position in Q1. The outlook for autos has not crashed as feared and the market seems to better understand the GTX story. However, I believe GTX’s asbestos liability remains widely misunderstood. The market is overestimating the indemnity’s bankruptcy risk and a substantial discrepancy remains between sellside/buyside estimates and probable payouts. In addition to autos broadly rallying and GTX closing the valuation gap versus peers, I believe a better understanding of the indemnity and lower than expected payments represent a third catalyst for GTX shares to rally.

I believe the misunderstanding boils down to two major issues:

- The liability payments are capped annually and deferrable, thus the indemnity is similar to a preferred equity and cannot cause a covenant breach or bankruptcy

- Investors are overestimating the probable annual payments

The most important detail of the indemnity is that it is capped at $175MM annually and, in the event GTX’s financials deteriorate, the payment can be deferred indefinitely at a reasonable 5% interest rate, thus it cannot cause bankruptcy*. The indemnity is close to a preferred equity, where we are taking long-term risk that the liability will limit cash flows to equity holders, but we are not taking short-term or cyclical risk where a sudden downturn in GTX’s operations results in the inability to pay interest and/or repay loans resulting in bankruptcy. GTX screens as having ~4.5x net leverage and ~2.5x interest coverage. (For reference, my numbers are ~$650MM in EBITDA, ~$3B in net debt and liabilities, ~$55MM in interest, $175MM in “worst case” asbestos liabilities, and ~$20MM in other liabilities.) However, the asbestos liability accounts for ~$1.4B and ~$175MM in liabilities and expenses. For “bankruptcy relevant” metrics, GTX is a more reasonable ~2.5x net leverage with ~9x interest coverage – elevated but I believe a manageable level given GTX’s variable cost structure, above cycle growth, and strong cash conversion.

Finally, I believe analysts are substantially overestimating the asbestos liability’s overall size and annual run rate. Most sellside analysts simply take the $175MM payment and project it indefinitely into the future. However, this is a worst-case scenario – GTX can only “beat” the Street. I believe current run rate annual payments are closer to ~$135MM and will decline towards ~$100MM-$130MM by 2022. As the indemnity payment is a post-tax liability, 100% of the difference between analyst assumptions and probable payments will drop to FCF, which yields $0.60-$1.00 in additional FCF/sh. by 2022 vs. a current price of $15-$19/share.

There’s a lot of “noise” around the indemnity – GTX is a spin, HON wrote up the liability into the spin following an SEC inquiry, GTX doesn’t have “effective internal control” over the liability, etc. However, looking through the noise, the annual asbestos liability is a simple calculation:

[(Claims Resolved x Average Payout Per Claim) – Insurance Recoveries + Legal Fees] x 90%Note: Honeywell pays 10% of the liability

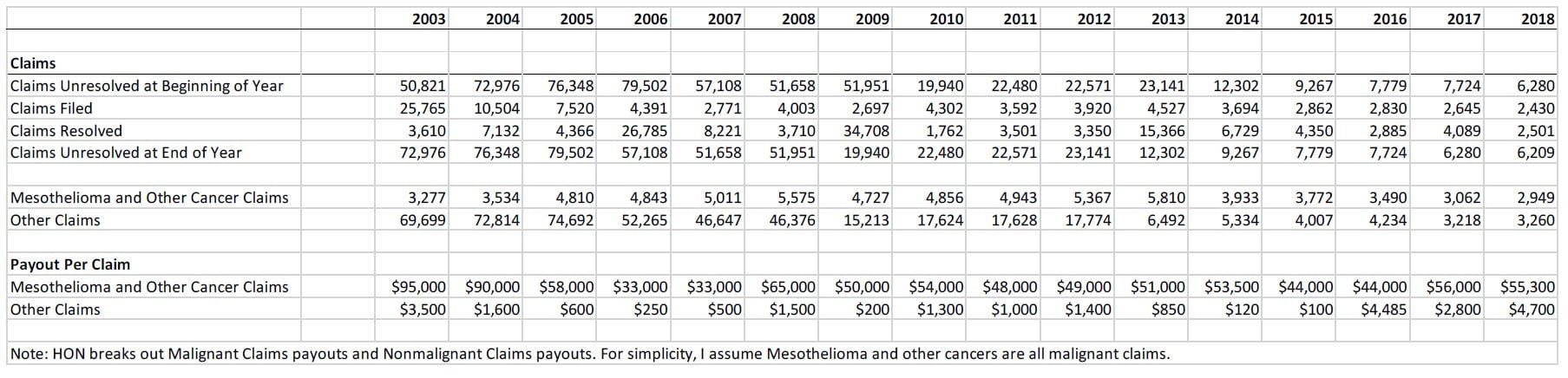

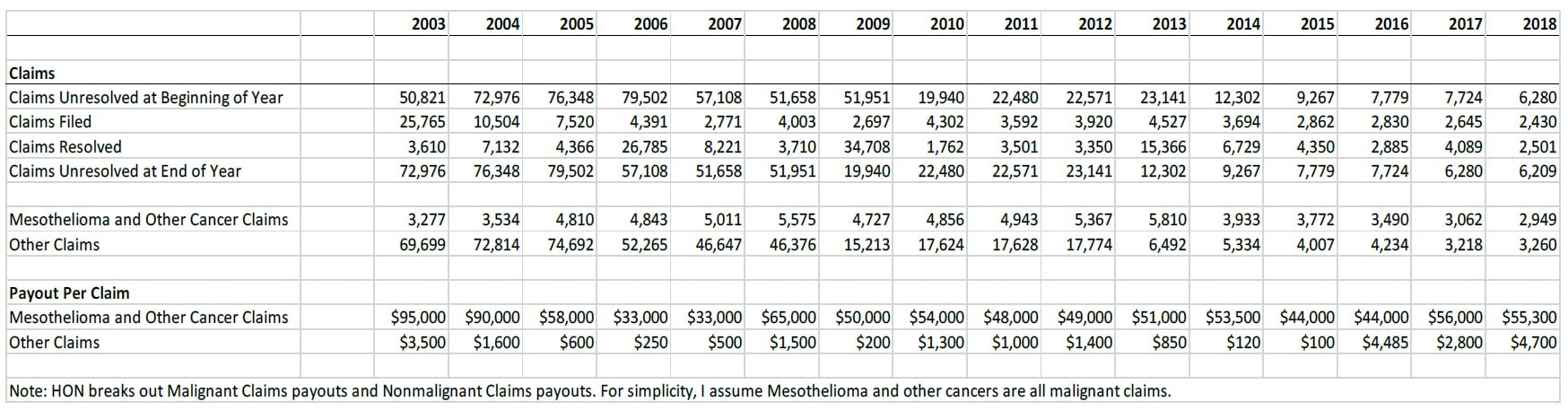

Here are the relevant metrics since 2003 from HON’s 10-Ks:

If that is difficult to read, the table is provided in landscape mode at end of this letter. Also, to simplify the calculations below, I assume that insurance settlements are minimal and that the legal fees and 10% contribution from Honeywell roughly equal each other.

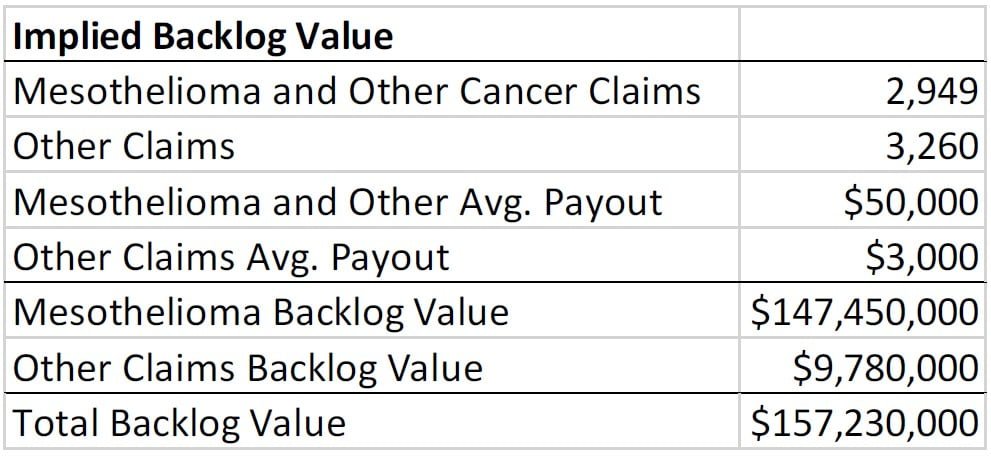

The total liability is then the sum of 1) the backlog of existing claims and 2) any new claims filed. For the backlog, I take the claims already filed and multiply by recent average payouts to reach ~$157MM. I assume this backlog gradually settles towards zero over the next ten years adding ~$16MM in annual expense. This compares to 2019 EBITDA-capex of roughly ~$550-$600MM.

Next we must calculate future claims. For conservativism, I estimate all new Claims Filed will be for higher payout mesothelioma cases. Claims Filed have fallen from ~4,000 per year from 2006-2013 to ~2,400 in 2018. At present run rate, that implies roughly ~$120MM per year – 2,400 cases x $50,000 per case. Adding that to our $16MM of backlog expense above yields ~$135MM in annual run rate asbestos expense, which is consistent with the actual payments over the last three years. However, I believe the rate of new claims will continue to fall. HON/GTX are being sued over asbestos brake pads which were pulled in the early 1980s. While it’s never clear exactly what caused someone’s mesothelioma, persons exposed to these brake pads with enough frequency for HON/GTX to be at fault are likely well into their 70s and 80s and will begin to die of other causes without the disease developing. I estimate new claims filed will fall towards ~2,000 per year by 2022, yielding roughly ~$115MM per year including backlog. While the ultimate total size of the payout is unclear, I believe these payments will likely “cliff” sometime in the next ten years towards a sub-$50MM run rate.

*In theory, the presence of the liability could contribute to a bankruptcy via its impact on credit or counterparty sentiment. For instance, the debt markets could worry about the liability and refuse to roll over GTX’s debt. However, I view this as a remote possibility and GTX has no debt due until 2023.

Portfolio Review – New Positions

The fund has begun to acquire shares in an illiquid security and targets a large position. I will update investors once we have reached our targeted size. What I will say is that the position meets our risk/reward metrics: a strong balance sheet that limits long-term loss of capital and a strong liquidity event to reach a 50-150% upside in the next two years.

As always, please feel free to contact me with any questions.

Sincerely,

Chris McIntyre

This article first appeared on ValueWalk Premium

{kind=link}