In August, the hedge fund industry had its second consecutive month of inflows in H2 2018, and this time the breadth of allocations was much improved. Despite the improvement, it has by no means been a universally beneficial period.

Q2 hedge fund letters, conference, scoops etc

Macro products, so far, seem relatively impervious to bouts of performance declines, while managed futures funds continue to carrying the weight of February’s large losses. Credit funds are in investors’ favor, and event driven strategies rebounded, but emerging market managers are increasingly facing their own negative financial impacts of the trade wars, and strong USD to EM currencies.

Investors have shown a willingness to stick with themes, both positive and negative, but also to change direction quite quickly. How the rest of the year will play out given some recent macro performance slips, and these investor tendencies, is a difficult guess.

Highlights

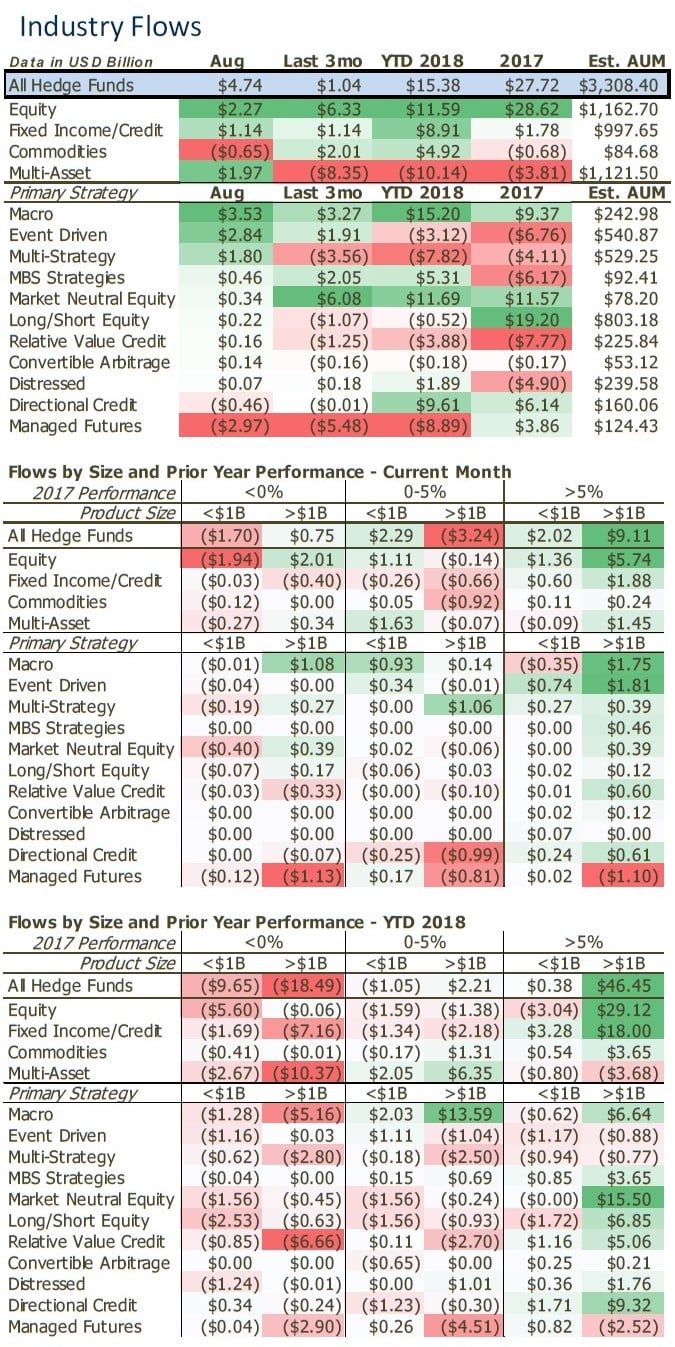

- Allocations continued to trickle into hedge funds in August. Investors added an estimated $4.74 billion.

- Investors resume allocating to macro strategies in the face of performance difficulties.

- Event driven funds saw a spike in allocations in August.

- Investor sentiment to managed futures was negative for a sixth consecutive month.

- Emerging market fund redemptions continue into a third month, nearly 60% of products with outflows in 2018.

Allocations Continue to Trickle Into Hedge Funds in August

Investors added an estimated $4.74 billion into hedge funds in August bringing YTD net flows for the industry to $15.38 billion. Total estimated hedge fund assets are now $3.308 trillion.

Key Points

- Investors allocated across a broader selection of funds in August.

In the months prior to August, a relatively low proportion of funds were receiving new assets, which is a sign of low participation. In four of the five months since February, prior to August, a well below average proportion of products were receiving new allocations, which is somewhat of a concern for the health of the industry. Despite the low overall net inflow in August, the breadth of allocation is a spot of good news. - Investors resume allocating to macro strategies despite, and in the face of, performance difficulties.

Macro funds produced three consecutive months of asset-weighted performance declines ending in April. Three months later they had their second monthly outflow of 2018. In July they produced losses again, and in August asset-weighted losses rose meaningfully. Despite the earlier losses, and in the face of current losses, macro strategies resumed their asset-raising success. - Managed futures funds face sixth consecutive month of redemption pressures.

2018 has been a tough year for managed futures products, and there is no need to reiterate that point in different ways each month. One positive note, asset weighted returns in August were their highest since January. Investors sitting on the fence, whether currently invested or not, and considering redeeming, staying, or allocating, may look to these months of outperformance for reasoning. If only the strategy’s losses in February could have been avoided, an argument in their favor would be much easier to make. - Event driven funds saw inflows jump in August, a rarity for the group in recent years.

There have been some high profile drawdowns in the event driven space over the last two years. As a result, it has been a long time since any sustainable aggregate interest has been shown toward the universe. June and July saw very light outflows, and investors allocated the most they have, on a net basis, to event driven funds in August since August 2017. Of all strategies, event driven had the broadest level of inflows during the month with 70% of funds receiving new allocations. - Credit strategies earned new allocations in 2018, but are they earning future allocations?

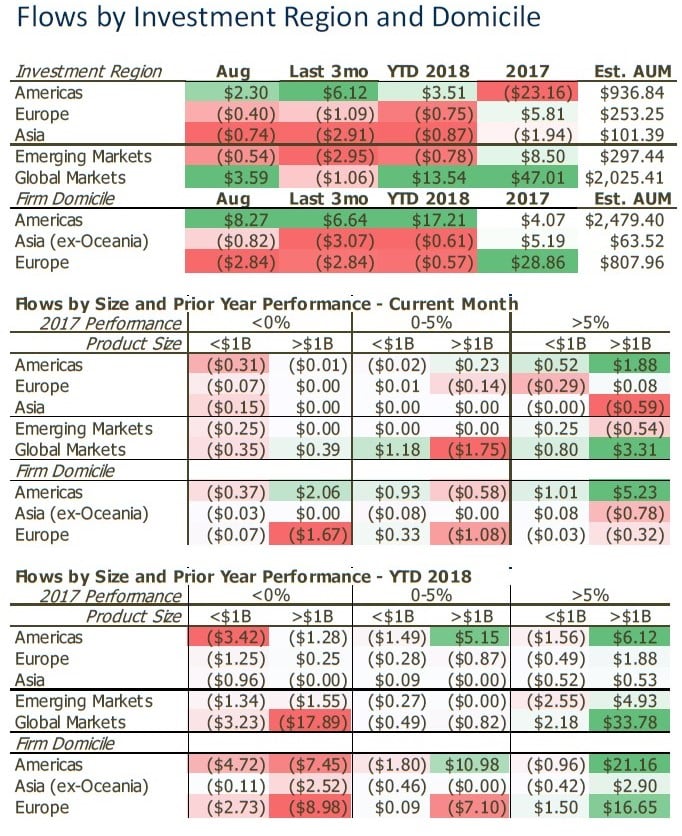

After a string of performance losses ended in March 2016 resulting in meaningful outflows, credit hedge funds went on to produce nearly two years of consecutive monthly performance gains (22 of 23 months). It took a long time for aggregate inflows to return, but they have in 2018. After a good start to the year, asset-weighted returns have been mixed. However, there is plenty of good performance being produced outside of difficulties in emerging markets.

Redemption Pressures for Emerging Markets Funds Enters Third Month

Key Points

- A strong US dollar and global trade policy has hurt EM returns and investors’ sentiment.

This is the exact same bullet point headline as last month, and it continues to hit the nail on the head. A clear example of the sharp turnaround managers have faced; the ten managers with the largest redemptions in August have returns an average of -12.4% in 2018. These same ten returned an average of +32.3% in 2017. - After three months of redemption pressures, most EM managers now have net redemptions for 2018.

Yes, August was a tough month. Nearly 70% of EM managers saw outflows in August, and now nearly 60% of EM managers have YTD net outflows. Despite the primarily performance-related outflows, pockets of interest remain. Some investors continued to allocate to China fixed income strategies in August, and if products have been able to avoid market-like losses during the recent downturn, investors appear to have rewarded them for it. The remainder of the year will be telling of how well managers are able to position current losses in the context of future opportunities.

Article by eVestment

{kind=link}