LISI Market comment for the month of June 2018, titled, “Just-In-Time Tapering.”

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

Summary Points

- The globally coordinated monetary accommodation machine that led to broadly distributed economic growth since the Great Recession is beginning to slow, and with it that pleasant purr of running engines has given way to the sputtering sounds of wear and tear. Blame volatility on the bumpy road of trade spats and geopolitical risk if you must, but the major central banks are beginning to tighten policy

- The "tapering" of Quantitative Easing (QE) programs appears finally to be gaining traction. Coupled with modest steps to increase policy rates, the fine tuning seems to mimic the innovative "Just-in-Time" inventory management strategies that led to industrial efficiency improvements in the 1970s and 1980s

- Worries about trade and rising protectionism have weighed on equity markets since their January peak. Building troubles in Emerging Markets assets are also giving investors pause. Combined with interest rate uncertainty these have ushered in a sideways range in major developed country equity markets. Strong corporate earnings in early 2018 have tamed the formerly high P/E ratios, a healthy contraction we expect to continue in coming months

- Bounding toward the third quarter, the US markets seem to shrug off every threat as fiscal stimulus and an accommodative monetary stance keep the economy humming along with decades-low unemployment, tame inflation and improving corporate earnings. Still, vacillating late-cycle inflation drivers in the US have prompted a data vigil to predict how far and how fast the Fed will hike rates.

- The Fed wants to create a sufficient buffer between the Fed Funds rate and zero in order to allow for stimulative maneuverability if needed. We see one more 0.25% hike this year, possibly two, but data such as hourly wages are stubbornly resistant to the expected upward pricing pressure that should accompany a sub-4% unemployment rate not seen since the height of the dot-com boom

- The US 10-year Treasury Note breached the 3.0% yield for the first time since January 2014, yet it subsequently moved down with the Euro-jitters resulting from an overleveraged Italy. While the Fed's Balance Sheet Normalization Program navigates uncharted territory with simultaneous monetary tightening actions, the Fed has cautiously allowed its holdings to decline only modestly from $4.5 trillion to $4.4 trillion since September

- Perhaps it is appropriate that a long, shallow economic recovery should follow the most jarring and profound economic downturn since the Great Depression. The successful QE experiment may now be approaching an end. We remain optimistic about equities for the remainder of 2018, barring some major shock. While the US stock markets continue their leadership as the fiscal boosts of tax cuts and deregulation filter through to corporate bottom lines, we are watching the international economic environment for signs that the lattice of mutual support among major markets begins to weaken

- It remains to be seen whether the calipers of monetary policy tools continue to run in just-in-time mode if damaging trade wars emerge or if other expansion threatening situations come into play. Given the reasonably stable current economic and market conditions, the LISI Investment Committee at its late May meeting decided to maintain its current Tactical Asset Allocations

The globally coordinated monetary accommodation machine that led to broadly distributed economic growth since the Great Recession is beginning to slow, and with it that pleasant purr of running engines has given way to the sputtering sounds of wear and tear. Blame volatility on the bumpy road of trade spats and geopolitical risk if you must, but the major central banks are boosting their efforts to head off potential inflation. Notably, the "tapering" of Quantitative Easing (QE) programs appears finally to be gaining traction. Coupled with modest steps to increase policy rates, the fine tuning seems to mimic the innovative "Just-in-Time" inventory management strategies that led to industrial efficiency improvements in the 1970s and 1980s. Here, though, interest rates, reserves and a few policy tools comprise the inputs to be optimized. One can hardly complain, given how successfully the globally coordinated liquidity has guided the long recovery, now the second longest on record. We may soon need a new term to replace "late-cycle" to describe the longevity of the recovery, maybe "late-late cycle."

Worries about trade and rising protectionism have weighed on equity markets since their January peak. Building troubles in Emerging Markets assets are also giving investors pause. Combined with interest rate uncertainty these have ushered in a sideways range in major developed country equity markets through May, after strong performance in the second half of 2017. Still, bounding toward the third quarter, the US markets seem to shrug off every threat as fiscal stimulus and an accommodative monetary stance keep the economy humming along with decades-low unemployment, tame inflation and broadly improving corporate earnings. European and Japanese economic growth continue, though with somewhat diminished strength despite continued low policy rates, while sharply positive confidence surveys and manufacturing data in 2017 have now rolled over. Vacillating late-cycle inflation drivers in the US have prompted a data vigil to predict how far and how fast the Fed will hike rates.

Given the reasonably stable current economic and market conditions, the LISI Investment Committee at its late May meeting decided to maintain its current Tactical Asset Allocations.

1. Central Banks: Nascent Contraction of Balance Sheets Underway

The US Federal Reserve has hiked US interest rates consistently, if slowly, over the last 18 months, from near-zero to its current 1.50%-1.75% (prior to the expected hike to 1.75%-2.00% at its June 13th meeting). We see one more 0.25% hike this year, possibly two, but data such as hourly wages are stubbornly resistant to the expected upward pricing pressure that should accompany a sub-4% unemployment rate not seen since the height of the dot-com boom.

Still, the Fed wants to create a sufficient buffer between the Fed Funds rate and zero in order to allow for stimulative maneuverability in case of economic downturn. At the same time, the Fed Balance Sheet Normalization Program navigates uncharted territory with simultaneous monetary tightening actions. One big question centers on whether the rate hikes and QE wind-down can be managed appropriately to avoid over-tightening.

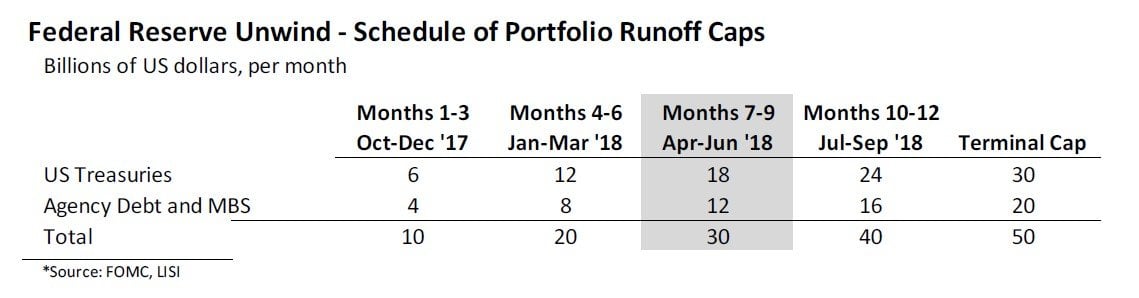

The normalization program is now in its third trimester, and the size of the assets allowed to mature without reinvestment is beginning to grow (see table below).

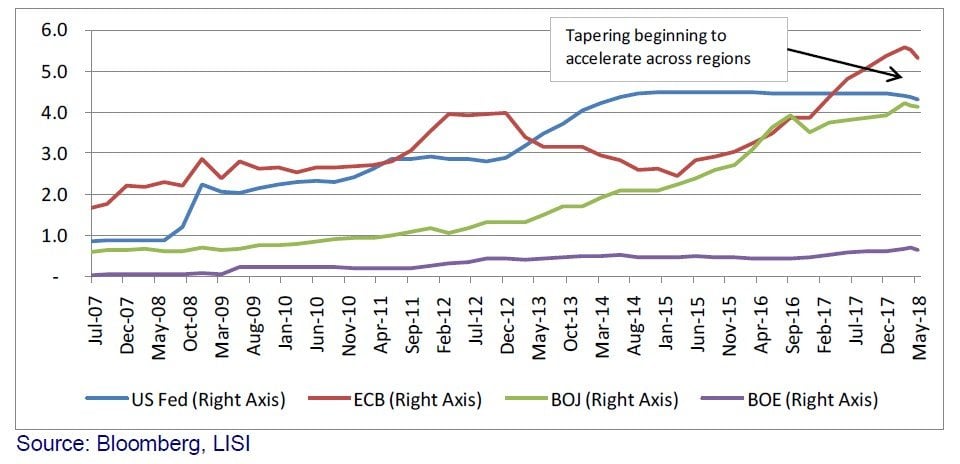

The Fed balance sheet has hovered at about $4.5 trillion over the last few months despite the normalization program. This has happened though Fed purchases of assets to offset the reduced levels of US Treasury note/bond and Agency/MBS holdings. By the end of May the balance sheet was $4.4 trillion (Treasury notes/bonds dropped from $2.5 trillion in September 2017 to $2.4 trillion in May 2018, while Agency/MBS fell from $1.8 trillion to $1.7 trillion). Perhaps the cautious moves reflect the Fed's intent to apply the tapering calipers judiciously, in just-in-time fashion. We expect the drop in UST/Agency/MBS holdings to accelerate later this year, as well as reduction in the overall balance sheet. At the same time, the European Central Bank appears to have recently taken an even stronger approach to reducing its balance sheet (see chart below).

Major Central Bank Balance Sheets, 2007-2018 (US$ Trillions)

2. US 10-Year Treasury Notes Breach 3% Level

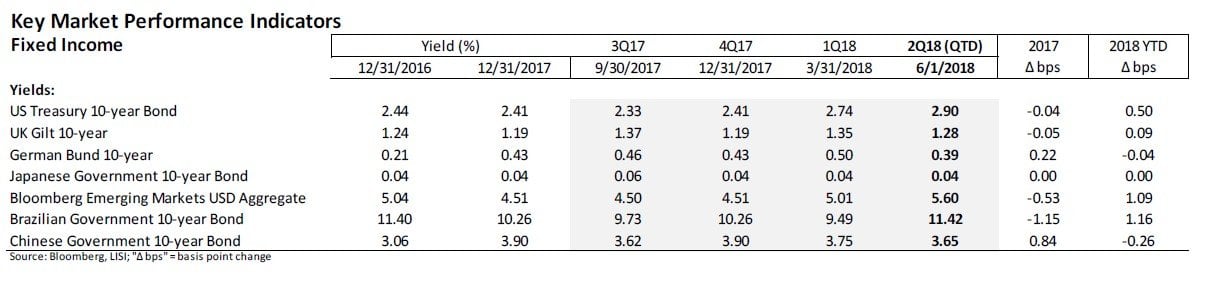

Fixed income markets have been waiting for the yield of the US 10-year Treasury Note to breach the 3.0% level for some time now, especially in the wake of the succession of Fed rate hikes that started in December 2015. The new FOMC under Chairman Powell, feared by many to instill a hawkish stance, has proven to be as watchful of and maybe wary of data readings as previous committees under Janet Yellen and Ben Bernanke. That 3.0% yield was hit in May, for the first time since January 2014. Yet it subsequently moved down with Italy-driven volatility (see table below). As of this writing the rate appears ready to settle above 3.0%, particularly in light of the near certain further rate hike on June 13th. Meanwhile, among the major developed market issuers only the UK offers greater than 1.0% yields for 10-year sovereign risk in its gilts.

Tapering the flow of liquidity provided by the major central banks may pressure sovereign yields to rise, increase corporate borrowing costs and eventually begin to expose those countries and companies with weaker balance sheets and limited growth prospects. The stark difference in US Treasury rates compared to the other "safe haven" sovereign debt has also contributed to a strong dollar that may soon begin to menace those that pay debt service in dollars while collecting revenues in local currency. International commodities keyed to the dollar will increase local costs – sugar, fuel, plastics, steel – such that the weakest of the herd may become exposed in advance of any major economic downturn.

Increasing risk premia for corporate debt may begin to signal this effect, e.g., the High Yield index has increased 19 basis points in 2018, to a 3.6% spread over comparable US Treasury notes, after contracting by 66 basis points in 2017 (see table below). These yield increases may reflect concern over the sustainability of the current economic expansion as well as fear of rising rates.

3. Eurozone Equities Weakness Expected

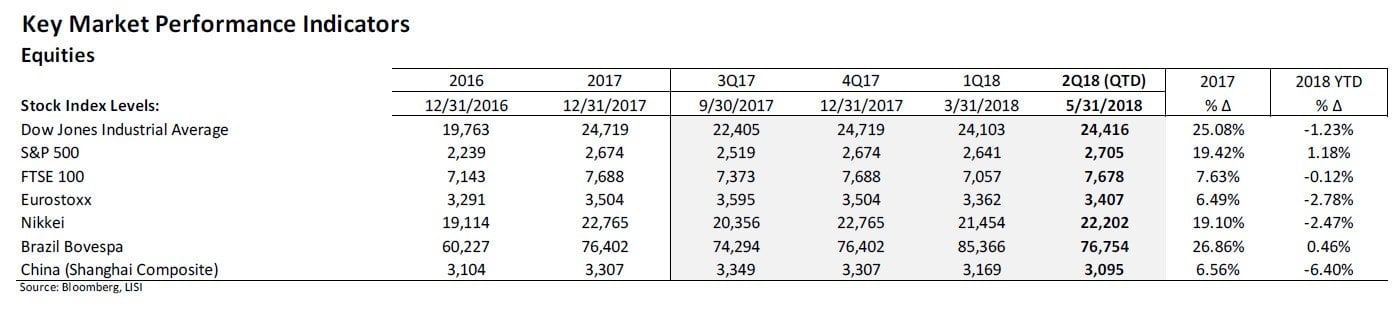

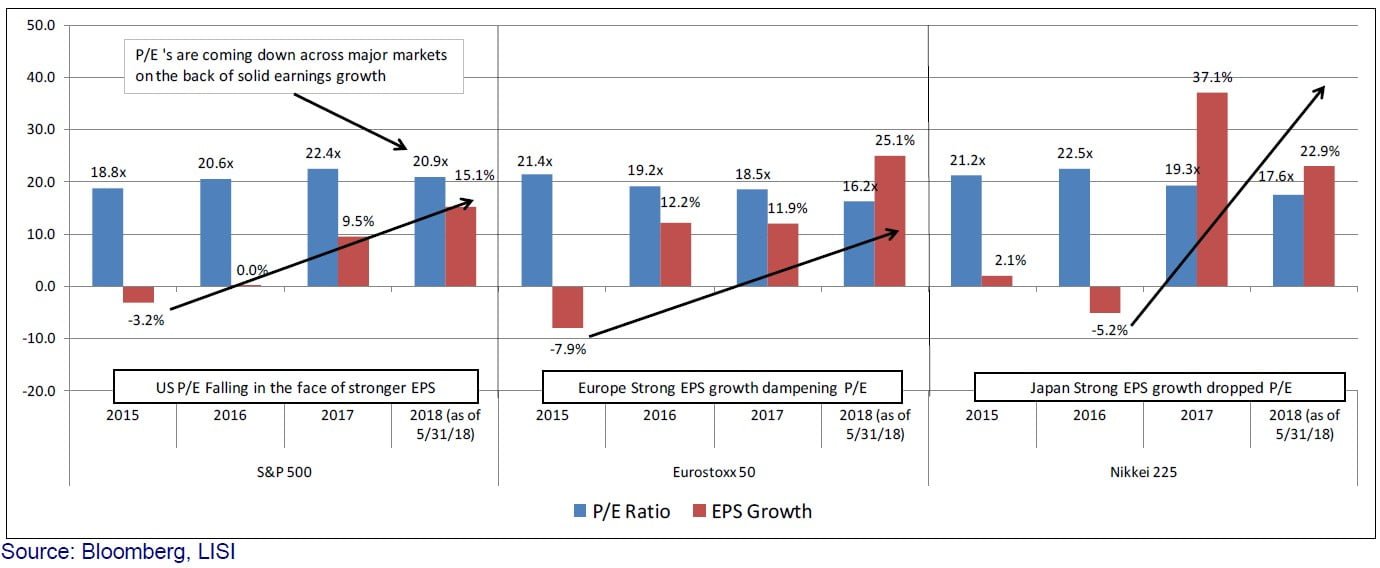

We remain optimistic about equities for the remainder of 2018, barring some major shock. The developed markets equity indices seem hesitant to return to their upward trend experienced from early 2016 to the beginning of 2018. The Eurostoxx 50 and Nikkei 225 both show negative performance for the year through May, while the US stock markets continue their leadership as the fiscal boosts of tax cuts and deregulation filter through to corporate bottom lines.

The somewhat more hawkish rhetoric of Fed Chairman Powell and the FOMC leads us to watch inflation data closely, since it might spark an acceleration in rate hikes which could dampen the enthusiasm for US equities. We are also watching the international economic environment for signs that the lattice of mutual support among the major markets may begin to weaken further.

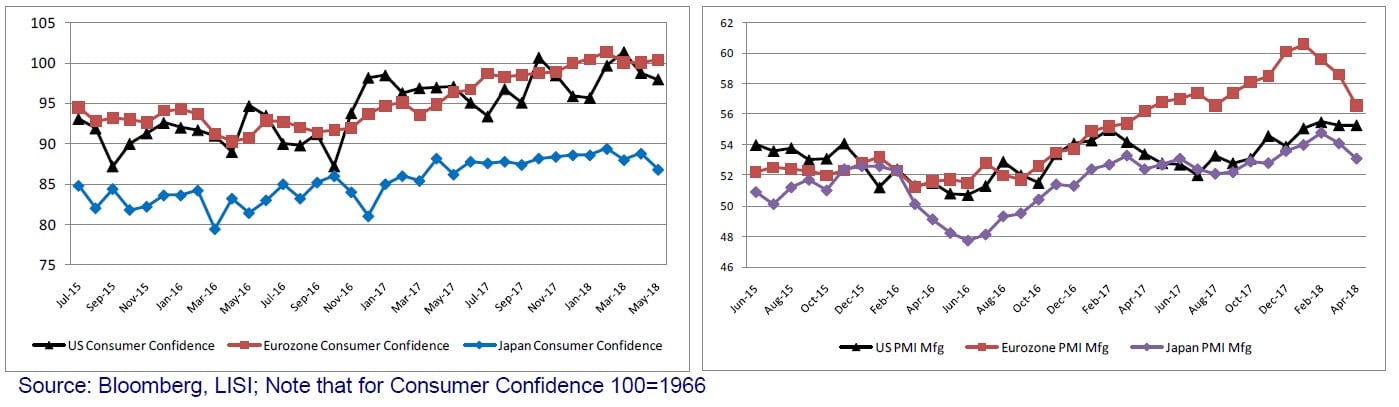

The market seems to be recovering from the Euro-jitters resulting from Italy and talk of actions that could jeopardize the country's finances and even potentially disrupt its participation in the Eurozone. That view notwithstanding, after an 18-month run-up during 2016 and 2017, European Purchasing Manager Indices (PMIs) are turning over, though they remain in positive territory. At the same time, consumer confidence is flat after running up through 2017 (see charts below). We view the weakness in Eurozone PMIs and confidence indices to suggest coming weakness and are reducing our European equity exposure accordingly.

Consumer Confidence and Purchasing Manager (PMI) Indices, 2015-18

Strong corporate earnings in early 2018 have tamed the high price-to-earnings (P/E) ratios that concerned us during 2017. With earnings-per-share growth accelerating, the P/E for the S&P 500 dropped from 22.3x at the end of 2017 to 20.9x as of May 22nd. Similarly, the Eurostoxx 50 showed a P/E of 16.2x vs. the end-year measure of 18.5x, while the Nikkei 225 registered 17.6x vs. 19.3x. We believe that the shift downward in valuations is healthy for the markets, and expect P/E contraction to continue in coming months (see chart below).

EPS Growth Across Regions Dropping P/E Ratios

Conclusion

At its late May meeting the LISI Investment Committee voted to maintain current Tactical Asset Allocations. We see continuing volatility in the markets, particularly in equities, but expect that broad-based economic strength will provide a sufficient foundation for markets to recover from small shocks such as the recent political rumblings emanating from a highly leveraged Italy. Heightened market sensitivity to QE tapering, inflation trade skirmishes, and geopolitical tension is likely to continue. Yet, we still see support for equity valuations in improving corporate earnings, particularly in a US market helped by tax cuts.

The market's resiliency of recent years, combined with solid economic underpinnings, gives us confidence that our overweight equities allocation remains justified. Accordingly, across asset classes we favor the following in terms of allocation:

- Fixed Income – We recommend shortening duration and accepting somewhat higher credit risk to mitigate effects of the anticipated rate hike cycle, while taking advantage of improving fundamentals

- Equities – We maintain our positive view on equities and maintain allocations given improving EPS, support from impending US fiscal stimulus, and the Fed's slow and steady approach to hiking interest rates and the balance sheet unwind. We are cautious about the prospects for European equities and have shifted our stance somewhat away and toward Asia, in addition to the core US positioning

- Alternatives – We like the low correlation to core markets exhibited by alternative assets, and favor their inclusion as a small component of portfolios with moderate to higher risk profiles

- Cash – We recommend keeping a small allocation in cash to capitalize on any market dislocations

Perhaps it is appropriate that a long, shallow economic recovery should follow the most jarring and profound economic downturn since the Great Depression. Over the last decade, central banks have had an unusual opportunity to experiment with varieties of stimulus in concert and with little fear of inflation. That period may now be approaching an end, with nascent removal of monetary accommodation through policy rate hikes and QE tapering. It remains to be seen whether the calipers of policy tools, the monetary authorities' toolbox analogue to the factory floor, can continue to run in just-in-time mode if damaging trade wars emerge or if other expansion threatening situations come into play.

{kind=link}