Warning signs are flashing in the U.S. market…

Since 2009, the U.S. stock market has made investors a lot of money. But sooner or later, the good times have to end.

Mean reversion, as we’ve talked about before, means that markets (along with pretty much anything else in life) tend over time to reverse extreme movements – and gravitate back to average.

It’s like a rubber band… stretch it and when you let go it returns to its original shape. So after a period of rising prices, securities tend to deliver average or poor returns. Likewise, market prices that decline too far, too fast, tend to rebound.

We’ve been saying for a while that the U.S. market is “stretched” and could snap back to its “original shape” at any moment.

And on top of that, by many measures, U.S. stock market valuations are high, the U.S. consumer could be in trouble and there’s plenty of uncertainty in geopolitics.

In short, the good times will eventually end for the U.S. stock market.

Now, I don’t recommend getting out of all of your U.S. positions. I think the bull market could still head a little higher. But I do think it’s time to reallocate a bit of your U.S. exposure. So where should you look to put some money today?

Invest in Europe

Europe has lagged the U.S. in the post-global financial crisis economic recovery process. It did not adopt the quick-fire emergency measures that U.S. policy makers did. (But then again, Europe’s banks were not 24 hours away from blowing up in an almighty financial explosion the way the U.S. banks were in 2008.)

Still, Europe made some policy mistakes. Although Europe slid into recession, European policymakers did not push the money printing buttons as quickly as the U.S. And the European Central Bank (ECB) didn’t start lowering interest rates until a full year after the Federal Reserve, the U.S. central bank, had started.

But it is clear now that the European economy is catching up with the U.S. recovery. It is probably about two years or so behind the U.S., but recently has been following a similar policy roadmap as that drawn by the U.S.

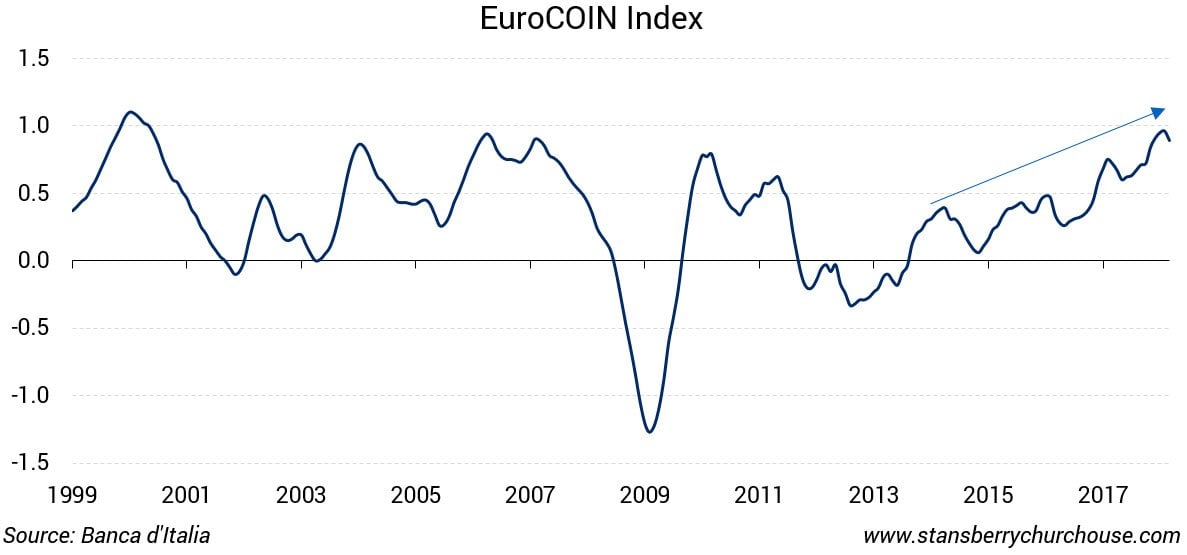

One can see the growth trend clearly in the EuroCOIN index, an economic activity index that takes in a large set of Eurozone growth data to produce a singular growth index. Think of it like a proxy index for Eurozone economic growth. It recently hit a ten-year high.

Unemployment in the Eurozone has also been falling steadily. It fell from its peak of more than 12 percent to around 8.7 percent in December 2017, and is looking set to fall further.

The Purchasing Managers Index (PMI) has long been regarded as an indicator of the health of an economy, particularly its manufacturing sector.

Europe’s PMI recently hit a 6.5-year high. The Eurozone services PMI also recently hit a record high.

Low inflation has been a cause for concern for policy makers around the world. It is often seen as a sign of weak end-user demand and signals weak growth. Inflation has been below the ECB’s target of 2 percent, but it will likely be running at about 1.7 percent to 2 percent in the next year or so. Higher inflation will be a sign of stronger growth and a signal for the potential further easing back of quantitative easing.

So the underlying macro conditions in Europe look to be in decent shape

Still, Europe’s stock market has significantly trailed the performance of the U.S. market. Given the elevated valuations in the U.S. market, I expect there will soon be a rotation out of U.S. equities and into markets like Europe.

Here are five reasons why you should invest in Europe…

- The European market was the worst performing major equity market globally in 2017.

It has underperformed the U.S., Japan and the emerging markets.

- Europe’s underperformance has been occurring as the Europe economic surprises index has been on a rising trend relative to the similar index for the world at large.

Simply put, the equity market has not been reflecting the solid and improving underlying macroeconomic conditions.

- European equities have not reacted to the recent decline in the euro versus the U.S. dollar.

Normally, a decline in the value of the euro should be positive for European exports and earnings. It would normally reflect in the outperformance of the equity markets. But not so far.

- European fund managers appear to be generally positive about the European equity markets.

They have been putting money to work in the markets. Cash holdings by long-only funds managers, recently at about 1.4 percent, are close to six-year lows.

Typically, when flows into European equities are rising relative to flows into the U.S. market, the European stock markets tend to outperform the U.S. market. This has not happened this time around – at least not yet!

- Europe has avoided the worst of the political outcomes that could have come about in various elections.

There have been plenty of surprises on the political front over the past year or so. But even Brexit negotiations seem to be proceeding without the total impasse that seemed possible in early 2017. There is still a long way to go on this front though.

In short, as investors see Europe’s generally positive economic news and its underperformance, they’ll likely rotate into European stocks in the coming year. I recommend you do the same and invest in Europe.

Good investing,

Peter Churchouse

Article by Stansberry Churchouse