I recently wrote an article for Sure Dividend entitled “Consider Equity REITs for Your Next Investment“. In that article, I listed nine equity REITs for dividend investors to consider in light of the drubbing that REIT valuations have recently taken due to fear of rising interest rates and to capitalize on the pass-through provision for REIT income included in the new tax legislation. Both of these topics are covered in some detail in the previous article. This article provides a more complete investment thesis for Omega Healthcare Investors (OHI), one of the nine REITs highlighted in the previous article.

[REITs]ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Omega Healthcare Investors

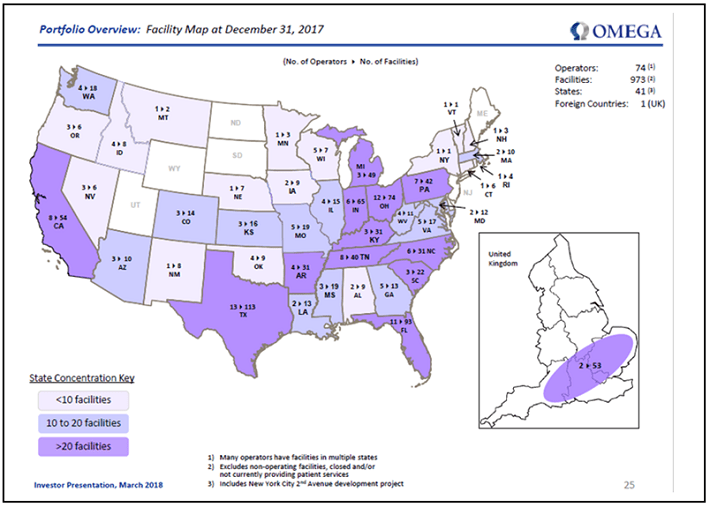

Omega invests primarily in skilled nursing facilities (SNFs) and is as close to a pure play SNF REIT as can be found in the market with 83% of revenues generated through ownership of SNF facilities and 17% generated by senior housing developments. The company’s enterprise value is $10.3B making it the largest SNF focused REIT in the market. Omega owns 973 facilities located in 41 states and the United Kingdom (UK) managed by 74 different operators.

Source: OHI Investor Website

The chart above shows OHI has reasonable geographic diversification with facilities across most of the US and a foothold in the UK. As noted above, OHI also has a diverse set of 74 operators for its facilities. The chart below provides details for the top 10 based on OHI revenue generation.

Source: OHI Investor Website

Readers will note that the top 10 operators of OHI’s facilities provide roughly 65% of OHI’s revenues.

Omega carries an investment grade credit rating of BBB- from Standard & Poor’s and Fitch. To maintain that investment grade credit, OHI carries a fairly conservative debt load with a total debt to EBITDA ratio of 5.1x and a fixed charge ratio of 4.1x ensuring that OHI generates more than sufficient earnings (EBITDA) to cover the interest on debt plus preferred dividend distributions. Omega also has sufficient liquidity with a $1.25B revolving credit facility with roughly $1B available as of February, 2018.

Omega Healthcare’s Recent Financial Performance

Omega’s past financial performance has been just short of exceptional, particularly for a stodgy conservative equity REIT. The chart below shows OHI’s investment and revenue growth from 2004 through 2017.

Source: OHI Investor Website

Both investments and revenue have grown at better than 19% annually for the last 14 years. That growth in investments and revenue has also translated into solid growth in EBITDA and Adjusted Funds From Operations (AFFO) over the same period.

Source: OHI Investor Website

Keep in mind the above numbers are not on a per share basis; they are at the business level. Readers should specifically note that, with an annual growth rate of 23.9%, OHI has been able to grow AFFO faster than both investments and revenue. Omega has shared its growth in AFFO with investors over those 14 years as shown in the chart below.

Source: OHI Investor Website

Omega’s dividend distributions have grown at an average annual rate of 10.4% from 2003 through 2017 (15 years) with an average AFFO payout ratio of just over 78%. Investors who have held on to OHI have been well rewarded through dividend investments alone. A 10.4% compound annual growth rate for dividends in excellent. Omega’s share price has likewise experienced significant growth over the last 15 years.

Source: OHI Investor Website

With a compound annual growth rate of 14.2%, OHI has rewarded long term investors with a high level of dividend and capital appreciation over the last decade and a half. It would seem from all the long term metrics that OHI has been and should continue to be a fantastic investment.

However, OHI’s near term performance has investors on edge. I’ll cover this in more detail in the investment thesis section below.

Omega Healthcare Investment Thesis

With the general market currently experiencing a mild correction, and REIT valuations suffering further from fear of rising interest rates, should you be considering an investment in OHI at this time? If that isn’t already a difficult question, there is more to take into consideration before deciding to take a long position in OHI. I’ll cover the considerations for and against OHI in more detail below.

Market corrections happen all the time and, generally, it is healthy for the market to shake off some of the froth and foam from periods of steep valuation increases. I generally use market corrections to accumulate more shares or initiate positions in new holdings. In other words, “buy the dips“.

Interest rates are another matter all together. I’ve looked at the correlation between equity REIT valuations and the 10 year Treasury in previous writings as have other authors. While there is correlation initially between rising rates and falling equity REIT valuations, it is generally limited to a couple of quarters time after which REIT valuations generally recover and return to business as usual. The way I process this information is that REIT’s valuations, like most other high yield income investments, initially fall because there is a direct competition between rising interest rates and REIT dividend yields. As rates rise, investors demand a commensurately higher yield which drives down REIT valuations. The recovery in REIT valuations happens because the underlying reason for rising rates, accelerating economic growth, benefits REITs in general just as it benefits other company’s financial performance. For more detail on the behavior of equity REITs during periods of rising interest rates, readers can link to Cohen & Steers.

One of the most significant long term reasons for investing in OHI is our changing population demographics. With the baby boom generation retiring at the rate of roughly 10,000 per day, the number of seniors in the population is growing rapidly. The chart below shows the growth in seniors for various age groups.

Over the next 30 years, the population of people typically needing skilled nursing care will grow significantly which should translate into higher demand for the facilities OHI owns. The next chart shows the utilization of SNF type facilities as a function of age.

Source: OHI Investor Website

Reader should note that the steep portion of the curve runs from about 75 – 88 years of age where the number of SNF days rises from about 1,300 to 5,300 per 1,000 beneficiaries. Skilled nursing facilities could actually be in short supply in a few years as the chart below shows.

Source: OHI Investor Website

By 2022, SNF occupancy is projected to be at roughly 95%. At this point, local and regional availability will become tight. By 2025, the expectation without additional SNF facilities being built, is that there will be an overall shortage of SNF space to meet demand.

One of the key reasons OHI’s near term performance has flattened and its stock price has suffered is that a couple of OHI’s operators are having difficulty covering the rent for OHI’s facilities. Specifically, Orianna, representing 5% of OHI’s revenue stream, filed for bankruptcy March of 2017 resulting in some revenue impairments and Genesis, representing 7% of OHI’s revenue stream, has been in the financial doghouse for the last couple of years. OHI’s response has been to transition some of the facilities operated by Orianna to other healthier operators, sell a few underperforming facilities, and to grant limited rent concessions to Genesis. This is why we see no growth for investments, revenue, EBITDA, and AFFO between 2016 and 2017 in the charts presented above. I believe that OHI will successfully work through the current issues with underperforming operators allowing OHI to continue to grow and prosper. The expected demand increase resulting from the aging of the baby boom generation will grow to be a major tail wind in just a few years.

However, there is more risk with an investment in OHI than was apparent 3-4 years ago when I initiated my position in the REIT. REIT’s rely heavily on equity capital secured through secondary offerings for growth and investments. With OHI’s near 10% dividend yield, that equity capital today is too expensive meaning that OHI may have to rely on debt for capital investments for the near future.

There is also the risk that the future may bring changes and reductions to Medicare and Medicaid reimbursements. In my view, this is a relatively low risk. The over 65 group is set to grow to roughly 25% of the total US population and generally has very high voter turnout. I don’t believe politicians will risk the angst from such a large active voter block that significant changes to either Medicare or Medicaid would surely bring. With that said, the risk is not zero.

Final Thoughts

Omega is a well established and well run healthcare REIT with a history of steady and strong growth. With an investment grade credit rating, a strategy in place to address operator performance, and return to strong growth, OHI management is making the right moves for the future. Recent investor jitters over rising interest rates and its operator issues have pushed OHI’s stock price into deep bargain territory and its dividend yield up to about 10%. The partnership and REIT pass-through income provision in the recently passed tax legislation will shield 20% of OHI’s dividend from Federal income taxes. An investment in OHI at its current valuation should reward investors very well in future years with the demographic tail wind pushing profits higher.

There is risk in an investment in OHI with its currently underperforming operators and high concentration in SNFs. I already have a large position in OHI and I’ve chosen not to accumulate additional shares until it is clear that OHI management is able to effectively manage its underperforming operator issues. If I had to give OHI a rating today, based on my risk tolerance level (conservative), I’d give it a Hold while awaiting progress on the operator transitions. With that said, OHI does currently rank as a buy in the March 2018 Sure Retirement Newsletter.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by Dirk S. Leach, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.