We are short shares of Proteostasis Therapeutics, a clinical-stage biopharmaceutical company whose lead drug, PTI-428, aims to treat the genetic disorder cystic fibrosis. Proteostasis claims that the drug works in a unique way, by somehow increasing the levels of messenger RNA and protein corresponding to the so-called CFTR gene that is dysfunctionally mutated in people with the disease and that gives rise to its ultimately fatal symptoms.

In December, Proteostasis released results from a small Phase 2 proof-of-concept clinical trial, supposedly showing that PTI-428 meaningfully improved lung function relative to placebo. On the back of these results, the company announced last week that the FDA had granted it “breakthrough therapy” designation, a relatively minor development that nonetheless sparked a ~100% spike in the company’s stock price. Over the following five trading days, Proteostasis’s entire share count turned over more than twice, strongly suggesting an influx of new and potentially uninformed investors. The company quickly capitalized on this surge by announcing a nine-million share public offering last night – apparently as eager to sell shares at recent prices as we are.

Contrary to Proteostasis’s hype, we believe that its Phase 2 results are far less meaningful than they appear. The main reason that PTI-428 looks good is not that patients who received it performed unusually well but that the four placebo patients to whom they were compared performed unusually poorly. Judged by a more reasonable benchmark, PTI-428 seems to do little – echoing an earlier, more obviously disappointing Phase 1 trial in which the drug yielded no statistically significant improvement in lung function.

While Proteostasis touts changes in CFTR mRNA and protein levels as key signals that PTI-428 is working as intended, closer inspection reveals a wide range of data-quality problems and red flags, such as the absence of consistent dose-response relationships. Given the scarcity of CFTR mRNA and protein even in the airway epithelium, we doubt that Proteostasis can reliably measure its favored biomarkers, calling into question its fundamental understanding of its own drug. Indeed, we find it difficult to trust the company’s data, given its tendency to gloss over potentially negative facts. For instance, while a group of partially independent researchers have recently found that, in one in vitro model, PTI-428 failed to increase CFTR protein levels or functionality to a statistically significant degree, either on its own or when added to standard-of- care drugs, Proteostasis management has ignored the unpleasant results, even though three Proteostasis employees were co-authors on the paper.

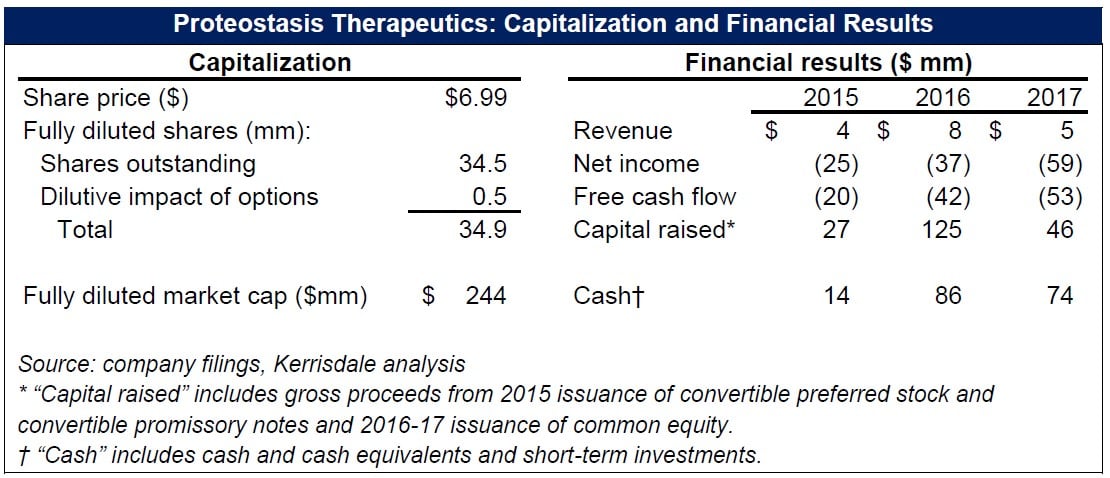

With an ineffective lead drug and unpromising pipeline, Proteostasis has little value; we estimate 70-90% downside, based on cash per share. There is little value in PTI’s misleadingly spun data, bizarrely noisy biomarkers, and selectively disclosed results. Alas, it’s far easier to inflate weak data than it is to inflate ailing lungs.

I. Investment Highlights

Clinical data show that Proteostasis’s lead drug is ineffective. The apparent success of PTI-428 in its small Phase 2 proof-of-concept trial stems almost entirely from the anomalously bad performance of the 4-person placebo group, while, on average, patients taking PTI-428 barely improved. With larger, more representative placebo groups in future trials, we believe the

illusion of PTI-428’s efficacy will disappear; after all, the drug already failed to deliver statistically significant efficacy results in an earlier trial. Beyond measures of lung function, PTI-428, unlike effective cystic-fibrosis drugs, has failed to meaningfully improve sweat-chloride concentrations. Meanwhile, other clinical measures that Proteostasis at one point planned to study, like patient- reported health satisfaction, have mysteriously vanished from the discussion, perhaps because the company didn’t like the results it got.

Proteostasis claims that its drug works by increasing levels of CFTR mRNA and protein, but its attempts to directly measure changes in these scarce substances have yielded extremely noisy and unreliable data, replete with inverted or nonsensical dose-response relationships (i.e., low- dose or even placebo patients experiencing greater “improvements” in these metrics than high- dose patients). The company has also alluded to problems with biomarker quality control and the need to discard “outlier” values for unexplained reasons, raising serious questions about just how much investors should trust any of its results.

The case of the missing trial and other data mysteries. We believe Proteostasis has a habit of sweeping unpleasant or confusing findings under the rug. Suspiciously, a 14-day, 16-patient trial of PTI-428 combined with another cystic-fibrosis drug, originally projected to read out in 3Q 2017, was quietly shifted to 1Q 2018, only to disappear from the company’s recent investor presentations and earnings releases as the first quarter draws to a close. What happened to this trial, and why hasn’t the company already explained it?

Similarly, Proteostasis has failed to reckon with the unsettlingly weak results of a recent in vitro study of PTI-428 conducted by a semi-independent team of researchers. These researchers found that, in a cell-culture model of cystic fibrosis, PTI-428 only increased CFTR mRNA to a “modest degree” and did not appear to increase CFTR protein; even when combined with standard-of-care drugs, PTI-428 did not confer a statistically significant improvement in CFTR protein quantity or channel function. These null results fly in the face of Proteostasis’s claims about how its drug ought to work but support our view that, whatever it might do in the company’s labs, the drug does little of value in the real world.

II. Company Overview

Founded in 2006, Proteostasis began as a broad effort to develop drugs to combat dysfunctional protein processing and regulation. After years of largely fruitless effort, in 2013 the company made what it now regards as a “breakthrough discovery”: a novel type of treatment for cystic fibrosis.1

Cystic fibrosis is a genetic disease in which people harboring certain mutations of a single gene produce misfolded or otherwise defective forms of a protein known as CFTR, a chloride channel that, among other things, allows the mucus in the airway to remain properly hydrated. Defective CFTR molecules give rise to thick mucus that fosters the growth of pathogens, triggers chronic inflammation, and severely damages the lungs, ultimately leading to death. A rare disease (with only 70,000 victims worldwide), cystic fibrosis defied attempts at addressing its root cause until the advent of Vertex Pharmaceuticals’ drug ivacaftor, a small molecule that enables some forms of mutant CFTR to work better once they’re embedded in the cell membrane. Unfortunately, patients with the most common form of cystic fibrosis, caused by having two copies of the F508del allele,2 don’t have much membrane-bound CFTR to work with, because the misfolded F508del protein is recognized as faulty by quality-control machinery in the cell and quickly destroyed before it can make its way to the membrane. Thus ivacaftor, on its own, only benefits a very small minority of cystic-fibrosis patients.

However, Vertex went on to develop a second drug, lumacaftor, that helps the F508del-CFTR protein escape destruction and reach the membrane, where ivacaftor can then enhance its (still impaired) ability to act as a chloride channel. This combination of lumacaftor and ivacaftor, marketed under the name Orkambi, is now the standard of care in cystic fibrosis, although some complain about its high cost and modest efficacy (1).

While several companies, including Vertex itself, are hard at work developing new and improved versions of drugs like ivacaftor (known as potentiators), drugs like lumacaftor (known as correctors), and complex combinations thereof, Proteostasis claims to have created something entirely different: an amplifier. In the company’s own words, “[a]mplifiers, which include [its lead drug] PTI-428, are CFTR modulators that selectively increase the amount of newly synthesized unfolded form of CFTR protein, thereby providing additional substrate for other CFTR modulators, such as correctors and potentiators, to act upon.”3 Based initially on its own in vitro studies, Proteostasis says that its amplifier drug causes CFTR mRNA and protein to proliferate, supplying enough fuel that, when added to, say, Orkambi, it might fully return patients’ lung function to normal.

That’s the theory, at least – and it was enough to get Proteostasis’s IPO done in February 2016, albeit at a share price 38% lower than initially projected. After a series of clinical-trial delays and disappointing data points, though, Proteostasis lost much of its market value by late 2017, as its share price dipped below $2 (75% less than the IPO level). In December, however, seemingly positive results from a Phase 2 proof-of-concept trial temporarily revitalized the stock, taking it back up to a price of ~$6 – but only briefly, as disappointment appeared to gradually creep back in, driving the price once more toward $2. Last week, however, Proteostasis enjoyed an experience of déjà vu, as its announcement that it won the FDA’s “breakthrough therapy” designation, itself the result of the same Phase 2 data from December, led to another price spike. The market is evidently regaining its faith in Proteostasis’s approach. But a close look at what the company has actually reported – as opposed to the stories it has told – reveals that its entire “amplifier” concept – the linchpin of its valuation – is likely bogus.

III. Clinical Data Show that Proteostasis’s Lead Drug Is Ineffective

Standard Endpoints

When Proteostasis disclosed results from its Phase 2 study of the “amplifier” PTI-428, the focus was on a standard measure of lung function: percentage of predicted FEV1, or ppFEV1. “FEV1” refers to forced expiratory volume over the course of one second, i.e. the quantity of air one can exhale during a forced breath lasting that long. Using standard benchmarks, doctors can establish predicted FEV1 based on factors like age and height. Dividing a patient’s actual measured FEV1 by his or her predicted FEV1 yields the standardized metric ppFEV1, which eases comparison across patients. Since cystic-fibrosis patients suffer from progressive lung deterioration that impairs their ability to exhale relative to healthy people, their ppFEV1 values fall well below 100%, typically in the range of 40-70%. Recent high-profile cystic-fibrosis clinical trials have largely aimed to demonstrate improvements in ppFEV1, which can themselves be quantified in two ways: absolute changes expressed in percentage points or relative changes expressed in percentages. For example, a patient whose ppFEV1 goes from 65% to 70% has improved by 5 percentage points in absolute terms and ~7.7% (= 70/65 − 1) in relative terms.

With this terminology in mind, we turn to Proteostasis’s results. In a 28-day trial enrolling cystic- fibrosis patients already taking Orkambi (and staying on it), Proteostasis compared 20 patients who added the “amplifier” PTI-428 to their regimen with 4 – yes, 4 – patients who added placebo. Proteostasis summarized the main efficacy endpoint as follows:

The addition of PTI-428 to Orkambi® demonstrated mean absolute improvements in ppFEV1 of 5.2 percentage points from baseline compared to placebo (p<0.05), with mean relative improvements of 9.2 percent (p<0.05). This treatment effect was achieved by day 14 and sustained through 28 days of dosing.

Though a 5-percentage-point change may not sound like much, it would constitute a meaningful improvement, especially on top of a drug like Orkambi that is already known to work; moreover, Proteostasis claims it was statistically significant at the 5% level. Notwithstanding the usual caveats about small sample sizes, Proteostasis thus treated this 5-point improvement as a decisive vindication of PTI-428, and the market has followed along.

But, to our knowledge, Proteostasis has only directly stated the observed improvement of PTI- 428 patients relative to placebo patients; it has not separately stated how well each group did on its own. However, individual patient data that the company has only disclosed in graphical form enables us to do the math ourselves, uncovering a much less inspiring picture. Below we reproduce Proteostasis’s graph of relative changes in ppFEV1, followed by our estimates of the underlying numbers. On average, we calculate that the PTI-428 group improved by just 2.5%, while the (4-person) placebo group worsened by 6.7% – exactly replicating Proteostasis’s stated placebo-adjusted relative improvement of 9.2%. In terms of absolute changes, we estimate that the PTI-428 group improved on average by just 1 percentage point, while the placebo group worsened by 4 percentage points. While this reconciles to the same net 5-point improvement reported by the company, the breakdown puts the data in a different light. The PTI-428 group didn’t see its ppFEV1 values noticeably increase; an average 1-point move across 20 patients is negligible. Instead, the unlucky 4-person placebo group saw its average tank, driven by just 2 individuals. The results that the market has celebrated don’t show a highly effective drug; they show an anomalously bad placebo. But this fluke is unlikely to repeat in future, larger trials, suggesting that the illusion of PTI-428’s efficacy will eventually vanish.

Article by Kerrisdale Capital

See the full PDF below.