The Clorox Co (NYSE:CLX) manufactures and markets consumer and professional products worldwide. It operates through four segments: Health and Wellness, Household, Lifestyle, and International.

Q1 2021 hedge fund letters, conferences and more

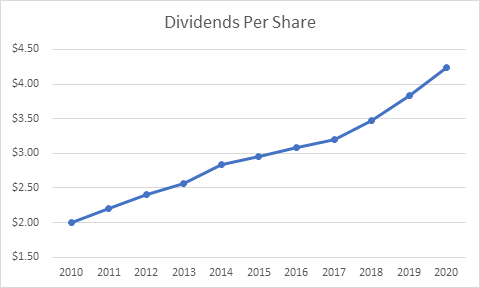

Clorox's Annual Dividend Increases

Clorox is a dividend aristocrat with a 44-year history of annual dividend increases. Over the past decade, Clorox has managed to increase dividends at an annualized rate of 7.50%.

The last dividend increase was in June 2021, when the Board of Directors authorized a 4.50% hike in the quarterly dividend to $1.16/share.

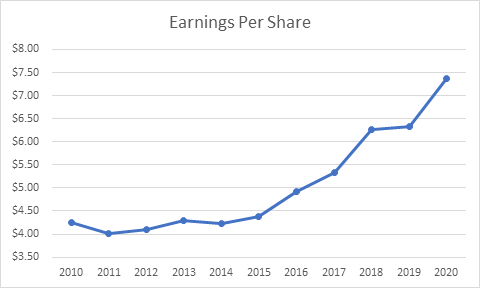

The company managed to grow earnings from $4.24/share in 2010 to $7.36/share in 2020. Clorox is expected to earn $8.38/share in 2021 and $8.13/share in 2022. The Covid-19 pandemic increased demand for Clorox products in the near term. While it is possible that growth in the near term would decelerate because people are not stocking up, it is also possible that we are in a new normal that would permanently increase the demand for its products.

It is fascinating how earnings per share basically remained flat between 2010 and 2015, which tested the patience of most long-term shareholders.

Clorox has a portfolio of products with strong brand names, that are number one or two in their respective product lines, which helps in having pricing power. As a result, it should be able to pass on commodity price increases to customers. Future earnings growth could be driven by innovation, new product launches, cost containment initiatives, as well as international expansion.

Delivering Returns

Clorox aims to continue delivering total stockholder returns by focusing on company's long-term financial goals such as:

- Growing net sales 2-4 percent annually

- Expanding earnings before interest and income taxes (EBIT) margin 25-50 basis points annually

- Generating free cash flow of 11- 13 percent of sales annually

The three pillars of the strategy include expansion in a geographic, category and channel direction, continued reinvestment in its brands as well as cost containment initiatives. A key driver of the strategy is to accelerate sales by growing existing brands, including expanding into adjacent categories, entering new sales channels and increasing penetration within existing countries. Increased exposure to emerging market economies could further drive increase in sales. The company also anticipates using its strong cash flow to pursue growth opportunities and increase shareholder returns. In addition to that the company will be targeting sales growth through product innovation, which helps its pricing power.

Clorox will also target margin expansion and maximizing cash flow through implementation a continued robust cost-saving program and maintaining price increases the company has taken. The strong focus on cost, has provided the company with a relative cost advantage versus competition. In addition, Clorox continuously reinvests money in its brands, which helps it maintain its market position.

One of the risks behind Clorox is that it generates a large portion of revenues from the US – over 80%. It is more exposed to the US economy than other global consumer staples companies, which could also be an opportunity as well. The other risk I see is that Wal-Mart (WMT) accounts for a quarter of sales for Clorox. Wal-Mart is notorious for trying to keep costs low, by squeezing vendors to sell at lower prices. This is bad for pricing power, and could impact profitability. This over reliance on Wal-Mart could be mitigated through continued international expansion. The other risk include competition from generic products, which could be mitigated by the ability to distinguish Clorox' brands by spending on R&D and advertising.

IGNITE Strategy

In 2019, the Company unveiled its “IGNITE” strategy, which works on top of its concluded 2020 strategy. Source: Clorox PR

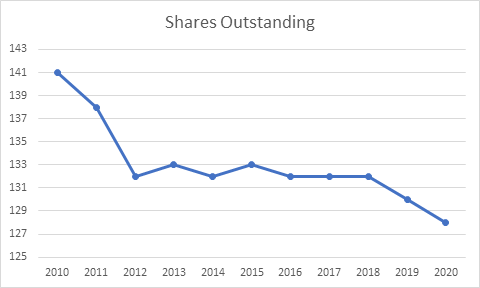

Growth in earnings per share was aided by a gradual decrease in the number of shares outstanding. Clorox has reduced its share count from 141 million in 2010 to 128 million by 2020.

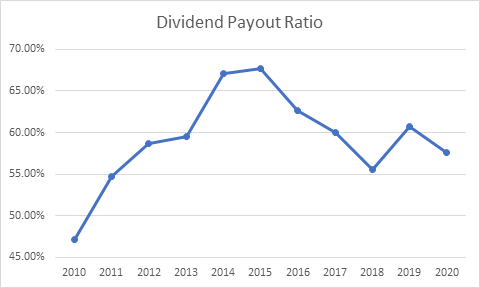

The dividend payout ratio increased from 47% in 2010 to 67.73% in 2015, before falling down to 58% in 2020.

Currently the stock is slightly overvalued at 23.23 times forward earnings. Clorox yields 2.59%.

Relevant Articles:

- Dividend Aristocrats List for 2021

- Dividend Aristocrats for Further Research

- Five Dividend Growth Stocks Raising Shareholder Distributions

- How long will it take to generate $1,000 in monthly dividend income?

Article by Dividend Growth Investor