For many investors, it’s pretty unsettling to hear that the market’s “fear gauge” is suddenly on a tear. But that’s what happened over the past week. That fear gauge, formally known as the VIX[i], rose almost 300% in three trading days, signaling an end to the market calm that dominated in 2017. It also triggered a chain reaction that caused problems for investors who’d been betting against volatility.

A lot of the coverage about what happened uses terms like futures curves, ETPs and “short vol”—it can get complicated. Let’s break down the components piece by piece.

What are VIX futures all about?

The VIX is an index that measures how much equity volatility the market expects in the near term. A higher index level means a higher level of expected volatility, and vice versa. Investors commonly use VIX futures[ii] to hedge or to speculate about how the level of volatility might change down the road.

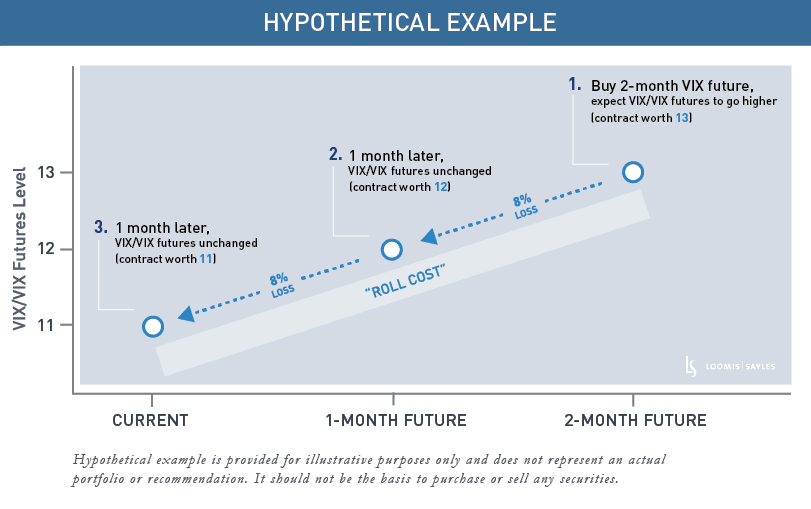

In 2017, the average closing level of the VIX Index was 11.10, among the lowest levels ever recorded. Despite this low level, the VIX futures curve was still relatively steep, so two-month futures were at higher levels than one-month futures, which were higher than the current level of the VIX. This “steepness” meant buying VIX futures to hedge or to speculate that volatility would go higher was a costly proposition. Let’s use an example to explain why.

Hypothetically, let’s say the VIX is trading at 11, one-month futures are trading at 12, and two-month futures are trading at 13. As an investor, I buy the two-month future at 13 to express a belief that expected volatility will rise. Then one month goes by, but the level of the VIX and VIX futures hasn’t changed. The two-month future that I bought at 13 now has one month to expiration and is now only worth 12. This equates to a loss of 8%! If I continue to hold this another month, and the level of the VIX and VIX futures still don’t change, my 12 would go to 11 (where the VIX is currently trading) and I would lose an additional 8%. This is what investors call the “roll cost” associated with being long volatility.

What is an ETP?

The VIX futures market is largely an institutional market, but in 2010, exchange-traded products (ETPs) were created to make volatility trading more accessible to retail investors. Some ETPs allow an investor to express a long view on volatility in the S&P 500® Index; they will gain value if volatility rises, but are subject to the “roll costs” as described above if volatility doesn’t change and will lose value if volatility falls. In 2011, a new kind of ETP emerged that allowed investors to express a short view on volatility (called inverse ETPs). Inverse ETPs lose value if expected volatility rises and gain value if expected volatility falls. Importantly, investors in inverse ETPs will also receive the “roll cost,” so in the hypothetical example above, they would make 8% per month if expected volatility didn’t change.[iii]

The “short vol” trade

Inverse ETPs are effectively a bet against volatility, and this is what the “short vol” trade was all about. Prior to the dip in the market that started on January 29, the S&P 500 had not had a 5% correction in 400 trading days—this was the longest run without a 5% correction in 50 years! Given that backdrop, it is not surprising that the VIX was also historically low in 2017. In this type of environment, inverse ETPs were steadily rewarded because volatility rarely became elevated. Investors flocked into this type of strategy, as yield was scarce in other asset classes, and the risk/return tradeoff—in 2017’s low-volatility environment—seemed very favorable.

Read the full article by Scott Darci of Loomis, Sayles & Co., Advisor Perspective