During his first State of the Union address on January 30, President Donald Trump touched on a number of policy milestones and laid out his plan for the continued prosperity of the United States. Here, our experts offer their perspective on how the details of that speech (namely, the dollar’s strength, infrastructure spending, and defense) could potentially impact the financial world.

Read on to see what they think.

Earnings

John Butters, VP, Senior Earnings Analyst

“And just as I promised the American people from this podium 11 months ago, we enacted the biggest tax cuts and reforms in American history…We slashed the business tax rate from 35 percent all the way down to 21 percent, so American companies can compete and win against anyone in the world.” –President Trump (January 30).

In the State of the Union address on Tuesday, President Trump touted the passage of tax reform, which he signed into law on December 22, 2017. Prior to the bill becoming law, a number of S&P 500 companies had made positive comments about the potential benefits of tax reform.

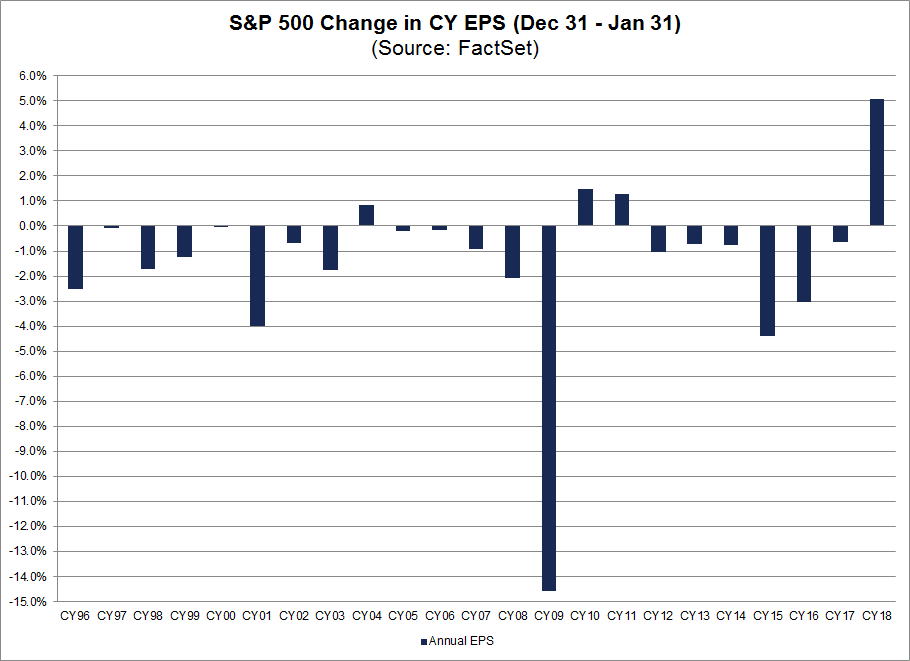

Since the start of 2018, the CY 2018 bottom-up EPS estimate for the S&P 500 (which is an aggregation of the median 2018 EPS estimates for all of the companies in the index and can be used as a proxy for earnings) has increased by 5.1%. This represents the largest increase in the annual EPS estimate over the first month of the year since FactSet began tracking this data in 1996. The reduction of the corporate tax rate in 2018 due to the tax reform law is a major contributor to this increase in earnings expectations for 2018.

In addition to the comments on tax reform, President Trump also made comments regarding infrastructure spending in Tuesday's speech.

“I am asking both parties to come together to give us the safe, fast, reliable, and modern infrastructure our economy needs and our people deserve. Tonight, I am calling on the Congress to produce a bill that generates at least $1.5 trillion for the new infrastructure investment we need.”

Would an infrastructure bill also provide a boost to earnings expectations for S&P 500 companies? From December 31 through January 31, 88 S&P 500 companies discussed the term “infrastructure” during their earnings calls for the fourth quarter. However, only a small number of these companies discussed this term in reference to a potential federal spending plan. Based on the comments from these companies, it appears any positive impact from a federal infrastructure plan would likely occur after 2018.

Fixed Income

Pat Reilly, VP, Fixed Income Analytics, EMEA

As you are stuck in rush hour traffic on a crumbling interstate or stranded at a terminal that feels so, so far removed from the golden age of flight (LAX, O’Hare, LaGuardia – I’m looking at you), the President’s desire for Congress to generate some sort of infrastructure bill undoubtedly rings clear. What remains hidden like an iceberg’s true mass though, is the impact of said infrastructure bill on interest rates and dollar strength. The President is known for taking credit for the performance of the economy (although our now pre-teen expansion is more certainly attributed to Ben, Janet, and Tim Geithner than the Oval or either legislative body), but if we continue down this road the implications could veer towards a correction or recession. Let me elaborate.

Nominal GDP growth is trending around 3% on an annualized basis and inflation is still nascent. At the same time, interest rates are slowly heading higher and balance sheets are normalizing. The impacts of Tax Cuts and Jobs Act are yet to be felt though, either positive (more $ in your pocket!) or negative ($1.5 trillion added to the Federal debt that, ostensibly someone will pay eventually). So who pays for an additional $1.5 trillion infrastructure bill? My sense is that getting 6x more funding from non-Federal sources than Federal funding is a pipe dream. I mean, I want to pilot a F-35, but that’s not going to happen either! So eventually, We The People will end up financing this somehow, likely at higher rates to compensate for a more leveraged economy. At the same time, the administration continues to talk down the dollar (sitting here in London, recent dollar weakness makes zero sense to me relatively speaking). This is great for exports, but harms the consumer, invites further inflation into the core basket of goods, and makes it harder to inflate away the implications of added Federal debt. This, as you may have surmised, also indicates higher rates ahead.

This implies that fiscal and monetary policy are not on the same page (not that they should be) and that the Fed must be ever diligent not just on the dual mandate of full employment and price stability, but also on a shadow third leg in evening out the government’s predilections.

My 2018 policy prediction: the Fed reverts course from three or four rate increases to two, as a lagging dollar and market pressures do some of the heavy lifting around rates for them.

Global Economies

Sara Potter, VP, Associate Director, Thought Leadership and Insights

In his State of the Union address, President Trump cited strong job growth since the election. In December 2017, 148,000 jobs were added, marking 87 straight months of positive job gains. But throughout 2017, the job growth numbers continued to ease, not surprising for an expansion that is now 8.5 years old and with an unemployment rate at a 17-year low of 4.1%. While still respectable, the 12-month increase in nonfarm payrolls that we saw in 2017 was the slowest in seven years, with 2.1 million jobs added.

The president also talked about renegotiating trade deals. Although he didn’t mention NAFTA specifically, this trade deal is currently being renegotiated. With Mexico and Canada making up nearly 30% of U.S. total trade, the stakes are high and the outcome will certainly have an impact on future trade negotiations.

Jessica Ulbricht, Consulting Manager, New York GBB Consulting

Preceding President Trump’s 2017 inauguration, an anticipated increase in defense spending and military friendly policies resulted in gains for combat and defense stocks . The President reiterated his focus on defense spending in Tuesday’s State of the Union address, and cited ongoing national security threats in his call on Congress to fully fund the U.S. military by ending the defense budget sequester.

The perception of a favorable military and defense environment has continued to augment these stock gains throughout the first year of the Trump presidency. Over the last year, an index of the top U.S. defense stocks has maintained its outperformance of the S&P 500, with gains amongst defense contractors and defense electronics companies being the most pronounced.

Despite these calls for increased spending, it is probable that Congress will continue to kick the can down the road with respect to substantially increasing defense appropriations. While some Democrat and Republican leaders have publicly recognized that increased funding is necessary to support efforts of bolstering military readiness, disagreements on unrelated issues stand to prevent this proposal from receiving the necessary 60 Senate votes to pass. Both sides of the aisle need to compromise on some of the outstanding domestic policy issues, or bipartisan support for a large increase to the defense budget will remain unlikely.

As reactions to the President’s address appear to remain split down party lines, partisan business as usual can be expected to continue as we approach this year’s midterm elections. As such, it is unlikely that defense stocks will continue to outperform at their current rate, but modest gains are still a reasonable expectation given the widespread recognition of the need for an eventual defense spending increase.

Mergers and Acquisitions

Bryan Adams, Director, FactSet M&A

Tuesday night's State of the Union address was surprisingly refreshing in that it referenced mergers and acquisitions at several key moments. Just kidding, these speeches rarely have a direct impact on M&A and as far as I know, no President has ever mentioned M&A in the State of the Union. There may be themes that hint at potential policy but until concrete legislation sits firmly on the horizon, M&A remains neutral from these political events.

However, for the sake of discussion, I heard a few key topics that have an outside chance at influencing M&A, where I can definitely foresee a time when we could approach the prospect of that being an eventuality.

Tax Reform: We recently examined where this stands with M&A, but to paraphrase here: not a deal-driver. There is a possibility that the few industries not benefiting as much from tax reform could consolidate, but the relative impact has to be meaningful before any deals emerge.

Deregulation: Within the core themes of 2017 was the expansion of a deregulatory environment. For example, opening up more federal land, allowing coastal drilling, and removing hurdles for coal are supposed to hasten energy independence (which was discussed in the speech). Other industries are in focus as well. As such deregulation is generally viewed as a net-positive for business. From an M&A perspective, major deregulation historically has led to significant deals in the aftermath. Glass-Steagall repeal in 1999 led to financial services consolidation so that US banks could better compete with global banks in Europe and Asia. Telecommunications Act in 1996 led to consolidation in the media and telecommunications sectors (and the re-joining of the former Baby Bells). Will the current deregulatory march have the same impact on any industries? At the moment, I'd also say there aren't any deal-drivers in sight.

In short, speeches are great for promoting and selling ideas, and an assessment of the past year with a view to the next year is an age-old tradition. But real policy needs to be in place before we see any real M&A.

Article by FactSet