Emerging-market bonds delivered strong returns last year, and we think the sector has more potential in 2018. But global economic and geopolitical risks abound, making it more important than ever for investors to be selective.

[REITs]Emerging-market debt (EMD) got off to a rocky start in 2017 for fear that rising US interest rates and a stronger dollar would draw money out of the sector and put pressure on emerging-market (EM) government and corporate balance sheets. But investors who stayed the course did well. Through November, major indices for EM government and corporate bonds—both US-dollar and local-currency denominated—returned anywhere from 7.5% to nearly 13%.

Why has the EMD sector been so resilient? Part of the answer has to do with the health of the global economy. After nearly a decade of subpar growth, developed-market countries are finally starting to gain traction. This is good news for the developing world, because stronger growth in the US and other advanced economies tends to boost economic activity elsewhere.

In 2018, though, investors will have to exercise caution. EM fundamentals remain strong and EMD valuations broadly attractive. But macroeconomic and geopolitical risks are growing, and the global environment has become less certain. The Federal Reserve could disrupt markets by tightening US monetary policy more aggressively than expected. China’s economy could slow further, putting pressure on commodity prices.

This is why it’s essential to stay active and take a highly selective and tactical approach in order to build portfolios that can deliver long-term results.

Why It Pays to Be Choosy

The good news is that critical reforms and stronger economic fundamentals have reduced many developing countries’ vulnerability to external shocks and sudden portfolio outflows. They’ve done this by bringing inflation under control, reducing current account deficits and embracing centrist, fiscally responsible economic policies. All of this should provide EMD with a cushion that it did not have just a few years ago.

Even so, investors should be selective when it comes to their EM exposure. Country and sector selection matter, because political and economic risk varies across the developing world.

The biggest challenge in 2018 will likely be monetary policy changes in the US and other DM countries. So far EMD has weathered a series of gradual Fed rate hikes without difficulty. But with new leadership at the Fed, there’s a chance the pace of tightening could increase in 2018 by more than the market currently expects. If it does, US Treasury yields could rise and a recent uptick in the US dollar could accelerate, putting pressure on some EM currencies and bonds.

Political risk within EM countries shouldn’t be overlooked, either. Several countries, including Mexico and Brazil, will hold elections that could lead to significant policy and leadership changes.

Fortunately, political risk tends to be country specific. Argentina’s politics have little to do with Indonesia’s. This means investors can limit the volatility that any single country’s political risks might generate by diversifying across EM countries.

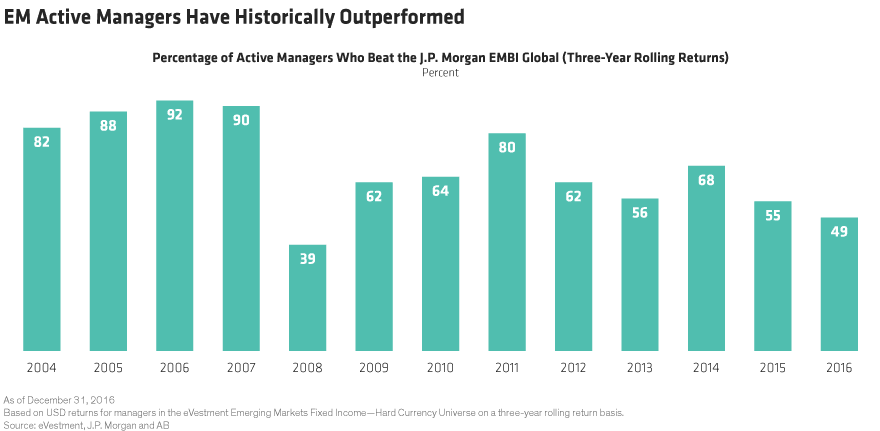

Over time, active EM strategies that take country- and company-specific factors into account and can underweight and overweight sectors and individual bonds have paid off. Between 2004 and 2016, a majority of hard-currency EMD active managers beat a broad index on a three-year rolling basis 85% of the time (Display).

A Multi-Sector Opportunity Set

How investors build an EMD allocation will depend on each one’s needs, comfort level, return objective and governance constraints. But having access to EMD’s multi-sector opportunity set offers the ability to diversify by country, credit and currency, and can help to generate stable returns over a multiyear investment horizon.

Investors must be selective about their EMD exposure, particularly in times of uncertainty. But in today’s world, it no longer makes sense for investors to relegate EM bonds to the periphery of their fixed-income portfolios. In a sense, many developing countries have already emerged and are essential engines of global growth. In our view, a fixed-income portfolio today would be incomplete without them.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Article by Shamaila Khan, Alliance Bernstein