An Undercurrent of risk awareness means it is a time for buying gold or is the metal outdated?

After the GFC, investors the world over remain palpably aware of the potential consequences of another unexpected burst of a credit bubble. One of the conundrums facing risk managers is preparing a contingency for this scenario, when the inevitable all-out rapid-fire asset liquidation would be triggered. What reassurances can managers offer investors as potential hedges against a downturn that may very well materialise as a result of failings in central bank planning?

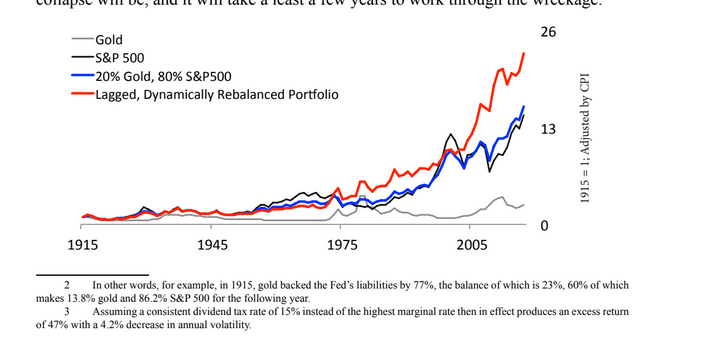

Balancing the Trade Off

To certain market participants the go-to solution is gold – historically proven to hold ground, and often gain, in these types of market crashes. However, the historical performance of growth in gold returns is far from appealing compared to many alternatives – leaving many portfolio allocations far under a prudent optimal allocation for minimising risk exposure. Considering that since 1914, annually rebalancing a portfolio with a 20% gold allocation and the remaining 80% in the S&P 500 outperformed overall returns by 8.2% compared with a full 100% allocation to the S&P 500 it is surprising that many investors remain underweight compared to this allocation. Add to this that the portfolio holding gold also offers a 15% improvement in the annual standard deviation of returns and you might be left wondering what’s the trade-off? 1

A Portfolio Approach

Certain prominent hedge fund managers, amongst them renowned American fund manager Mark Spitznagel, highlight the fact that adding a vastly underperforming and highly volatile asset actually has the probabilistic potential to enhance the return of a rebalanced portfolio. 2 Markowitz’s Modern Portfolio Theory illuminates the understanding behind this optimally allocated portfolio – through analysis of the correlation of returns of assets held in the portfolio.

For those buying gold fear not the volatility - Correlation is Key

This argument points to accepting the excessive volatility in certain circumstances. For example, recent research from Myrmikan Capital LLC suggests that investors would be wise to “embrace volatility” when it comes to allocating to gold mining stocks and ETFs.1 The key is ensuring that the asset added is anti-correlated with other portfolio holdings. Gold mining exposure also provides investors with a suitable alternative to holding gold bullion – offering enhanced liquidity through gold-mining shares and ETFs. As a clear example we might look at the Barron’s Gold Mining Index.

On initial impressions we are far from impressed that the fact that returns from this index have lagged the S&P 500 by a jaw dropping 87% since 1915 whilst also exhibiting twice the volatility. However, on closer inspection, and when applying the portfolio approach, we can see a 29% rebalanced allocation since 1915 would have enhanced returns by a whopping 72% and actually lowered the overall portfolio volatility compared to the S&P 500 alone. 1

Buying Gold - Tough to Stomach – The Short-Term View

It is not surprising that despite the maths being substantiated by a historical track record, many investors are put off by the higher volatility and lower returns of gold related assets over the shorter term. The problem is that history tells us that economic cycles of boom and bust will repeat. Prudent investors, capable of considering the longer term, and looking for a little extra peace-of-mind against these risks might consider at least marginally adjusting their allocations towards the 20% level. Easier said than done when traditional fixed income and equities asset prices are sailing higher, not to mention the rocketing returns to be found in the digital asset space.

Source:

1. Myrmikan Research, January 15, 2018, Embrace Volatility

2. Universa Philosophy

"Quant" has a Masters in Science from Oxford University. She worked as an analyst at a bulge bracket bank, as well as a quant researcher at one of the world's largest asset managers. She is currently studying for CFA level III and works part time as a quantitative researcher at a hedge fund.