By Steve Blumenthal

“Nearly all men can stand adversity, but if you want to test a man’s character, give him power.”

– Abraham Lincoln

Do you remember back in the early 80s when interest rates peaked at 15.25% and most everyone felt rates were moving higher, certainly not lower? The fact is, it was the single best time in history to get bullish on bonds.

Solomon Brothers’ head of research Henry Kaufman went from bond bear to bond bull and that call, unpopular as it was, later earned him “guru” status. The thing is, at that time, most people thought he was nuts.

Recall too that inflation was in the mid-teens and both stocks and bonds had burned investors over the prior decade. Fed Chairman Paul Volker stood tall in his fight to rein in inflation. Kaufman’s bullish call went on deaf ears. Few seized the opportunity.

I remember my mentor, John Ray (then a portfolio manager at Delaware Funds) telling me a story about an investment committee meeting where he stood before his colleagues and said we should put 100% of our money in long-term Treasury bonds and call it a day (or maybe call it 32 years as that investment beat stocks by a large margin). John’s bullish call went on deaf ears.

Let’s pause and look at the current situation from 35,000 feet. Back then we were trying to defeat inflation by driving ultra-high interest rates even higher. Today, we are trying to create inflation by driving ultra-low interest rates even lower. Who wanted to buy bonds in the early 80s? The past 1, 3, 5 and 10 years of performance were abysmal. It was the right thing to do. Everyone wants to buy bonds today. Just look at the fund flows.

Investors look at recent performance and project it forward. This has to stop!

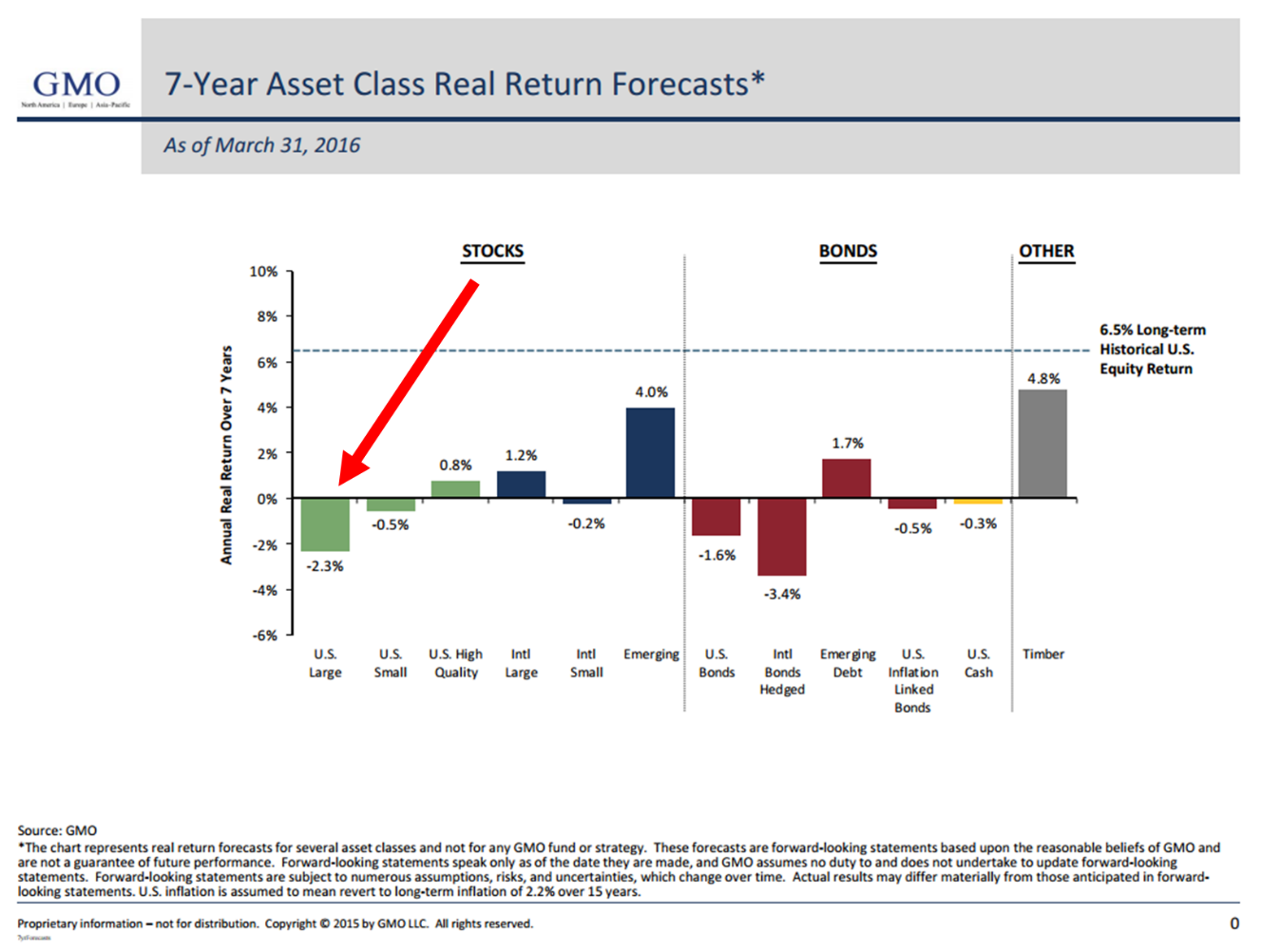

It’s a fine mess we find ourselves in. So here is the skinny. The bond market has little juice left to provide your portfolio with the help it provided you in the past. The same is true for the equity market as you can see next in GMO’s 7-Year Real Asset Return Forecast:

For the S&P 500 Total Return Index, that’s -2.3% per year for seven years. And, as you see, there is a lot of below 0% numbers across categories in the chart. Show this to everyone you know (especially your clients).

By the way, over the last decade, GMO’s forecasts had a 93.6% correlation to what they predicted and what actually happened. In non-geek terms, that’s pretty spot-on. No guarantees, of course, but we should take note.

All of this perhaps more eloquently expressed by Bill Gross in his latest missive entitled, “Bon Appetit!”

With interest rates near zero and now negative in many developed economies, near double-digit annual returns for stocks and 7%+ for bonds approach a 5 or 6 Sigma event, as nerdish market technocrats might describe it. You have a better chance of observing another era like the previous 40-year one on the planet Mars than you do here on good old Earth.

We are in the late stages of an economic game of musical chairs. Not many open chairs remain. We circle around and when the music stops, we race quickly to find an open chair. At the end of the game, there are few winners yet we all think we can play it and act quickly when the music stops. The Fed is in control of the music.

Many will lose but the game will be reset (higher interest rates and lower stock prices) and on we will go and play again. Let’s not lose the game. For now, be smart, play defense, be patient and know that there are many ways to make money. I share a few ideas in the conclusion below.

Today, let’s quickly take about the Fed (a behind the curtain view) and their probable course of action and then, in bullet point form, share with you my notes from Mark Yusko’s outstanding presentation at the recent Strategic Investment Conference (hosted by my good friend simply now known as Mauldin). By the way, I’ve ordered the audio recordings and will see if I can get permission to share a link to Yusko’s presentation with you. It was outstanding and, overall, I believe it is well captured in this next quote from Bill Gross.

The “fact of the matter” – to use a politician’s phrase – is that “carry” in any form appears to be very low relative to risk. The same thing goes with stocks and real estate or any asset that has a P/E, cap rate, or is tied to present value by the discounting of future cash flows. To occupy the investment market’s future “penthouse,” today’s portfolio managers – as well as their clients, must begin to look in another direction. Returns will be low, risk will be high and at some point the “Intelligent Investor” must decide that we are in a new era with conditions that demand a different approach. (Emphasis mine.)

With that, let’s get started. Grab a coffee or maybe two – I share a number of “what do we do” ideas.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Fed Up

- Mark Yusko’s Presentation – There Goes The Boom

- Trade Signals – Global Recession Probability High, No U.S. Recession Yet

Fed Up

I had dinner with Danielle DeMartino Booth last week in Dallas. Danielle is a former senior analyst for Richard Fisher and worked with him during his time as the Dallas Fed president.

Danielle co-hosted a private dinner and I was fortunate to be seated next to her. I have been reading Danielle’s weekly blog since I saw her last June on CNBC (via ZeroHedge.com). The piece was titled, “Another Fed ‘Insider’ Quits, Tells The Truth.” Read her blog, she’s really smart.

In a few short months, Danielle is coming out with a book titled, Fed Up. Our dinner discussion was honest, direct and candid. A bit of a peek behind the great curtain.

Honestly, I can’t tell you I feel any better and, in fact, I feel worse. Much of what I believe was confirmed.

Smart people were at the conference, like former Dallas Fed president Richard Fisher, and have tried to stress the business behavioral reactions to policy but, to be clear, there is not much hope in a change of monetary religion. Their hope to unleash animal spirits is not the outcome they are getting. They are guessing with blind faith in a flawed model.

Janet Yellen and her team of 750 plus PhDs are being tested. “… But if you want to test a man’s character, give him power,” said Lincoln. Of course, man is defined to be woman or man. Her character and her leadership, like Volker’s in the early 80’s, is at test.

Richard Fisher

The bottom line, in my view, is that the Fed lacks real world business experience. Banks are sitting on $2 trillion of the Fed created QE money and earning 50 bps. Free money… not getting into the system (i.e. loans). Zero (or near zero) bond interest rates have incentivized corporations to borrow for nothing and use the money to buy back stock and M&A. What future opportunity costs are being missed? What unintended behaviors have been created?

I was surprised to learn that there are over 750 PhDs on staff at the Fed. Academics educated in a Keynesian ideology. Expect helicopter money to come next and the direct buying of stocks.

Fisher has business common sense. And so does Danielle. Thus, Danielle has titled her soon-to-be-released book, Fed Up. Not sure if you feel any better. In fact, I don’t! I’m going to buy the book.

With thoughts on the Fed out of the way. Next is a summary of Yusko’s presentation in bullet point form. Short and to the point. So please email me if something is unclear.

Mark Yusko’s Presentation – There Goes The Boom

- Global trade has gone negative – it has never happened without a recession.

- Corporate earnings – six quarters of year-over-year decline: A leading economic indicator… it is probable that recession is coming.

- Bad companies are supposed to go out of business. Chesapeake Energy should not be able to borrow $4 billion.

- QE has kept too many poor quality companies in business.

- Interest rates are not going up. 2023 will be the secular low in interest rates.

- Yusko sees recession next year; however, if oil spikes higher, then recession will come sooner.

- Yellen will not raise rates this year. (SB here: to that end, we’ll find out in June or July. Christine Lagarde at the IMF and China have her by the short hairs – no rate increase or dollar will rise and China will respond in true currency war fashion and devalue the yuan).

- In February, Christine Lagarde put them all in a room (The Shanghai Accord) and said, “This ends now.” (Speaking about the currency truce and the plan to coordinate QE together.)

- Immediately following that February meeting, you saw a massive spike in futures buying activity. Yusko said, “Pretty amazing.” Here is a picture:

- On inflation – he said there isn’t any… there is no inflation. Everything is deflating.

- The Fed will be talking about QE4 by the third quarter. This slide was cute:

- The huge QE stimulus has had no impact on GDP but a big impact on the S&P. Notice that every time they end QE, stocks do not go up.

- QE ended in 2014. The stock market is not up since then.

- Regarding Japan: Wherever the yen goes, Japanese stocks go. Yen goes down, then stocks go up and vice versa.

- The Bank of Japan owns one-third of JPY bonds and 60% of all ETFs (SB here: I recently showed they own 59%. Think about how crazy this is…).

- He said, “Yellen will buy stocks just like the Japanese.”

- Regarding oil, Yusko predicted $26 per barrel of oil and that happened. He then predicted $50 per barrel of oil by year end. He didn’t think it would happen as fast as it did (we are near $50 today).

- Adding: Oil takes 10 years to recover. You get a spike, then back down, spike, then back down.

- He noted that “Doctor Copper” is telling us the world economy is in trouble.

- On the business cycle:

- Debt maturity calendar is large in the next few years – expect defaults.

- Election year market tendencies:

- The S&P 500 market high typically occurs in the fourth quarter prior to a new president taking office.

- Recessions almost always start in the first year of a new president.

- This is an interesting fact he noted: the compounded annual return on the S&P 500, December 1999 to present, is just 3.5% (nominal – or before inflation).

- GMO is predicting negative real returns for the first time since 1999. (SB here: I shared his story with you last week… In 1999, when he told his UNC endowment board of directors that equity returns would be a negative 1.9% annualized for the next seven years, he was scolded by a board member. Then, like today, he recommends a shift away from equities.)

- GMO is predicting -2.3% for the next seven years (that is an annualized loss per year so think of it as a loss of approximately 20% compounded. Try telling that one to your retirement board or brother-in-law).

- He noted margin debt is at a record high. (SB: something we have been talking about for months.)

- Adding, “Stocks go down 6.5 times faster than they go up.”

- He thinks we are looking at a 2000 to 2002-like period all over again.

- “The problem with human beings is we sell what we need and we buy what recently worked.” (SB: If you are an advisor, I bet you are nodding your head along with me in agreement with this quote. Imagine telling your parents that you want to go into a business that plays games on human behavior – one where you need to convince your clients to buy the investment strategies that haven’t worked recently and get your clients out of the ones that have worked. This goes for stocks, bonds and any type of investment.

- Put 80% of your money in a well thought-out, disciplined, long-term investment plan. Don’t give money to your friend’s business – “but you will” and “you will lose.” Don’t give money to a strange new idea – but you will and you will lose. So set aside at least 80% into diverse assets (he likes index funds) but he recommends 100% to a diversified “endowment like, investment plan. (SB: he was funny in explaining this. I did those things and I lost and I learned.)

- On debt: “there is too much debt everywhere.”

- On emotions, he commented, “Do not make investments that feel good, you will lose your money.”

- All of the money that went into the market in January, February, March and April of 2000 went into tech stocks. Cisco was at $100 per share. It went to $8 and is now $24. It is never going back to $100.

- Most investors say to themselves, “I’ll get out when I get back to even.” Don’t do that…

- Advice on manager selection, he said, “Never buy a manager with a good three-year track record, buy a good manager with a long-term record and a crappy three-year record… you will do better.” (SB: good advice.)

A selection of slides from his presentation along with a few comments from me:

- I’ve been noting for some time (like the subprime time bomb we discussed in 2006) that one of the large systemic risks is a sovereign debt crisis in Europe. To that end, I found this next slide from Yusko’s presentation interesting:

- Here is the chart on the presidential election cycle:

- Market doesn’t like rate hikes:

- On valuations (SB: this is data I share with you monthly)

- If share prices stay high and earnings decline, you get an even higher overvalued market:

- Finally, because I’ve tortured you with enough slides and I’m pretty sure my edit team wants to shoot me right now, I’ll conclude this section with one last chart.

Do you remember the “front page” theory? When it becomes consensus that the market will forever go higher, you end up with some bullish print on the front page of a popular magazine and when bottoms are reached, you see something along the lines of this bear market will never end. To that end, Yusko shared this next chart:

Trade Signals – Global Recession Probability High, No U.S. Recession Yet

Click through to find the most recent trade signals. You can see how we are positioned in our CMG Opportunistic Tactical All Asset ETF Strategy. High yield remains in a buy signal as does the Zweig Bond Model (favors long-term bond exposure). Equity market trend evidence is neutral at best. Our CMG Ned Davis Research Large Cap Indicator remains in a “sell”. Here is a link to the Trade Signals blog page.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Concluding Thoughts – Portfolio Ideas

I’m going to share a few portfolio ideas with you, but please understand that the following is not a recommendation for you to buy or sell any security as I do not know your personal needs, time horizon, risk tolerance, goals or assessed suitability. Past performance is no guarantee of future results. Speak with your investment advisor and craft a well thought-out investment game plan. Ok, here I go:

First, the path to success is discipline and diversification. How you size the risks (all investments involve risk, including CDs and cash) in your portfolio matters. Here are a few ideas:

- Consider managed futures, global macro and tactical strategies. They have been largely out of favor over the last three years – find good managers and consider overweighting to these categories. I favor a 40% to 50% weighting. I like a mix of currency strategies (due to non-correlation or diversification benefits) and approaches that can go directionally long or short equity and fixed income exposure.

- Find ETF strategies that have the flexibility to invest globally. Blend together a few (3 to 5) experienced ETF strategists that have disciplined processes with the flexibility to move to fixed income, cash, sectors, internationally and even cash. Make sure they don’t have the same process and make sure their strategies can position to defensive asset classes.

- For your equity exposure, hedge your individual positions with out-of-the-money put options and consider writing covered calls to increase your yield and reduce the cost of the put options (think of it as “stock catastrophe insurance”).

- Incorporate a disciplined way to go flat with some of your equity exposure. Internally, we use the CMG Ned Davis Research Large Cap Momentum Index. We go long a low-fee large cap stock ETF on buy signals and we buy a Treasury bill ETF on neutral signals (See Trade Signals section below). To us, cash or BIL gives us an option to buy at a bargain sometime in the future. It also reduces our risk exposure. Find a disciplined way to do the same.

- There are also mutual funds that can give you equity market exposure but also have hedging processes built in.

- As for individual targeted risks (single position speculative plays), I am bullish on India and Mexico. I like using ETFs to gain exposure. I am bearish on Italy and France (consider buying put options on ETFs that give exposure to those countries).

- I am short-term neutral but long-term bullish on gold. A 5% to 10% portfolio max weighting.

- Hedge funds are not going away, but many will not survive. Fees will likely continue to come down. It may not feel like we need hedged strategies, but we do. Personally, I favor liquid access to hedge fund managers available within mutual fund 40 Act structures. (You are going to pay up for talent – I’d focus on net returns.)

- Think in terms of how much you are going to allocate to your three asset buckets: stocks, bonds and liquid alternatives. I favor 30-30-40 today and will switch to as much as 70-10-20 when equity market valuations become attractive again. That will happen in the next recession. Margin debt will unwind, selling pressure will be quick so a portfolio designed for defense today will be able to take advantage of the opportunity that will present. Patience is required today as will be the strong stomach required to take action when the time is right. Like the market lows in 2002 and 2009, it was hard to buy, but valuations were best and potential returns the greatest. My best guess is 2017… tied to recession, default cycle, etc. Much depends on the Fed and our fiscal authorities.

For now, participate but protect. And as Yusko concluded in his presentation, adopt the endowment approach.