IEA “ Oil Glut ” Predictions Already Being Cut Dramatically…..Only 2 Months Later

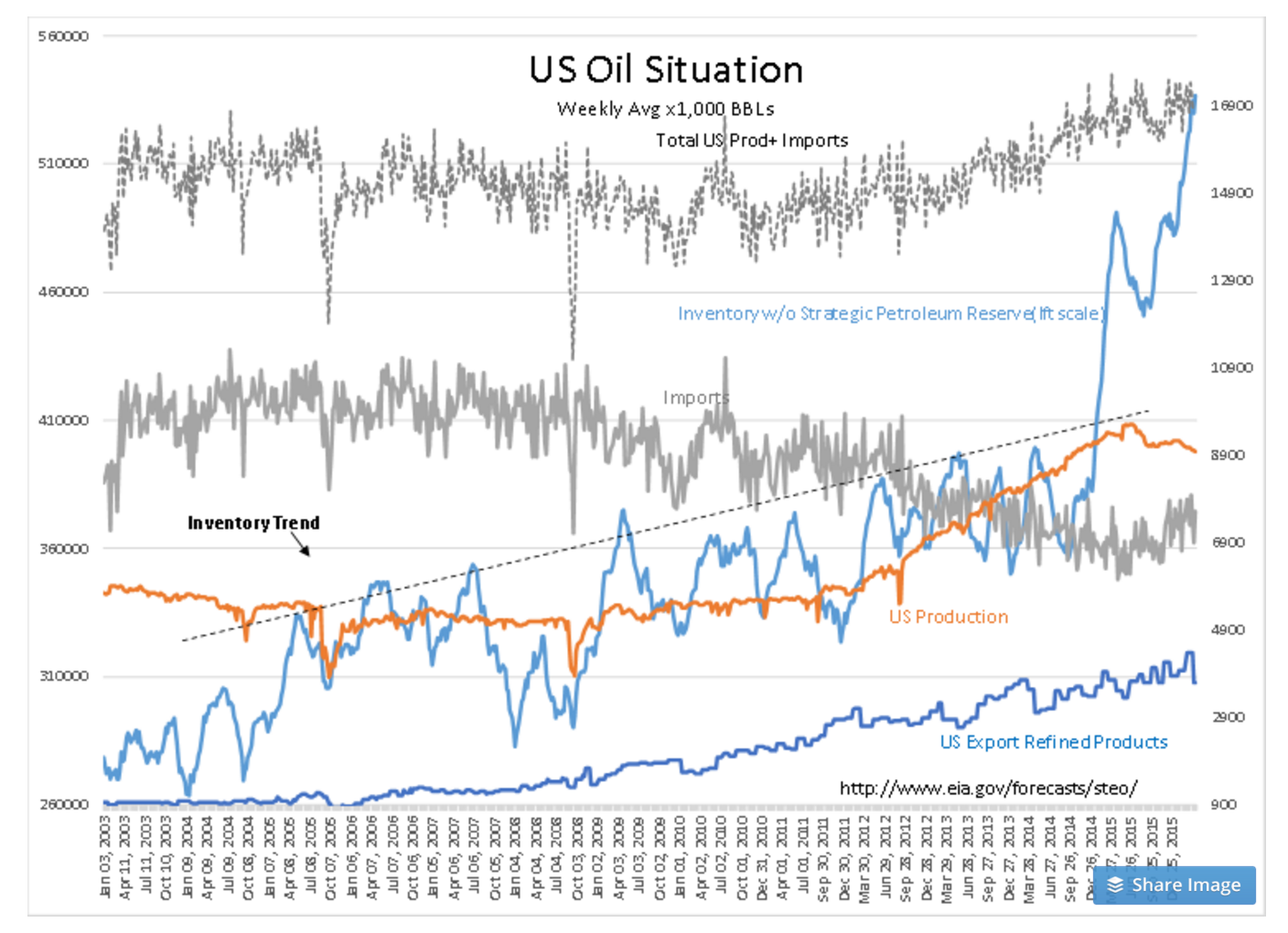

Here are two recent headlines on global oil supplies. Notice that the 1st was Feb 22, 2016 and the 2nd ~2mos later on April 14, 2016. The dire market psychology on the ‘Oil Glut’ has reversed in 2mos. But, look at the US Oil Situation chart which shows that while US production has shifted just below 9mil BBL/Day, US inventories which had been the market focus for bearishness have soared.

We just saw declining $WTI bottom in Feb and rise substantially! There is no support for a rise in $WTI in the US Oil Situation chart.

What this says is that most of what one hears is tied to trends in oil prices and not to fundamentals. The behavior of the majority of investors, perhaps more than 95% of investors, is to assume that price trends carry economic information and then look to determine which fundamentals they think are responsible. Herd mentality is always a strong force when individuals do not know how to read fundamental data. This is the basis for “The 1% Solution”.

Crude Glut Could Take Years to Disappear, IEA Data Show

OPEC official won’t rule out additional steps to stabilize the markethttp://www.wsj.com/articles/crude-glut-could-take-years-to-disappear-iea-data-show-1456152294 By Benoit Faucon, Summer Said and Bradley Olson

Updated Feb. 22, 2016 5:58 p.m. ET

IEA Sees Oil Oversupply Almost Gone in Second Half on Shale Drop

April 14, 2016 — 4:00 AM EDT http://www.bloomberg.com/news/articles/2016-04-14/iea-sees-oil-oversupply-almost-gone-in-second-half-on-shale-drop

I have been of the opinion that the so called ‘Oil Glut’ was within 1.5% of consumption and that 1yr’s growth of consumption of 1.5%-1.7% would eliminate the excess. I have always thought the panic was over-done and that it actually derived from changing views of inflation and the US$ by highly leveraged institutional investors, namely Momentum Investors. My view has only been reinforced by this significant and sudden change in market psychology. My assessment is that falling oil has been due to a US$ pricing shift which is now reversing as global trade fundamentals force it to normalize at lower levels.

It is hard to catch changes in market psychology and is the reason I focus on fundamentals. I see the US Oil Situation but making a forecast on where fundamentals are headed when it is not clear why we continue to import and build inventories is not something which I attempt. I make the assumption that oil production has economics with a 10yr+ time perspective and that I am likely not to understand it all till some time passes. I make the assumption that markets are self-adjusting and that most people do not knowingly run their firms into oblivion in the face of apparent Supply/Demand imbalances. I do not know why inventories are rising in the US, but have observed that past rises have been associated with rising refined product exports.

Past market interpretations about excess inventory was not correct in July 2014. Inventories only began to enter apparent ‘excess’ Jan 2015 and US production began to slow June-July 2015. US production is now 600,000BBL/Day lower while inventories have not only been maintained but have soared due to rising imports. I can also see that US GDP and World GDP are continuing to expand. US vehicle miles driven are at record levels. US refined petroleum products exports continue to rise and are at record levels. It is clear that global consumption has continued to rise!! It is clear to me that there is something else going on fundamentally than pure Supply/Demand considerations. I assume that the US inventory shift higher is due to planned expansion which is not clear at the moment to outside observers. I also factor into my thinking historical observation that consensus price-trend economics is always wrong!

I do not have all the answers for the US Oil Situation but I think markets have already adjusted and are moving ahead. $WTI prices are not reflecting fundamentals but changes in the US$.