Livermore Partners Q2 2019 letter to investors

July 25th, 2019

To Partners:

Second Quarter and YTD performance is on fire as our hedge fund, Livermore Strategic Opportunities, LP is experiencing its best year since 2016. It’s amazing given so many macroeconomic issues are abound and ever increasing.

In addition, we now have further proof of a slowing US economy adding to the world's angst. With this sequence of events, the candle has been lit and the FED is in full PUT mode with the markets racing to new all-time highs... Still, and in the face of slowing prospects of growth, I am pleased to share that as of June 30th, 2019 Livermore Strategic Opportunities LP ended the quarter with a gain of 40.4%.

Our gains for the year are even stronger given Q1’s solid performance. This provided a 2019 total compounded return of 78.46% YTD, our best year since 2016, which was our first full year and one in which strong opportunistic situations drove great returns. (commodities trader Glencore, activist-position Entertainment One and short-position Valeant Pharmaceuticals to name a few.)

2019 is not the same in terms of market dynamics as 2016 but there are some similarities. The key to which was a FED that drove a bulldozer to ignite inflation and increase growth, fueled an explosive bull market run. On the surface, and witnessing this movie play out back in 2009, it's no surprise the market believes the Federal Reserve's PUT mode (cutting interest rates to stimulate inflation and growth) will again lead to an earnings multiple expansion and supply investors a path to own equities in a big way. This has been the playbook of portfolio managers for a full decade now. They expect lower rates to support growth by remaining accommodative for both corporate borrowers and consumers.

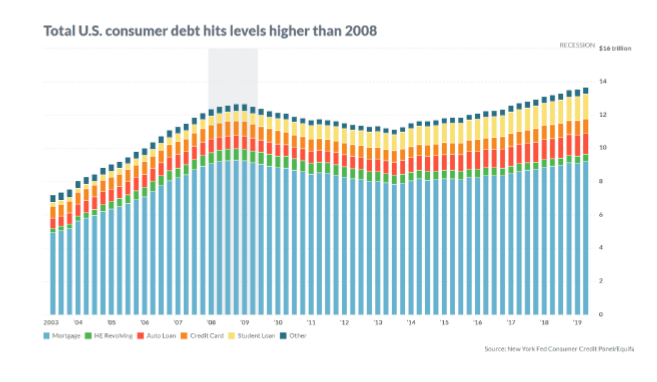

Though the past is a good indication of future events, I don't foresee this playbook working out the way investors hope, given the difficulty to spur higher growth when consumers have already been the beneficiaries of cheap debt for the past decade. As the chart below dictates, consumer borrowings are again at a peak, which calls into question how much a furthering expansion of the economy is possible.

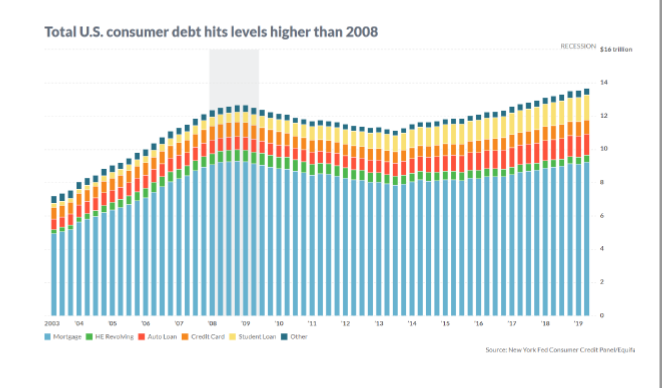

Though the past is a good indication of future events, I don't foresee this playbook working out the way investors hope, given the difficulty to spur higher growth when consumers have already been the beneficiaries of cheap debt for the past decade. As the chart below dictates, consumer borrowings are again at a peak, which calls into question how much a furthering expansion of the economy is possible.

Regardless, Livermore remains well-positioned and has continued to drive dramatic outperformance thru Q2. Our thesis on gold has begun to play out as has our specific stock selection both in event-driven names as well as select short exposure. This has been a great time to be a stock picker and let one’s ability to shine. Stock picking is working and helping to create alpha. It is what we strive for at Livermore. I am very happy for our investors but remain very cautious on the path forward. We continue to hold select short exposure and look to our hedging abilities or raising cash levels when prudent. Our gains on the year have been so strong and yet, our long portfolio continues to hold good value. It is indeed interesting times.

In the Q, Livermore witnessed a strong rise in gold (GLD) and gold miners. It’s been a big bet for us and makes up 20% percent of our total portfolio value. This investment played directly into our thesis when gold was at a low point in 2018 and held vast upside. A dovish Federal Reserve and worsening global macro events are a key driver for gold, as well as a “race to the bottom” on global currencies as devaluation takes hold. The threat of United States intervention in the currency market and de-valuation of the US Dollar is now fast becoming a reality. Therefore, Livermore feels we are only at the cusp of this new uptrend in gold that can last many years. So larger than ample exposure to gold is paramount.

Here is a link to a recent Newsmax television interview we gave in the quarter. Centering on our view of gold and the Federal Reserve’s reactionary nature.

On that subject, our late 2018 activist position in Detour Gold (alongside billionaire financier John Paulson) is playing out very well on the rise of bullion and the new Board and management team is executing accordingly. We are excited about the prospects for a further equity recovery as the company shifts into higher gear and cuts operating expenses to increase cash flows. Our investment in Detour at $11 a share in the fall of 2018 was well-timed as the stock ended the month of June 2019 at $16.50. Therefore, today we are sitting on a very strong gain of nearly 50% percent in a matter of just eight months. We continue to believe Detour offers further upside on pure fundamentals and as the sector begins to witness strong consolidation trends.

Our Tesla short position remained the largest in the fund as Q2 witnessed further weakness in the company's financials and business model. Livermore first initiated our position in 2018 with the stock over $300 per share with the view the value could crumble to $150 a share by 2020 (per our Q2 2018 investor LP letter). Tesla may be a growing business on revenue, but it is also a cash eating machine given its manufacturing nature. Thus, the path forward is challenged, especially with capex dropping seven quarters in a row. Not exactly a high growth company anymore! But with bearishness hitting a high point in mid-quarter, we decided to crystallize our short bet at $190 per share and realized a 40% percent gain. The belief being Elon Musk has many lives and is the ring leader of the Tesla circus. His next trick will be to attempt to calm fears on 2019 deliveries, gross margins, EBIT, and a path to sustainable profitability. Pushing the equity to bounce hard. Since then, the stock has indeed rallied, and Livermore has re-instated its short position more than 20% percent higher than our initial cover. It's not our largest short anymore but we will continue to review the size of the position as warranted. Our goal is to always capture alpha and tactically trading around positions like this helps us gain an edge and increase total returns.

Burberry remains a core long position for Livermore. The company is experiencing a renaissance of renewed vitality with new CEO Marco Gobbetti leading the charge. Expectations have been high, and the turnaround will take time. The stock has endured a small gain to date thru June 30th, and we feel over time, new creative director Riccardo Tisci will present an eclectic collection of higher margin and in-demand products to strengthen lasting profitability. We are driven to see Burberry succeed. It has been a holding ever since the beginning of Brexit in the summer of 2016.

Jadestone Energy (JSE.LN) remains a large holding of the fund and one that we continue to watch grow and mature. The equity has been on a tear since its 2018 IPO (up more than 50%) in London and has continued into Q2. Jadestone is unique and well-positioned given its strong free-cash flows, FCF yield, and management team. The newly acquired Montara asset has already shown strong signs of asset rationalization with major upside to boot. JSE management, led by Paul Blakeley, recently provided guidance of 13-15,000 BPD of production for Jadestone in 2019, with the potential for further bolt-on acquisitions to further strengthen the asset mix and leverage cash flows. We continue to be supportive and feel Jadestone can become a solid $1B company Brent oil producer with scale.

Other companies adding to our gains this quarter were: hometown Chicago-based generic pharmaceuticals company Akorn, gold producers Torex Gold, Solgold, and Ukrainian premium iron-ore pellet maker FerrExpo, which was hit hard in May and Livermore acquired a position on dramatic weakness. It has since rebounded mightily, adding to our returns.

In closing, 2019 has already presented us with solid opportunities for our event driven hedge fund. The outlook continues to be dynamic and one in which we must stay nimble. There are trade wars with China and the potential for real wars (given the flare-up with Iran). We must be on the lookout for challenges to the uptrend in this record bull market run.

Therefore, and as always, Livermore will be focused on unique special situation opportunities, especially where activism is possible, to drive further value and reap alpha-generating returns. Thank you again for the continued support.