A Critical Forensic Look At Radiant Logistics Strategy, Management, And Financial Accounting Strain Suggests 30-50% Downside Risk by Spruce Point

Summary

Radiant IPO’d through a reverse merger, using a similar logistics roll-up strategy; we’ll illustrate it’s non-economic and worse performing than Echo Global’s, a previous short call we made down 30%.

Radiant’s CEO and co-founder were involved with Stonepath Group, a public company that failed spectacularly 10 years ago when it admitted accounting irregularities tied to revenue overstatement and expense understatement.

Radiant’s share price is up 85% in the past year, yet investors are overlooking signs of financial strain such as diverging GAAP/Non-GAAP results, plunging cash flow, and guidance suspension.

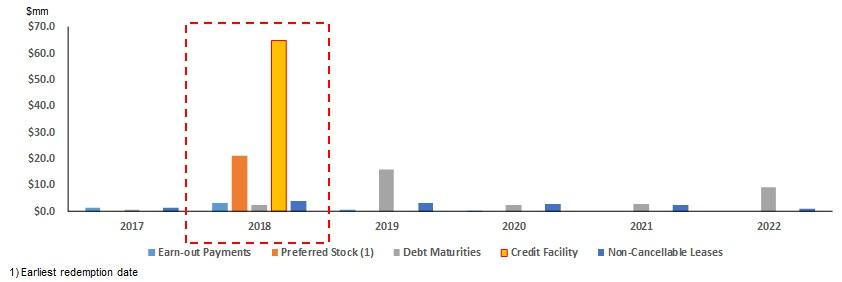

Radiant’s financial policies, capital management, and accounting are irregular. When investors focus on debt maturities due in 2018, we wouldn’t be surprised to see substantial dilution as cash flows sag.

Radiant’s valuation is irrational. It currently trades at a premium to peers, despite having no top-line growth, an inferior model, and financials divorced from reality. We see 30-50% downside.

Spruce Point Capital Management is pleased to announce it has released the contents of a unique short idea involving Radiant Logistics, Inc. (RLGT or “the Company”), a poorly constructed roll-up in the third party logistics (3PL) and transportation industry. With its share price up approximately 85% in the past year, we have conducted an extensive fundamental and forensic accounting review and believe investors are overlooking significant downside risks. As a result, we have a “Strong Sell” opinion and a price target of approximately $3.00-4.50 per share, or approximately 30-50% downside. Please review our disclaimer at the bottom of this email. We also encourage all of our readers to follow us on Twitter @sprucepointcap and register on our website.

Executive Summary And Tenants Of Short Thesis

We previously laid out our Seeking Alpha short case on Echo Global Logistics (NASDAQ:ECHO) in September 2016, a highly promoted but poor performing roll-up in the 3rd party logistics (3PL) sector. Echo’s share price recently touched $17.90 and has fallen by up to 30%.

Spruce Point believes that Radiant Logistics, another promotional 3PL roll-up story, is an even worse investment and much weaker company.

Questionable Management History Tarnished By Previous Accounting Scandal

- Radiant’s CEO Bohn Crain and first General Counsel Cohen were executives at Stonepath Group (formerly AMEX: SRG ; now OTC:SGRZ), which crumbled when it admitted financial and accounting irregularities tied to revenue overstatement and expense understatement. An SEC inquiry commenced, allegations of fraud were made, and Stonepath was eventually delisted and faded to the pink sheets and insolvency

- Later, with a “reverse merger” from the shell of “Golf Two, Inc”, the duo launched Radiant Logistics on the bulletin board in 2005

- The SEC has already questioned Radiant’s accounting, and it has made the scary disclosure that its margin method “Generally results in recognition of revenues and purchased transportation costs earlier than the preferred methods under GAAP which does not recognize revenue until a proof of delivery is received or which recognizes revenue as progress on the transit is made.”

- Don’t expect Radiant’s minor league auditor named Peterson Sullivan to spot problems. Radiant pays it miniscule audit fees, and three of its employees (including two partners) have recently been sanctioned by the SEC and PCAOB in less than two years

Similar To Echo, Radiant Is A Non-Accretive Roll-Up Strategy In The 3rd Party Logistics Space Showing Strains

- Radiant has completed 16 acquisitions since 2006 and has not demonstrated any cumulative net cash flow, a key measure of success

- Its largest acquisition of Wheels in 2015 has failed to hit expectations and exposed Radiant to the transportation brokerage market, an area coming under extreme margin pressure from new technology entrants. Radiant levered up and diluted shareholders meaningfully. It’s noteworthy that Wheels Group was itself a reverse merger on the Toronto Venture exchange and also promoted as a 3PL roll-up

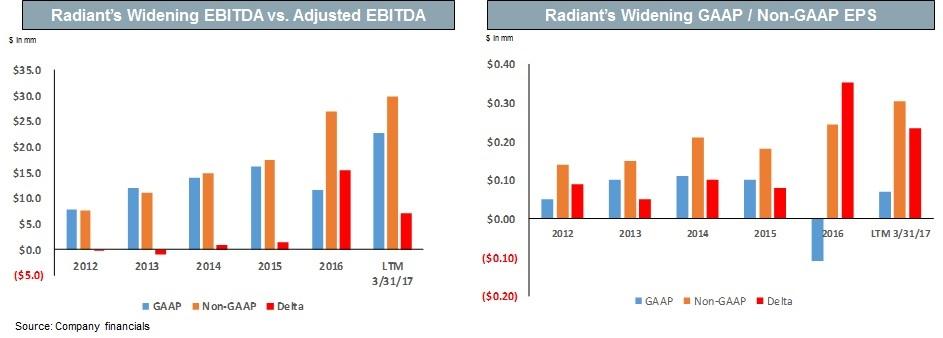

- Radiant’s GAAP/Non-GAAP financials are diverging at an alarming rate, and it recently announced “organizational changes” (Warning: it had to hire a “Chief Commercial Officer” and its COO resigned) while suspending Sales and EPS guidance to investors for FY 2017

Unattractive Capital Structure And Unfavorable Shareholder Policies

- Radiant’s expensive 9.75% perpetual preferred stock sucks cash flow from common shareholders; the Company will likely have to use its existing shelf registration to dilute shareholders again when the preferred first becomes callable at the end of 2018

- Radiant has a history of irrational dilution; eg. in July 2015 to pay down its credit facility costing just 3.5%; clearly, its equity is cheaper!

- Radiant announced a 5m share buyback in January 2016, yet has repurchased just 91k shares. It could have bought back all the stock it wanted at $3/share or less but it didn’t – shareholders should be asking why?

- Key insiders have been selling. Notably, Radiant’s second largest shareholder/original executive Cohen sold all his shares in 2015 and now hides his association from Radiant on his biography. The Company’s new COO also sold his entire shares one year after joining

Unattractive Valuation And Limited Reason To Own The Stock

- With shares up nearly 85% in the past year, investors seem blinded to the fact that recent cash flow is declining 20% YoY

- The market is expecting virtually no revenue growth from Radiant and has failed to take a close forensic look at the Company to identify issues that suggest further strain lies ahead. However, Radiant trades at an irrational premium to logistics peers

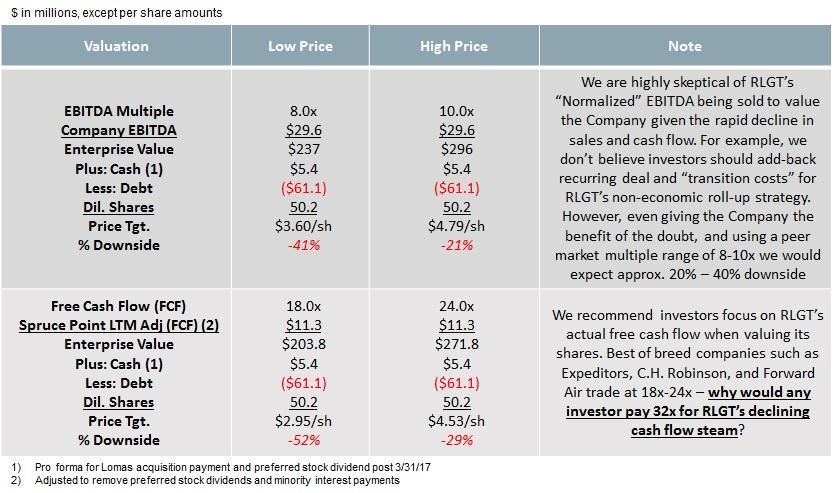

- We suggest valuing it on free cash flow multiple, which, at an 18-24x, would be worth approx. $3.00-4.30/sh, implying 30-50% downside

Capital Structure Overview And Valuation

We will demonstrate in this report that RLGT’s financial condition is fragile and its valuation is nonsensical. Investors may start focusing on FY 2018 very soon as a critical year for capital needs. Radiant has $48m remaining on its shelf registration, and we would expect further dilution to manage debt obligations.

(1) Less $7m paid for Lomas acquisition post 3/31/17 and $511k for preferred dividend.

Debt Maturity Profile

Details on Management’s Questionable History

Prior to starting Radiant Logistics in 2006, Bohn Crain was the EVP and CFO of Stonepath Group from 2001 to 2004, a publicly traded logistics roll-up that failed spectacularly during his leadership. Stephen M. Cohen was Stonepath’s general counsel and joined Crain to start Radiant.

9/20/04: Stonepath Group Announces Intention To Restate 2003 And Q1-Q2 2004 Financial Statements

- Stonepath determined that it had understated its accrued purchased transportation liability and related costs of purchased transportation; it relied on trend analysis to estimate its costs of purchased transportation

- The Company concluded that the process did not accurately account for the differences between the estimates and the actual freight costs incurred. This allowed for the accumulation of previously unidentified costs of purchased transportation and an under-reported liability for the accrued costs of purchased transportation.

- Stonepath’s CEO Mr. Pelino seemed to back Crain: “The Company has also restructured its financial organization to have the senior financial staff of its Domestic Services and International Services operations report directly to Bohn Crain, the Company’s Executive Vice President and Chief Financial Officer.”

11/17/04: Two Months Later, Bohn Crain Abruptly Resigns And Significantly More Financial Accounting Issues Emerge

- Revenue Overstatement: In the course of its review of the under-accrual of purchased transportation costs, the Company also identified two revenue recognition errors within its Domestic Services which caused the Company to overstate its revenues by approximately $1.1 million during the first two quarters of 2004

- Net Income Overstatement: The Company also expects to report an additional $3,600,000 reduction in net income for the income tax effects of the estimated adjustments discussed above. These adjustments primarily affect the fourth quarter of 2003. At that time, a $3,000,000 adjustment was recorded representing a reduction in the deferred tax asset valuation allowance and the reporting of a deferred tax asset.

- Restructuring and Guidance: Stonepath implements a restructuring, and a material charge is expected to negatively impact Q4’14 results. Stonepath decided to withdraw EBITDA and EPS guidance for 2004 and 2005

1/6/05: 10-Q Filing Reveals SEC Inquiry And Numerous Lawsuits

- SEC Inquiry: SEC conducted an informal inquiry to determine whether certain provisions of the federal securities laws have been violated in connection with the Company’s accounting and financial reporting. The SEC requested information relative to the restatement amounts, personnel at the Air Plus subsidiary and Stonepath Group, Inc., and additional background information from October 5, 2001, to December 2, 2004

- Lawsuits: Crain and other executives named in eight lawsuits alleging fraud, gross mismanagement, waste of corporate assets among other things

2/25/05: Amended 10-Q Reveals Even More Financial Errors During Bohn’s CFO Tenure

- Revenue Overstatement: 1) the Company identified a billing error in which the operating unit was invoicing one of its automotive customers at rates which had been approved by a customer representative who did not have the authority to do so; 2) Upon billing to a customer for certain capital equipment purchased in connection with the launch of a new distribution center for that customer, the unit recognized the revenue immediately rather than over the two-year life of the contract

- Expense Recognition: 1) Claims expenses from Q1’14 were shifted to and recognized in Q4’14, 2) Depreciation associated with the capital equipment mentioned above was depreciated over its useful life, rather than matching it to the life of the contract

Stephen M. Cohen was Radiant’s first General Counsel and Board member starting in 2005. He recently sold all his sizeable share holdings in 2015 and has removed his association with Radiant

- From 2000 to 2004, Mr. Cohen served as senior vice president, general counsel, and secretary of Stonepath Group. Mr. Cohen’s tenure at Stonepath overlapped with Bohn Crain’s during the period of financial misstatements and failure of Stonepath

- Mr. Cohen joined Radiant in October 2005. He took no salary as part-time counsel but received payments to his firm SCM Capital Advisers for legal and consulting services. He also owned 2.5m shares or 7.4% of Radiant according to early 10-K company filings

- Cohen started exiting his shares in July 2015 through a secondary issuance and, as of the last proxy filed 10/6/15, has fully exited. The sale of the shares came notably after Radiant’s highly promoted Wheels acquisition early in the year

- Mr. Cohen is now partner at Fox Rothschild and is the co-chair of the firm’s Public Companies Practice. Radiant used Fox Rothschild as its M&A legal advisor for the Wheels transaction and as its securities lawyer in the transaction Cohen sold shares

Signs Of A Suspect Accounting And A Non-Economic Model Coming Under Pressure

- Radiant bears striking resemblance to Echo Global Logistics, a company we were early to identify as a short

- In our opinion, Radiant is a significantly worse investment opportunity and weaker company

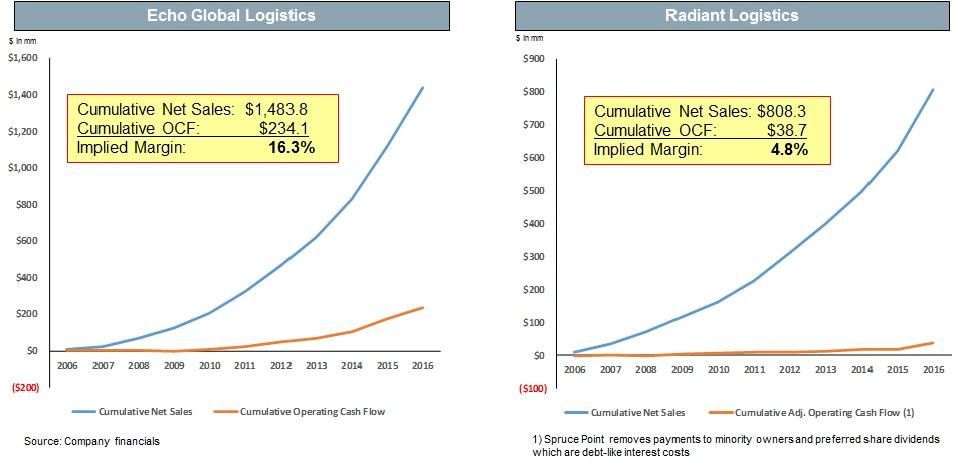

- Radiant’s effectiveness as a roll-up strategy can be compared with Echo’s. In the chart below, we illustrate the cumulative sales and operating cash flow for each company

- We find clear evidence to suggest that Radiant is an inferior roll-up with significantly lower cash flow margins

- There are glaring signs of financial issues with Radiant’s financial statements that must be critically evaluated

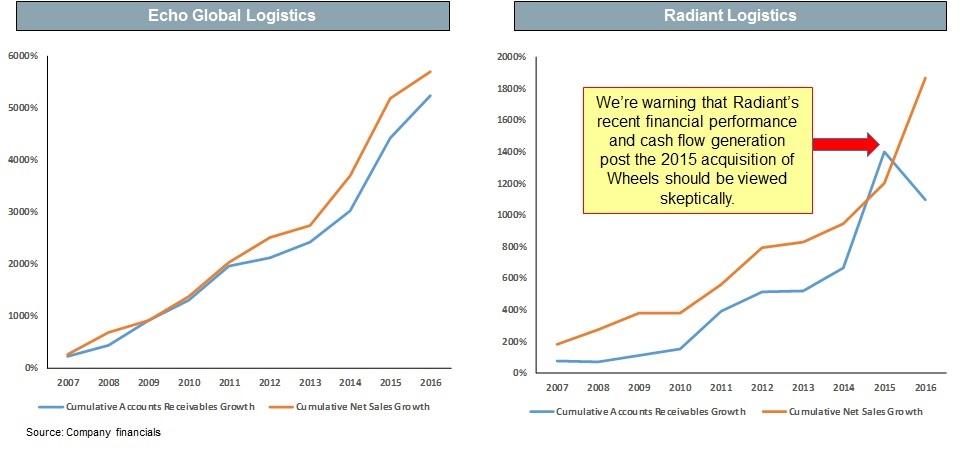

- Spruce Point believes that evaluating a company’s long-term accounts receivables vs. sales growth is a reliable indicator to identify potential financial misstatement. Both financial metrics should track each other closely

- ECHO and RLGT were founded in 2005 as asset-light logistics roll-up stories and make for excellent comparisons. It’s evident from the charts below that Radiant’s financials have deviated meaningfully over time and very significantly post-2015.

- The SEC weighed in years ago about Radiant’s revenue and expense recognition and warned that it was Non-GAAP. The comment letter should be read carefully

- The Company has ever since claimed its aggressive methods are “immaterial” – can this be trusted? Recall that bad “estimates” got Crain’s last company Stonepath Group in trouble

- It baffles us that Radiant’s auditor says its financials conform with GAAP when there are clear signs it may not. Read further to see the concerns raised by RLGT’s auditor Peterson Sullivan

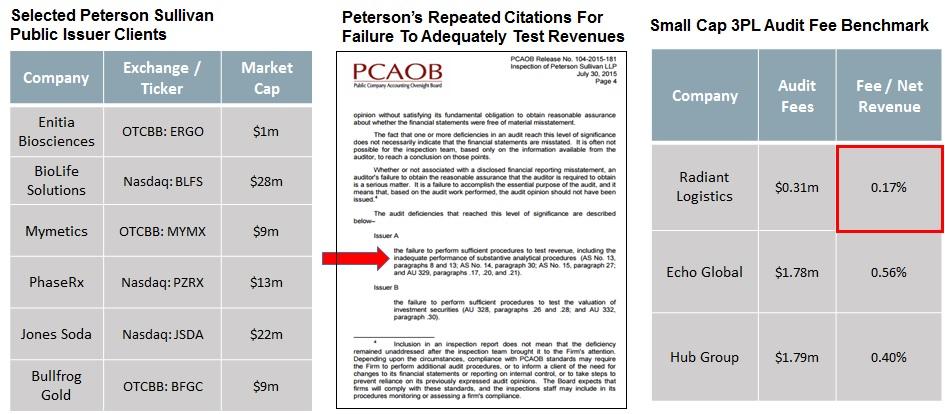

A Special Note on Radiant’s Auditor: Peterson Sullivan

- Radiant is based in Washington state but boasts its national presence and that it should be treated and valued as if it were a recognized industry player

- It has chosen a local auditor, Peterson Sullivan, to validate its financials. Peterson represents many speculative penny stocks and has recently been cited multiple times by the PCAOB for deficiencies in testing revenues – the most basic element of an audit (PCAOB Report: 2013 and 2015) Ironically, Peterson does not list either transportation or logistics as one of its industry specialties on its website and charges Radiant a negligible audit fee

- It’s also worth mentioning that Peterson is a small firm with just 21 partners, yet in less than two years, it has had three professionals (including two partners) sanctioned by the SEC and PCAOB for unprofessional conduct

- In light of the many irregularities we’ve observed with Radiant’s financials, investors should tread carefully

- Spruce Point warns that companies undergoing financial stress often times show an escalating divergence between GAAP and Non-GAAP figures. We observed this sign recently with our short recommendation on Echo Global

- As can be seen from the charts below, Radiant’s Non-GAAP financials really started diverging heavily in 2016, a year after it acquired Wheels Group

- Radiant’s largest deal to acquire Wheels Group seems to be a major disappointment and a source of stress for the company

- In January 2015, Radiant announced its largest acquisition on Wheels Group for ~$76m, a microcap Canadian company that served both the US and Canadian markets (50/50%) with brokerage and contract logistics services. Radiant levered its balance sheet to 2.5x Debt/16E EBITDA and diluted existing shareholders by issuing 6.9m shares to Wheels owners. Radiant then issued further 6m shares in July 2015 to pay down debt

- In our opinion, much like Echo acquired Command Transportation (May 2015) at the peak of the brokerage market, Radiant’s acquisition of Wheels also exposed it to the brokerage market near the peak and was ill-timed

- Financial control issues appeared early on in the deal. For example, Radiant’s press release first said it expected $750m of revenues from the deal, and a few days later, its investor presentation was changed to $800m at the midpoint

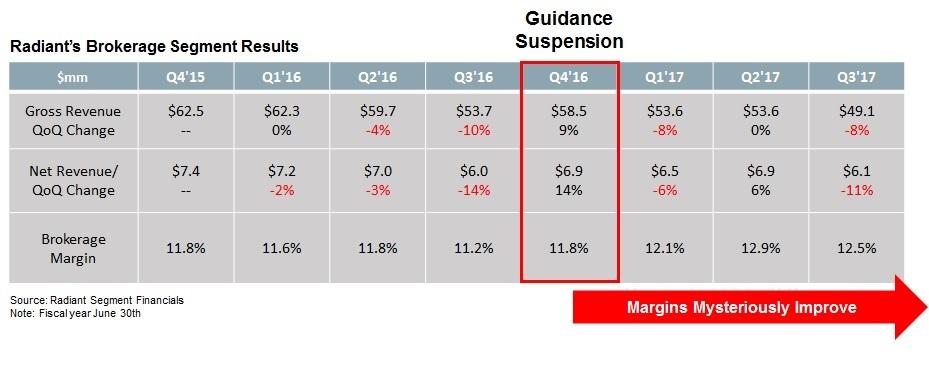

- Radiant suspended offering annual and quarterly guidance in Q4’2016 citing the uncertain brokerage market and excess capacity in truckload and intermodal. Yet, somehow Radiant has been able to improve margins in this segment while others in the industry cite margin compression

- The only explanation cited by Radiant is “lower purchased transportation costs” – if true, how much longer can these benefits last?

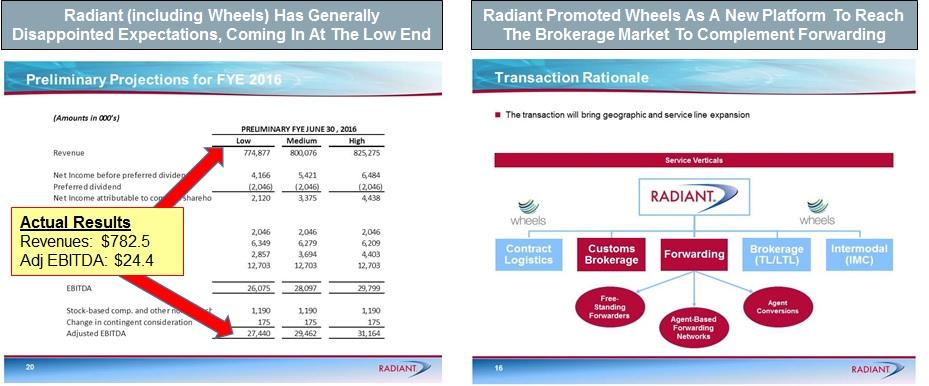

Radian’t Current LTM Gross Sales Of $758m Is Almost $100m Less Than Expectations 16 Months Ago:

- 2/16/16: Started reducing guidance for gross revenues to $836.0-852.0 million with net revenues of $188.8-192.4 million. Adj. EPS $0.20-0.23 per share

- 4/25/16: Reduced $25m of debt through pre-payment – likely a defensive measure seeing trouble ahead

- 5/16/16: Adjusted guidance normalized adjusted EBITDA in the range of $27.5-29.5 million on (gross) revenues of $788.9-829.1 million. Adj. EPS $0.22-0.24 per share

- 9/13/16: Declines to offer annual or quarterly guidance

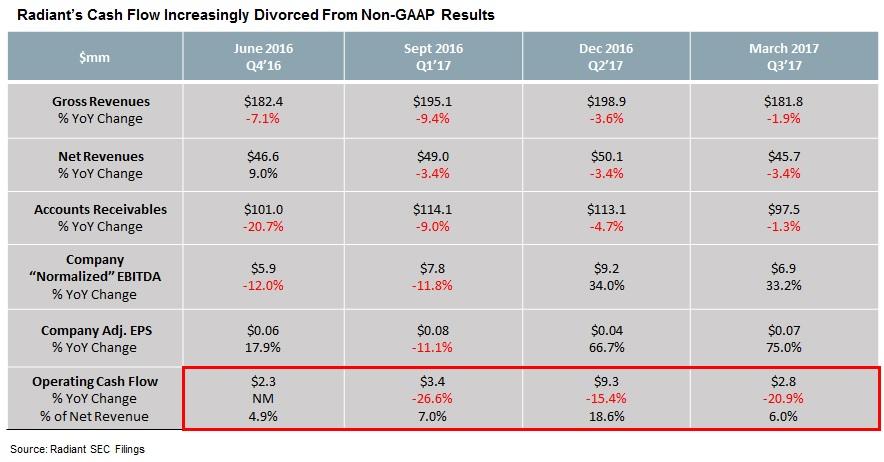

- In pushing Radiant’s stock up almost 85% in the past year, investors have narrowly focused on the Company’s highly Adjusted EBITDA and EPS, while ignoring its anemic top-line growth and plunging operating cash flow

- We don’t believe Radiant’s recent performance is sustainable, as its comparisons become significantly more difficult in the next few quarters to show growth, while its end markets struggle with excess capacity and limited visibility. Cash flow will become increasing important as 2018 approaches and its credit facility matures

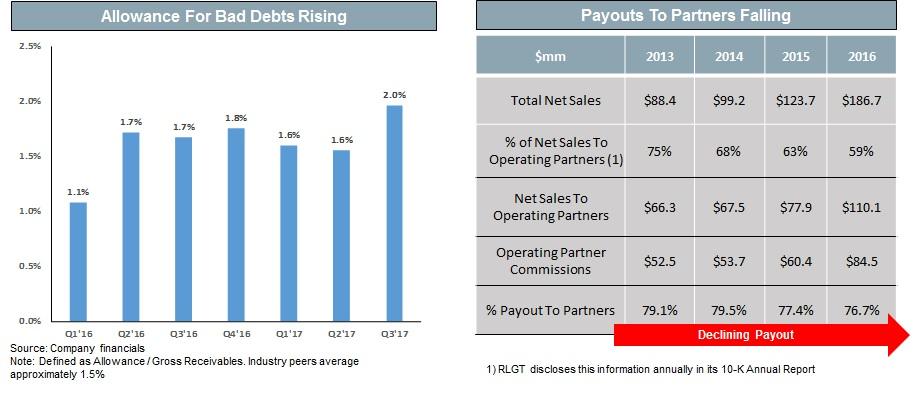

- More signs of financial strain appear by looking carefully at the Company’s bad debts and its drivers

- RLGT’s bad debt is surging and is a function of its strategic operating partner arrangements as noted in the Company’s Risk Factor below:

If our strategic operating partners fail to maintain adequate reserves against unpaid customer invoices, or if we are unable to offset against commissions earned and payable by us to our strategic operating partners for unpaid customer invoices, our results of operations and financial condition may be adversely affected.

We derive a substantial portion of our revenue pursuant to agreements with independently-owned strategic operating partners operating under our various brands. Under these agreements, each individual strategic operating partner office is responsible for some or all of the bad debt expense related to the underlying customers being serviced by the strategic operating partner. (RLGT 10-K, p. 9)

- We observe that Radiant’s commission payout to its operating partners has been declining. While this may have a short-term benefit to earnings, its long-term effect is reasonably quite bad since operating partners can generally terminate their agreements with Radiant at any point as note in its Risk Factors

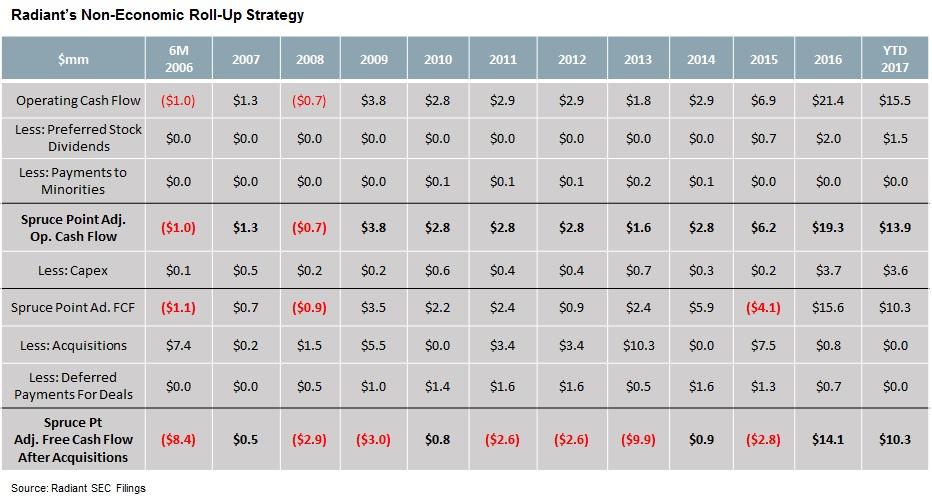

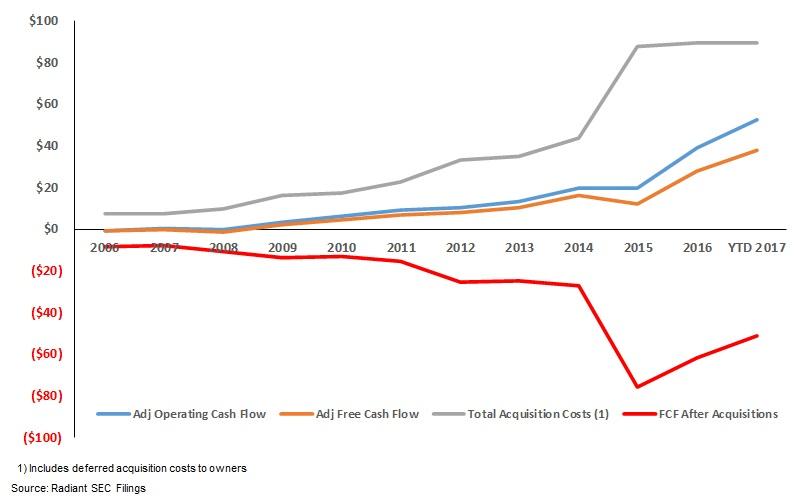

- Spruce Point has successfully argued that the best way to evaluate serial acquirers is to look at free cash flow after acquisition costs. It is a particularly useful metric when evaluating asset-light industries where acquisitions consist mostly of people and relationships vs. PP&E

- Radiant’s operating cash flows must be adjusted for its fixed 9.75% preferred payments (effectively debt-like interest costs) and payments to minority holders that flow through the financing section. We find that Radiant has burned a total of $51m in its lifetime (2006-YTD17) – no evidence it has added any value

- Radiant stands little chance to dig itself out of its hole in our opinion

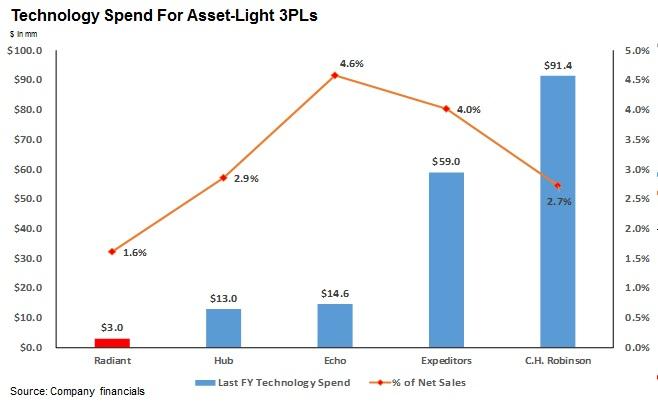

- Spruce Point was early to identify the effect that peer-to-peer technologies and big data would have on the old school 3PL industry when we exposed ECHO and its technology “hype” – especially now that Uber Freight (Private:UBER) and Amazon Logistics (NASDAQ:AMZN) are becoming a reality, margins for transportation brokerage are compressing

- Like most 3PLs, Radiant boasts that its competitive strength is its technology. However, both Spruce Point and Radiant warn that for serial acquisitive accompanies, the challenge of integrating various technology and IT systems can present major issues. Radiant goes so far as to add the following risk factor:

“Our management information and financial reporting systems are spread across diverse platforms and geographies, and we depend on information provided by strategic operating partners and acquired companies, not all of which have systems that are compatible with ours.” (10-K)

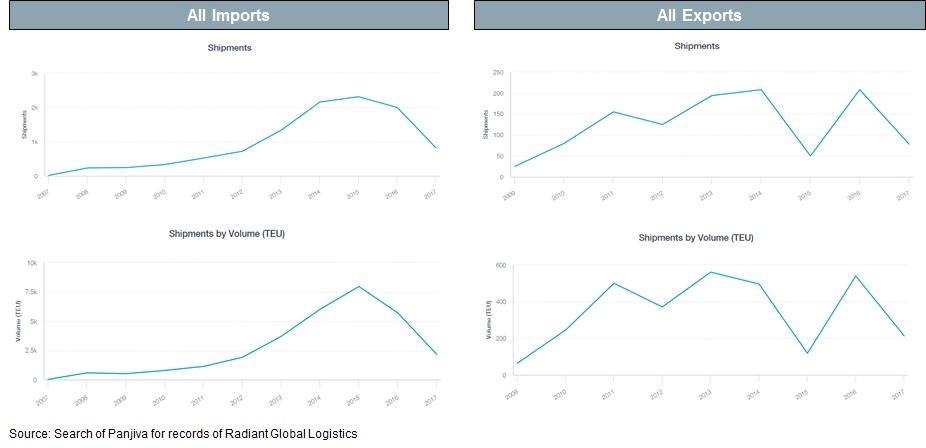

- Like most speculative companies, Radiant doesn’t offer many critical metrics such as shipments to help investors track their operational progression

- Spruce Point has accessed data from Panjiva, a global trade data firm to source bill of ladings which we believe give good insight into Radiant’s activities

- Our results show that US import shipments peaked and have rolled over materially since 2015. Export data also appears weak

Debunking The Bull Case And Valuation Price Target

What the stock promoters and bulls say:

Growth opportunities through accretive acquisitions – Radiant has grown through acquisitions and plans to continue its strategy. Acquisitions are quickly accretive as it targets generally small agent based forwarding businesses that are generating ~$1M to $3M in annual EBITDA and pays 4x-5x TTM EBITDA. Increase in its network size should improve economies of scale.

Spruce Point’s Rebuttal:

There’s hardly much evidence to suggest that Radiant as been a successful roll-up after a decade in existence. It has not generated any positive free cash flow after capex, preferred dividend, and earn-out costs. It is getting harder for Radiant to find small acquisitions and pay just 4-5x, and the Company’s own valuation of 11.4x unjustly rewards it for having created little value.

What the stock promoters and bulls say:

Proprietary IT system should enhance operational efficiency – As competition in the industry increases, the demand for industry specific IT solutions will. Radiant has already set up a scalable IT platform which is SAP (NYSE: SAP) based. Consequently, the Company has a competitive advantage vs. smaller competitor.

Spruce Point’s Rebuttal:

All 3PL companies say they have “proprietary” tech systems that give competitive advantages. The reality is that Radiant’s small size and $3m technology spend is dwarfed by its public peers and new, well-funded, start-ups that have raised significant capital to invest in the next generation of logistics solutions.

What the stock promoters and bulls say:

Radiant the next stock juggernaut like XPO Logistics (XPO) circa 2012. Founded in October 2005. Bohn Crain (founder and CEO) has quietly been building an XPO-like company but without the fanfare.

Spruce Point’s Rebuttal:

A very promotional statement, which compares a $300m company vs. $11bn diversified giant. The reality is Radiant has failed to capture the same level of institutional support in 10 years and will likely never scale.

What the stock promoters and bulls say:

The recent acquisition of the Wheels Group, Inc. (the company’s 11th and largest acquisition) significantly expands Radiant‘s scale, density, and service offerings and provides the platform for continued/accelerated growth in both the US and Canada.

Spruce Point’s Rebuttal:

Unfortunately, it has also exposed Wheels to the truck brokerage market at exactly the wrong time – when margins have compressed and visibility has vanished. The deal came at a punitive cost to investors, and now Radiant’s financials are indicating strain.

What the stock promoters and bulls say:

Expanding margins should follow: Using this calculation of EBITDA to net revenues, adjusted EBITDA margins have expanded from 2.6% in F08 to 14.4% in F16.

Spruce Point’s Rebuttal:

Radiant has admitted that its recognition of revenues and expenses don’t conform to GAAP and are aggressive. We suggest looking at operating cash flow instead. Last quarter’s operating cash flow margin was just 6.0%, near its lowest level in seven quarters.

What the stock promoters and bulls say:

Stonegate Securities (May 2017): Our acquisition analysis framework (trying to capture the acquisition model), applied to our F18 adjusted EBITDA estimate arrives at a valuation range of ~$7.50 to ~$9.50 with a midpoint of ~$8.50.

Spruce Point’s Rebuttal:

We’ve demonstrated the acquisition model doesn’t work, and modeling out a business to 2018 with no visibility is a challenge. Peers on avg. trade at 8-10x EBITDA and 18-24x FCF, but Radiant trades at an irrational premium. Just by assuming a peer range multiple, it’s easy to see 30-50% downside.

Peer Valuation Supports Irrational Overvaluation

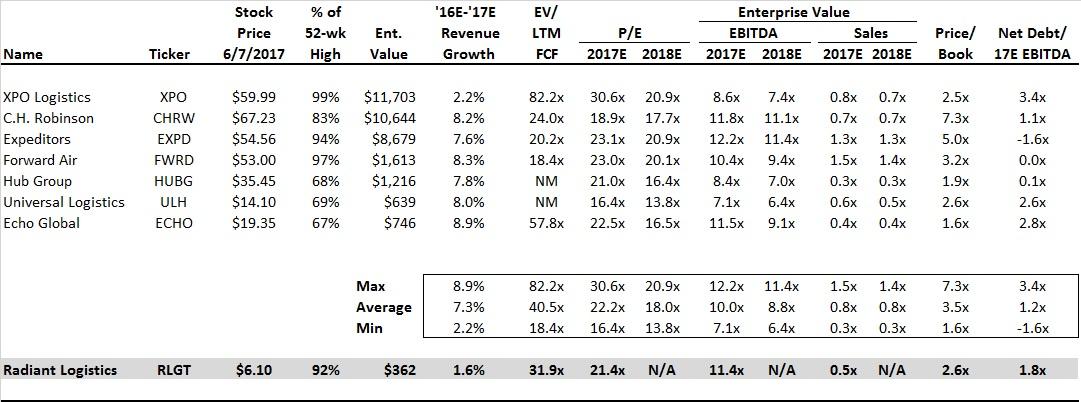

Radiant trades at an undeserved premium to its peers and has substandard growth, accounting, and management concerns. It is hard to justify an 11.4x EV/17E EBITDA multiple for Radiant, which is comparable to ECHO. Our peer set includes XPO Logistics, C.H. Robinson (NASDAQ:CHRW), Expeditors (NASDAQ:EXPD), Forward Air (NASDAQ:FWRD), Hub Group (NASDAQ:HUBG), and Universal Logistics (NASDAQ:ULH).

$ in mm, except per share figures

Source: Company financials, Wall St. estimates, CapitalIQ

Note: Financials estimates are calendar year

Spruce Point Estimates 30-50% Downside Risk Potential

In our view, once investors realize that Radiant is a very low quality investment opportunity fraught with high risk of financial misstatement, its multiple will correct closer to peers. Cash flow is the best way to value the company given financial statement distortions.

Disclaimer

This research presentation expresses our research opinions. You should assume that as of the publication date of any presentation, report or letter, Spruce Point Capital Management LLC (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our subscribers and clients has a short position in all stocks (and are long/short combinations of puts and calls on the stock) covered herein, including without limitation Radiant Logistics, Inc. (“RLGT”), and therefore stand to realize significant gains in the event that the price of its stock declines. Following publication of any presentation, report or letter, we intend to continue transacting in the securities covered therein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation. All expressions of opinion are subject to change without notice, and Spruce Point Capital Management does not undertake to update this report or any information contained herein. Spruce Point Capital Management, subscribers and/or consultants shall have no obligation to inform any investor or viewer of this report about their historical, current, and future trading activities.

This research presentation expresses our research opinions, which we have based upon interpretation of certain facts and observations, all of which are based upon publicly available information, and all of which are set out in this research presentation. Any investment involves substantial risks, including complete loss of capital. Any forecasts or estimates are for illustrative purpose only and should not be taken as limitations of the maximum possible loss or gain. Any information contained in this report may include forward looking statements, expectations, pro forma analyses, estimates, and projections. You should assume these types of statements, expectations, pro forma analyses, estimates, and projections may turn out to be incorrect for reasons beyond Spruce Point Capital Management LLC’s control. This is not investment or accounting advice nor should it be construed as such. Use of Spruce Point Capital Management LLC’s research is at your own risk. You should do your own research and due diligence, with assistance from professional financial, legal and tax experts, before making any investment decision with respect to securities covered herein. All figures assumed to be in US Dollars, unless specified otherwise.

To the best of our ability and belief, as of the date hereof, all information contained herein is accurate and reliable and does not omit to state material facts necessary to make the statements herein not misleading, and all information has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer, or to any other person or entity that was breached by the transmission of information to Spruce Point Capital Management LLC. However, Spruce Point Capital Management LLC recognizes that there may be non-public information in the possession of RLGT or other insiders of RLGT that has not been publicly disclosed by RLGT. Therefore, such information contained herein is presented “as is,” without warranty of any kind – whether express or implied. Spruce Point Capital Management LLC makes no other representations, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use.

This report’s estimated fundamental value only represents a best efforts estimate of the potential fundamental valuation of a specific security, and is not expressed as, or implied as, assessments of the quality of a security, a summary of past performance, or an actionable investment strategy for an investor. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Spruce Point Capital Management LLC is not registered as an investment advisor, broker/dealer, or accounting firm.

All rights reserved. This document may not be reproduced or disseminated in whole or in part without the prior written consent of Spruce Point Capital Management LLC.

Disclosure:I am/we are short RLGT, ECHO.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Article by Ben Axler, Spruce Point Capital Management