“Big money is made in the stock market by being on the right side of the major moves. The idea is to get in harmony with the market. It’s suicidal to fight trends. They have a higher probability of continuing than not.”

Martin Zweig

At the beginning of each month I like to take a look at the most recent published equity market valuations. So let’s do that today. As you review the charts, keep in the back of your mind that valuation metrics are pretty much useless in identifying market peaks but they are outstanding at helping us zero in on what the forward 10-year returns are likely to be.

You’ll also see that not only are the returns highest when the market is attractively priced, there is less risk. The opposite is true when it is richly priced as is the case today. But I’m a trend guy and the trend remains strong, so let’s be happy.

I’ve shared a number of intro quotes over the last few weeks about the Fed. Do you remember Edson Gould? He was a legendary technical analyst from the 1930s through the 1970s and developed a simple rule about Federal Reserve policy that has an excellent record of foretelling a stock market decline.

The rule states that “whenever the Federal Reserve raises either the federal funds target rate, margin requirements or reserve requirements three consecutive times without a decline, the stock market is likely to suffer a substantial, perhaps serious, setback” (Schade, 2004). This simple rule is still relevant. Although it tends to lead a market top, it is something that should not be disregarded.

In the mid-1980s the great Marty Zweig wrote a book titled Winning on Wall Street. He is quoted, “Monetary conditions exert an enormous influence on stock prices. Indeed, the monetary climate – primarily the trend in interest rates and Federal Reserve policy – is the dominant factor in determining the stock market’s major direction.”

Zweig’s Fed policy rule is simple, “three steps and a stumble.” Basically, when the Fed raises interest rates three times, the stock market stumbles. When they lower rates, it’s good for stocks.

And just to hit on the Fed topic one last time, keep this from Stan Druckenmiller front of mind, “Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

Expectations are for the Fed to raise rates again in March. It will be step three. As you view the valuation charts that follow, let’s keep a close eye on trend following indicators and a close eye on the Fed.

Grab a coffee and find that favorite chair. I’ll story through each of the charts for you.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Charts of the Week: Valuations and Subsequent 10-Year Returns

- Equity Market Trend Evidence Remains Positive

- 10 Out of 13 Times, It Ended Badly – Rosenberg on Fed Hikes and Recessions

- Trade Signals – Zweig Bond Model Turns Bullish on Bonds

Charts of the Week: Valuations and Subsequent 10-Year Returns

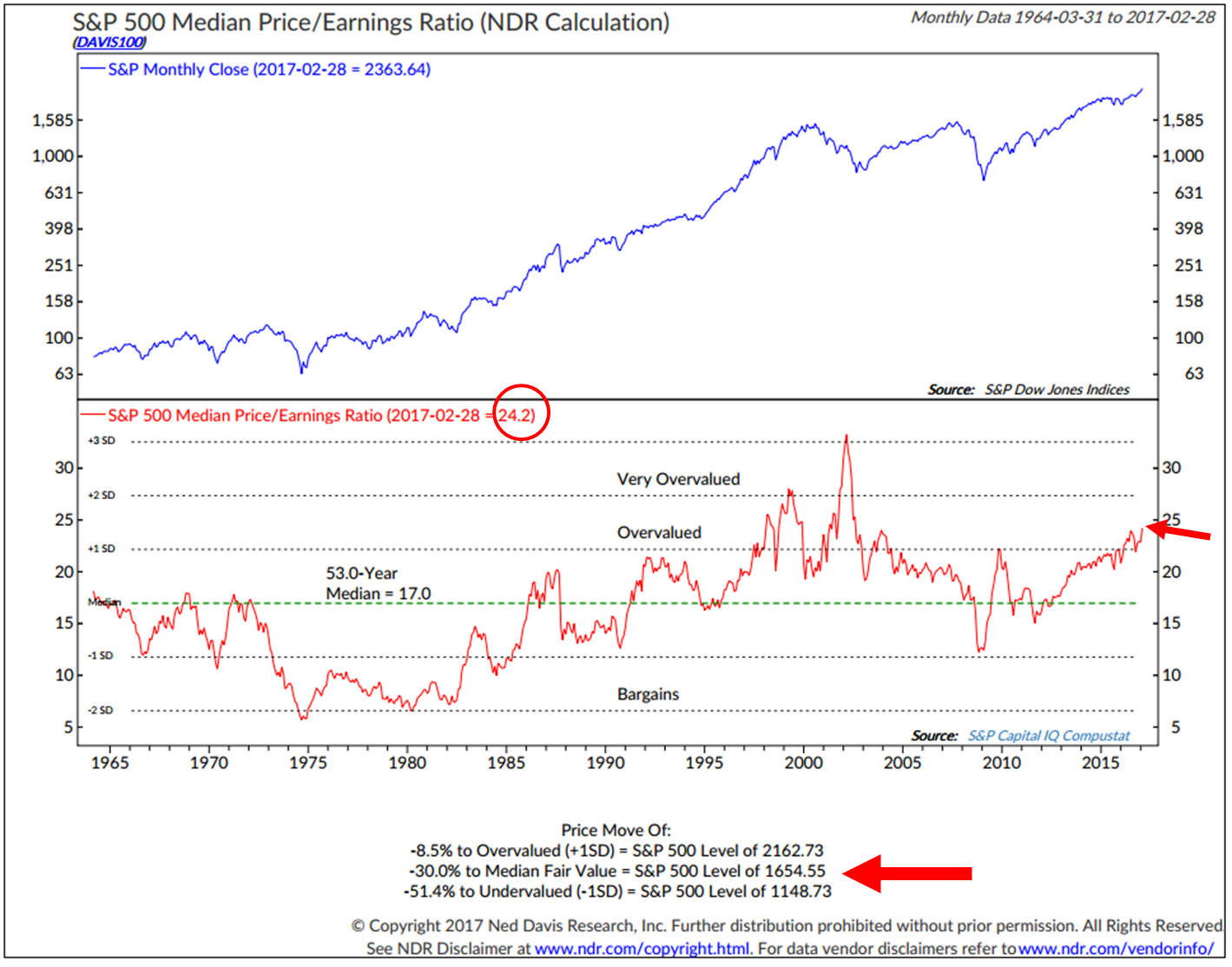

Chart 1: Median PE

Several bullet points on Median PE:

- The large red arrow points to Median Fair Value. It is based on a 53 year Median PE of 17.

- We are currently sitting 30% above that level.

- Also, the market is considered 8.5% overvalued. Overvalued and undervalued are determined by a 1 standard deviation move above and below Median Fair Value.

- Note too that the small red arrow points to the current Median PE level. It is higher than it was in 2007. The only higher period was around the Tech bubble.

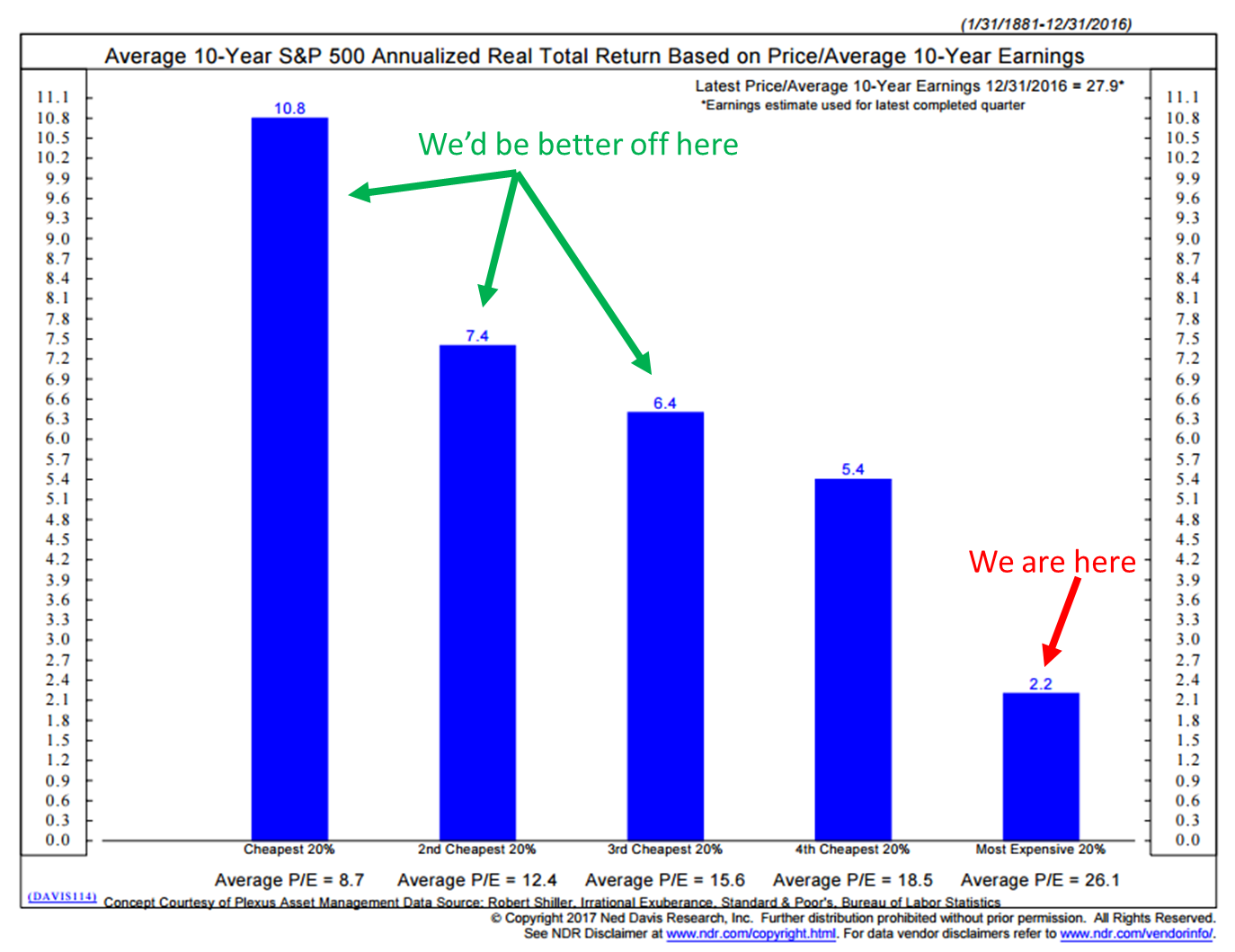

Chart 2: 10-year Forward Returns Based on Median PE

NDR sorted month-end Median PE readings into five quintiles.

- Quintile 1 Lowest 20% of all PEs (most attractively priced)

- Quintile 5 Highest 20% of all PEs (least attractively priced)

- Data period is 1926 through 2014

- Next shows the subsequent 10-year median annualized returns by quintile

In short conclusion, just like hamburgers, when you can buy them at a good price, you get a lot more for your money. When they are expensively priced, you get less for your money.

Median PE is at 24.2 at January 2017 month end. We sit solidly in quintile 5. A median annualized return of 4.3% is closer to 2.20% after inflation (assuming 2% inflation). Latest year-over-year CPI inflation is running at 2.50%. The hamburgers are very expensive.

Here is what the quintile breakdown looks like from 1981 to present, just to give you a feel.

As a quick aside, I favor Median PE because it takes a lot of accounting gimmickry out of the mix (takes out all the highs and lows). From there NDR looks at the subsequent return from each month end and sorts by quintile. Really cool work.

Chart 3: Median PE – Select Dates

To make this a little more real, I selected several dates to give you an idea as to what the Median PE was then and what the subsequent annualized 10-year return turned out to be.

- Green is low PE high return

- Red is high PE low subsequent returns

Chart 4: Median PE – Highest and lowest returns by quintile

To be fair, it is possible that a return might come in higher or lower than the median. To that end, here’s the nominal return data from 1981 to present:

- Bar chart for the subsequent 10-year annualized returns (Median returns)

- Bottom section shows the high low range. Meaning there were over 300 total month-end readings with subsequent 10-year results.

- Break that 300 down into five categories and you get 60 total occurrences.

- The highest return and lowest return out of the 60 in each quintile is posted. For example, in the best valued quintile 1, the highest return was 18.8% and the lowest return was 12.4%. A 6.4% low to high difference. I’d be happy with both or that average.

- However, note that the range begins to widen as valuations get more richly priced. I’d be happy with that 9.8% best of 60 occurrences in quintile 5 but that is a low probability.

The overall idea is that we can get a highly probable feel for what forward returns are likely to be based on valuations.

The same conclusions are found if you look at Shiller PE or most other valuation measures. Your money just can’t buy as much hamburger when it is expensively priced – not as much bang for your buck.

Chart 5: Market Valuation, Inflation and Treasury Yields: Clues from the Past by Jill Mislinski, 3/2/17

Below is some great commentary from Advisor Perspective’s Jill Mislinski. Warning – for quant geeks only. Otherwise… same conclusion. Expensive hamburgers.

“Our monthly market valuation updates have long had the same conclusion: US stock indexes are significantly overvalued, which suggests cautious expectations on investment returns. In a “normal” market environment — one with conventional business cycles, Federal Reserve policy, interest rates and inflation — current valuation levels would be a serious concern.

But these are different times. The economic cycle shaped by the Financial Crisis that began emerging in 2007 shortly after the Bear Stearns hedge funds collapsed. The Fed began its historic crusade in cutting the overnight rate from an average of 5.25% prior to the hedge fund collapse to ZIRP (Zero Interest Rate Policy) as of December 16, 2008. The bankruptcy of Lehman Brothers on September 15, 2008 was the most dramatic precipitator of the Fed’s unprecedented policies.

In the wake of the Financial Crisis, inflation has been low and the 10-year Treasury yield is about 105 basis points above its historic closing low of 1.37% in early July of 2016. So, with this refresher on the Financial Crisis in mind, let’s take another look at the popular P/E 10 valuation metric. SB here: PE 10 is the Shiller PE

Here is a scatter graph with the market valuation on the vertical axis (log scale) and inflation on the horizontal axis. It includes some key highlights: 1) the extreme overvaluation of the Tech Bubble, 2) the valuations since the start of last recession, 3) the average P/E 10 and 4) where we are today.

The inflation “sweet spot”, the range that has supported the highest valuations, is approximately between 1.4% and 3%. See, for example, the highlighted extreme valuations associated with the Tech Bubble arbitrarily as a P/E 10 of 30 and higher. The chronology of the orange “bubble” on the chart is a clockwise loop of 56 months starting at the 6 o’clock position.

The P/E 10 was 31.3 and the annual inflation rate for that month, June 1997, was 2.30%. The average inflation rate for the loop was 2.41%. The P/E 10 peak of 44.2 in December 1999 was accompanied by a 2.68% annual inflation rate. Two months later the inflation rate topped 3% at 3.22%. The right side of the loop shows what happened thereafter. The ratio slipped below 30 for two months (the tail at the bottom of the loop) before its final three-month swan song in the 30+ range.

The latest P/E 10 valuation is 29.2 at a 2.42% year-over-year inflation rate, which is right in the sweet spot mentioned above.

And speaking of that 30 threshold for the P/E 10, prior to the Tech Bubble, only two months in history had a ratio above 30: They were 31.5 and 32.6 in August and September of 1929, just before the Crash of 1929. Research estimates put the annual inflation rate during those two months at 1.17% and 0.00% (zero).

SB here: Jill also takes a look at valuations relative to the 10-year Treasury yield. You can go here for the full piece. I’m going to jump to her conclusion:

In the months following the Great Financial Crisis, we have essentially been in “uncharted” territory. Never in history have we had 20+ P/E 10 ratios with yields below 2.5%. The latest monthly average of daily closes on the 10-year yield is at 2.42%, which is above its all-time monthly average low of 1.50% in July 2016. The closest we ever came to this in U.S. history was a seven-month period from October 1936 to April 1937. During that timeframe, the 10-year yield averaged 2.67%. How did the market fare? The S&P Composite hit an interim high (based on monthly averages of daily closes) in February 1937. The index plunged 44.9% over the next 15 months.

If we look to the Dow daily closes during that period, the index hit an interim high on March 3, 1937 and fell 49.1% to an interim trough on March 31, 1938 — 13 months later.

What can we conclude? We have been in “uncharted” territory. Despite the end of QE, many analysts assume that Fed intervention through its Zero Interest Rate Policy (ZIRP), will keep yields in the basement for a prolonged period, thus continuing to promote a risk-on skew to investment strategies despite weak fundamentals.

On the other hand, we could see a negative market reaction to a growing sense that Fed intervention may have its downside, resulting in an aberrant bond market and increased inflation/deflation risk.”

We are indeed living in interesting times.

Chart 6: Shiller PE and Subsequent 10-Year Returns

Ok – you get the point. Let’s next focus back on the concept of trend. I believe it can help us better navigate the challenging periods that I see coming ahead.

_______________________________________________________________________________________________________

Equity Market Trend Evidence Remains Positive

Every Wednesday I post Trade Signals on the CMG website and each Friday I link you to it in OMR. Here is the link to the TS webpage.

I personally believe that much of what we need to know is found in the price trend of a security. It is the point where buyers meet sellers. More buyers than sellers pushes prices higher. Zweig’s famous “the trend is your friend.”

My go to equity market trend following chart is something we co-created with Ned Davis Research. I have been a happy subscriber since the mid-1990s and loved (and still do) Ned’s “Big Mo” (for momentum) chart. However, I wanted something that I believed was more tradable and we put our collective quant geek hats on and co-created the CMG NDR Large Cap Momentum Index.

Our process is different than Big Mo and scales out of the market as the weight of evidence weakens. S&P Dow Jones calculates the index and you can follow it here. The index is up 18.66% over the trailing 12 months. This is something you can follow yourself each week in Trade Signals.

Here’s the chart. Currently signaling 100% invested in U.S. Large Caps. A couple of things to note:

- First, this is hypothetical index history. Before any costs.

- The bottom section shows the return stats from early 1992 to present.

- About a 33% pickup in return over the period and a max drawdown (decline experienced) of 19.7% vs 55.3% for the buy-and-hold investor.

- S equals sell signals, B buy signals

- Top blue line is the gain of $100 for the CMG NDR Index (before costs) vs. the red line which is the gain of $100 for the buy-and-hold S&P 500 Index (before costs).

- The chart will make your eyes cross so I recommend reading the how it works (link just below chart)

Click here to go to Trade Signals. Page down until you see the chart and the “Here is how it works” explanation that follows.

Further, the next chart is a snapshot from last Wednesday’s post. I look at a number of indicators and post them each week.

___________________________________________________________________________________________________________

10 Out of 13 Times, It Ended Badly – Rosenberg on Fed Hikes and Recessions

Let’s hit this Fed topic just one more time.

David Rosenberg at Gluskin Sheff wrote Thursday that, “Monetary policy is profoundly more important to the markets and the economy than is the case with fiscal policy, though all the Fed is doing now is removing accommodation.”

Rosenberg added that, “there have been 13 Fed rate hike cycles in the post-WWII era and 10 landed the economy in recession. Soft landings are rare and when they have occurred, they have come in the third year of the expansion, not the eighth.” (emphasis mine)

_________________________________________________________________

Trade Signals – Zweig Bond Model Turns Bullish on Bonds

“The trend is your friend.” – Martin Zweig

Personally, over the years I’ve certainly had my set of fundamental convictions. I continue to listen to an inner voice of logic but it is “trend following” that I adhere to as I find the results more statistically significant.

My fundamental view may say one thing (like my current expectations for rising inflation pressures and that a sovereign debt default crisis in Europe will drive interest rates higher), while trend evidence is telling me something else.

Here’s an example: Twenty-five out of twenty-five Wall Street analysts believed rates would rise from 2.75% to an average of 3.25% in 2015. I, too, felt rates would rise. Rates on the 10-year Treasury fell to 2.25% by the end of 2015 on the way to a low of 1.37% on July 13, 2016. The Zweig Bond Model stayed in long bonds. The trend was for lower yields and higher bond prices.

You may be more of a fundamental person and that really works well for some. I’ve just seen too few traders over the years that have process, trading ability and conviction. Stan Druckenmiller is the man. He zeroes in on his high conviction trades and goes big. In believe he is the greatest stock speculator of our time. Few can do what he can do.

As you can see in the Zweig Bond Model chart above, the numbers are pretty good. $1,000 invested turned into $81,861 vs. $27,131 for the buy-and-hold investor in the Barclay’s Aggregate Bond TR Index. Risk management matters and after a 35 year bond bull market and rates near 5000 year lows, risk management matters more today than ever. But not all trades win. It takes conviction to stick to this or any process.

So despite my current view that rates will move higher, they might just move to 2% (currently at 2.50%) before they move to 3%. Or maybe they move to 1% as my friend Lacy Hunt believes. I like following a trend process and the Zweig process is a pretty good one.

Click here for the charts and explanations.

Personal Note – Anything Goes

I’m so excited for tonight. Susan, I and our boys are watching our 17 year-old Kyle take lead in his high school musical Anything Goes. His big goals involve acting and if it truly takes 10,000 hours, he sure has the passion and drive to do the work.

The story concerns madcap antics aboard an ocean liner bound from New York to London. Billy Crocker is a stowaway in love with heiress Hope Harcourt, who is engaged to Lord Evelyn Oakleigh. Reno Sweeney, a nightclub singer, and Public Enemy #13 Moonface Martin aid Billy in his quest to win Hope. You may remember some of the songs; “Anything Goes“, “You’re the Top” and “I Get a Kick Out of You.”

Believe it or not, he is tap dancing. You can imagine the teasing at the dinner table to which Kyle holds strong. Last night was the preview and he sure sounds confident. We can’t wait!

Kyle at last night’s preview show

I am presenting ideas on how to allocate at a March 14 and 15 event in Summit, Red Bank and Hackensack, New Jersey on behalf of Josh Jalinski, “The Financial Quarterback.” Josh is a popular financial radio talk show host on iHeart Radio.

Given where we are in the business cycle, I’ll be presenting on valuations and forward returns and will share some ideas on how to invest in the period ahead. John Mauldin will be sharing his views on what he sees ahead. If you have never seen John Mauldin present, you should. He has a gifted way of explaining complex macroeconomic topics in a way many people can better understand.

As a side, if you not reading John’s weekly Thoughts From the Frontlines, I recommend you do. You can follow him here.

If you’re an individual investor and are interested in attending, email [email protected] to reserve a seat. Let Josh’s team know I sent you to him and please feel free to email me if you’d like to learn more.

Texas Chili Dinner – March 28 at Mauldin’s home in Dallas:

If you are an independent advisor and you’d like to learn more about the Mauldin Solutions Core Strategy, John and his team will be hosting a series of due diligence meetings in Dallas. The first is scheduled for March 28 and 29 in Dallas. Dinner at John’s house the evening of the 28th and a half-day due diligence session with the ETF trading strategists that make up the Mauldin Solutions Core Strategy the morning of the 29th. Send me an email if you’d like to learn more.

John believes that it is important to diversify trading strategies. He launched a new portfolio management company called Mauldin Solutions and put together an investment strategy that is designed to be a “core” holding within an investment portfolio.

One of his goals is to be able to help brokers and advisers get their clients through the storms that as he says, “we all know are coming as the world struggles to figure out how to deal with the massive amounts of debt and government obligations that are building up.” He believes and it may not be this year, but at some point there has to be a great debt reset, and you’ll need to be able to get your clients through it.

John sought out to combine a handful of ETF trading strategists that have a global mandate. Four ETF strategists were selected and John is delivering the combined strategies in one portfolio. We are pleased to be one of the four ETF strategists he selected.

If you are interested in attending to learn more about what we’re doing, drop a note to me at [email protected] or John’s team at [email protected]. Give us your name and what firm you are with. We’ll get back to you ASAP.

Wishing you an outstanding weekend! Anything Goes – really excited… All the very best to you and your family.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

{kind=link}