So here we are, 11 days before America picks its poison, with most national polls showing a win for Hillary Clinton. If she pulls it off, she’ll become not only the first woman and first first lady to rise to the country’s highest office but also the first Democrat to succeed another two-term Democrat since Martin Van Buren succeeded Andrew Jackson in 1837.

She’ll also become the first to be under FBI investigation. Today we learned that the bureau is reopening her email case, mere days after WikiLeaks released even more damning files on the nominee. I find it interesting that back in July, eccentric internet entrepreneur Kim Dotcom predicted that WikiLeaks founder Julian Assange would turn out to be Hillary’s “worst nightmare”—a prediction that has largely come true.

Meanwhile, if Donald Trump manages an upset, he will become the oldest person ever to take the oath of office and the first to transition directly from the business world to the presidency without any past experience as a high-ranking government official (like William Howard Taft and Herbert Hoover) or military officer (like Zachary Taylor, Ulysses S. Grant and Dwight D. Eisenhower).

To Trump’s supporters and many others, of course, this is one of his main assets.

But back to the polls. In the end, they can often be misleading. I can point to several previous polls that said one thing but in the end turned out to be inaccurate, starting with those that suggested Brexit wouldn’t happen. As you know, they were way off.

In a now-classic example, California polls gave L.A. mayor Tom Bradley a wide lead in the days leading up to the 1982 gubernatorial election, and yet he was roundly defeated. Known today as the “Bradley effect,” the accepted theory is that voters told pollsters they supported Bradley, an African-American, so as not to appear racist. But in the privacy of the voting booth, those same voters pulled the lever for his opponent.

Many now wonder if a reverse Bradley effect could be taking shape in the current presidential election, with voters not wanting to admit their support for Trump—the least-liked person ever to run in U.S. history, followed closely by Hillary—but casting their ballot for him anyway.

Will this Election Buck the Trend?

I’ve written before about the presidential election cycle theory, developed several decades ago by Yale Hirsch, whose son Jeffrey serves as editor of the indispensable Stock Trader’s Almanac, now in its 50th edition. But because this year’s election breaks the mold in a number of important ways, it raises the question of how closely it will hew to past elections, at least where market reaction is concerned.

One of the most significant factors to keep in mind this year is that no incumbent’s name appears on the ballot. This is rarer than you might initially think. Since 1947, when the number of terms was limited to two, only five people have been elected twice and completed two full terms.

This two-term presidential cycle can often have a measurable effect on markets, as I wrote about in-depth in “Managing Expectations.” A president who’s up for reelection has a huge incentive to enact policies that support the economy and labor market, which investors like.

|

By the end of his second term, however, markets are faced with the reality that someone new will be occupying the Oval Office soon, complete with a new cabinet, new agenda, new governing style and new policies. This uncertainty has historically given investors the jitters—even when they’re in favor of the incoming president. (Even the most ardent Trump supporter must admit he’s more volatile and higher-risk than Hillary, who would likely maintain the status quo. But like a high-risk stock, Trump could also potentially deliver much higher returns.)

In second-term election years, then, equities dipped an average 4 percent, compared to an average increase of 7 percent during all election years.

Will we see a repeat of this in 2016? There’s no way to say for sure. But as of October 27, stocks are up more than 6 percent year-to-date. Although slightly below the average, this is much higher than returns in the last two election cycles when a new president had to be selected: In 2008, the market plunged nearly 40 percent; in 2000, it ended down 9 percent.

Looking Past November 8

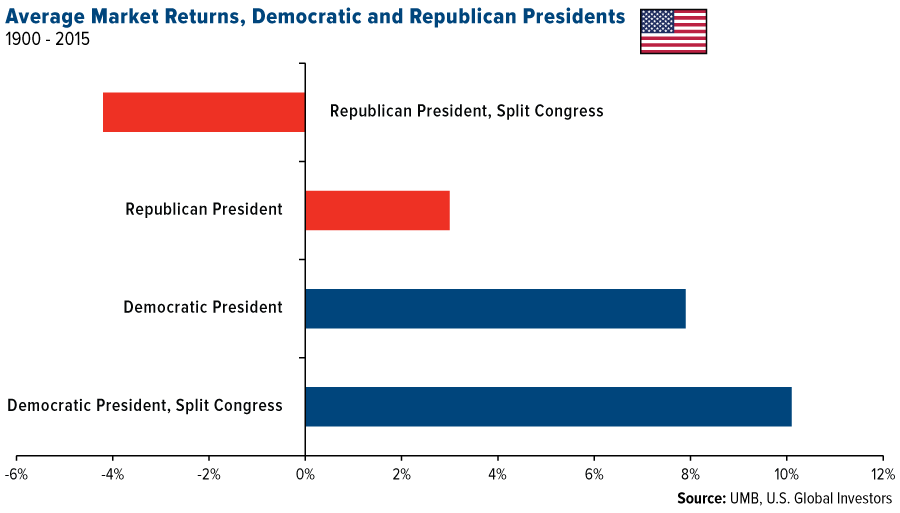

Again, it’s the policies that matter, not necessarily the party. However, there is evidence that stocks have performed slightly better when a Democrat is president, especially when Congress is split, as it was during most of Barack Obama’s administration.

Members of both parties might not like hearing this, but it’s what data mining has uncovered.

By-and-large, though, markets seem to be agnostic as to which party is in control of the White House. So many other factors exert just as much, if not more, influence over market performance, including monetary policy, inflation/deflation and whether the country is at war or peace.

Whichever way you swing, though, it’s becoming more compelling to have some of your portfolio in tax-free municipal bonds, which in the past have provided a certain level of stability in times of uncertainty.

Could Venezuela Become the Next Syria?

Speaking of poor policymaking, hyperinflation and violence—Venezuela is sliding closer and closer to the brink of collapse, with some sobering consequences.

This was among the topics of conversation this week at the Mining & Investment Latin America Summit in Lima, Peru. While there, I had dinner with a couple of Canadian lawyers who represented a few Latin American oil producers, some of them based in Venezuela.

Things have gone from bad to worse, they informed me. Since 2013, when Nicolás Maduro took power after the death of Hugo Chávez, the socialist country has struggled with skyrocketing inflation, food and medicine shortages, a shrinking economy and rising violence and corruption. (Its capital city of Caracas recently overtook San Pedro Sula, Honduras, for having the world’s highest homicide rate.)

These have only intensified since oil prices fell by half more than two years ago, as oil accounts for 95 percent of Venezuela’s export earnings.

Now, President Maduro has effectively suspended a scheduled recall referendum, backed by the opposition-controlled National Assembly, despite as many as 80 percent of Venezuelans in favor of his removal from office. The suspension has led to widespread protests in the streets, with accusations of a coup being tossed around on both sides.

|

The fear, the lawyers said, is that if Caracas falls, the vacuum it leaves behind would serve as a prime terrorist base of operations—a Latin American Syria, as it were, complete with the world’s largest proven oil reserves to finance it.

We’ve already seen the country cozy up to fellow OPEC member Iran, recognized by the State Department as the world’s leading state sponsor of global terrorism. According to the Gatestone Institute, a New York-based international policy think-tank, Iran is “partnering with Venezuela’s drug traders and creating a foothold” in the Latin American country.

It’s such a travesty that a nation as resource-rich as Venezuela could allow itself to rot from within. Its descent into chaos should serve as just the latest cautionary tale to other countries that are willing to risk stability and prosperity for even more socialism.