Household Equity Ownership The Best Contrarian Indicator?

July 8, 2016

By Steve Blumenthal

Bonds are what they are. Today, they are less than what they are. It is said—nothing is ever new under the sun of finance… but we do live in a unique time in two critical ways—interest rates and monetary moment.

A few years ago, a book appeared called A History of Interest Rates… The book is a chronicle of 5,000 years of interest rates… Not a single line about negative yields. From Hamrabi to Ben S. Bernanke, negative yields were nonexistent. Today, they are here in plethora.

Two-thirds of those are Japanese. A trillion of French and a trillion of German. Every single Swiss, now yields less than zero. And yet, people seem to want them more for that.

A Fitch (the rating agency) press release characterized the demand for these assets as the demand for ‘safe’ assets. For all the world, the bond market seems to have the notion that sovereign debt is intrinsically and indisputably safe.

I was born a few months after yield made their lows in April of 1946… Today, people seem to feel negative yielding securities are inherently safe because interest rates always go down. Curiously enough, the bond bear market beginning in 1946…

The ECB has been buying sovereign debt including Italian debt hand over fist. These distortions inform every single corner of our capital markets.

These prices are under the thumb of government… We live in a central banks constructed hall of mirrors.

From Jim Grant’s keynote address at NYSSA Conference. Jim is the author of Grant’s Interest Rate Observer.

Jim goes on to recommend gold. He said, “The case for gold is not that it’s a hedge against monetary disorder, but that it’s an investment in monetary disorder, the dynamic we’ve seen play out since 2008. Radical monetary policy begets more radical monetary policy…”

We are living in an unprecedented interest rate and monetary policy period in time. As for gold, it moved into a cyclical bull market environment in January and the trend remains bullish. (Please visit my Trade Signals post and scroll down to the gold chart). I like gold for up to 10% of a total portfolio structure.

Today let’s take a look at what the most recent equity market valuation data is telling us. We’ll look at one-to-three year, seven-year and 10-year forward time horizons.

You’ll find that U.S. equities are significantly overvalued. This continues to suggest caution and setting realistic expectations on stock market returns.

Being the quant junkie that I am, I’ve found a couple of really cool charts I believe you’ll find interesting. Do you follow Value Line? One of the charts looks at Value Line’s price targets for individual equities. Another looks at equity ownership as a percentage of total household net worth and it has an amazingly accurate record of telling us what the 10-year forward returns may likely be.

I hope you enjoy today’s piece. Grab that coffee. There are a lot of charts but the read is quick.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- What Valuations Tell Us About Future Equity Market Returns

- What’s Been Driving Stocks Higher? Aggregate Cash Spent on Acquisitions

- Trade Signals – A Great First Half for Long Duration Bonds and High Yield

- Concluding Thoughts and a Few Ideas

What Valuations Tell Us about Future Equity Market Returns

Let’s do a quick run-through of various valuation measures and then look at probable forward returns:

- Average of Four Popular Valuation Measures

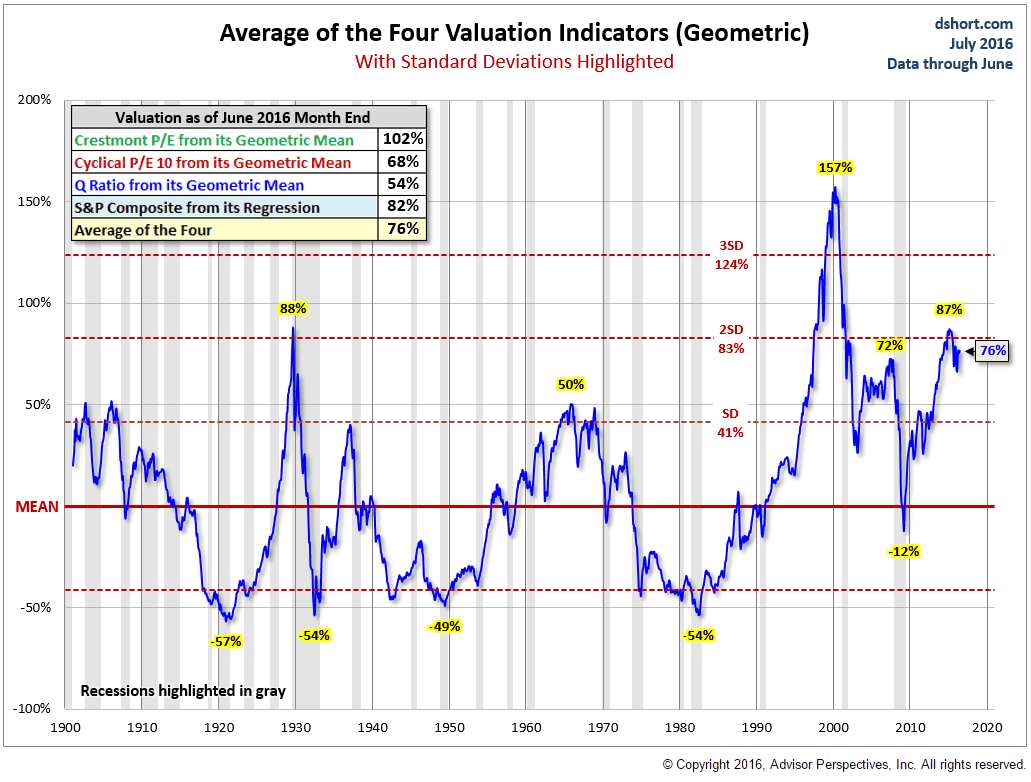

Note in this chart (source) that the average of four valuation indicators (Crestmont P/E, Shiller Cyclical P/E, Q Ratio and S&P Composite) is 76% above the mean as noted by the solid red line (the mean is the average of the four valuation measures dating back to 1900). Markets tend to move above and below the mean (solid blue line).

Note too that the most overvalued level was at 157% above the mean at the market peak in early 2000. It recently peaked at 87% and is currently at 76%. There were only two prior periods when valuations were higher – 1929 and 2000.

Here is a summary of the four market valuation indicators we update on a monthly basis.

- The Crestmont Research P/E Ratio (more)

- The Cyclical P/E ratio using the trailing 10-year earnings as the divisor (more)

- The Q Ratio, which is the total price of the market divided by its replacement cost (more)

- The relationship of the S&P Composite price to a regression trendline (more)

- Median P/E (Ned Davis Research (NDR) calculation) – 22.9 as of June 30, 2016

Median P/E for the S&P 500 Index is the point in which 250 of the 500 stocks’ P/E ratios are higher and 250 of the stocks’ P/E ratios are lower. I like it because it takes out a lot of one-time accounting gimmicks and sets a reasonable level to compare it versus the month-end median P/E going back in time.

The June 2016 reading of 22.9 puts us in quintile 5 (most expensive). If we break each month-end median P/E going back to 1926 through December 2014 into five separate quintiles (1 being the lowest P/E and 5 the highest) and then look at what the actual subsequent 10-year annualized returns turned out to be, we can compare where we are today and get a sense of a probable future outcome.

To help you get a sense for what is historically inexpensive and what might be considered expensive, following a breakdown of the median P/E ranges 1981 through December 2015 (quintiles 1 through 5):

The 52.3 year Median P/E is 16.9. I believe that identifies a point at which U.S. large-cap stocks are fairly priced. My plan is to switch from 30% equity (hedged) exposure to 50% when we get to quintile 3.

Based on today’s earnings, median fair value in the S&P 500 Index is at approximately 1550. The S&P 500 is near 2100 today. This means the market will need to decline 26% to get to a point in which it is fairly valued.

U.S. stocks are significantly overvalued. We should be cautious with our expectations regarding future returns.

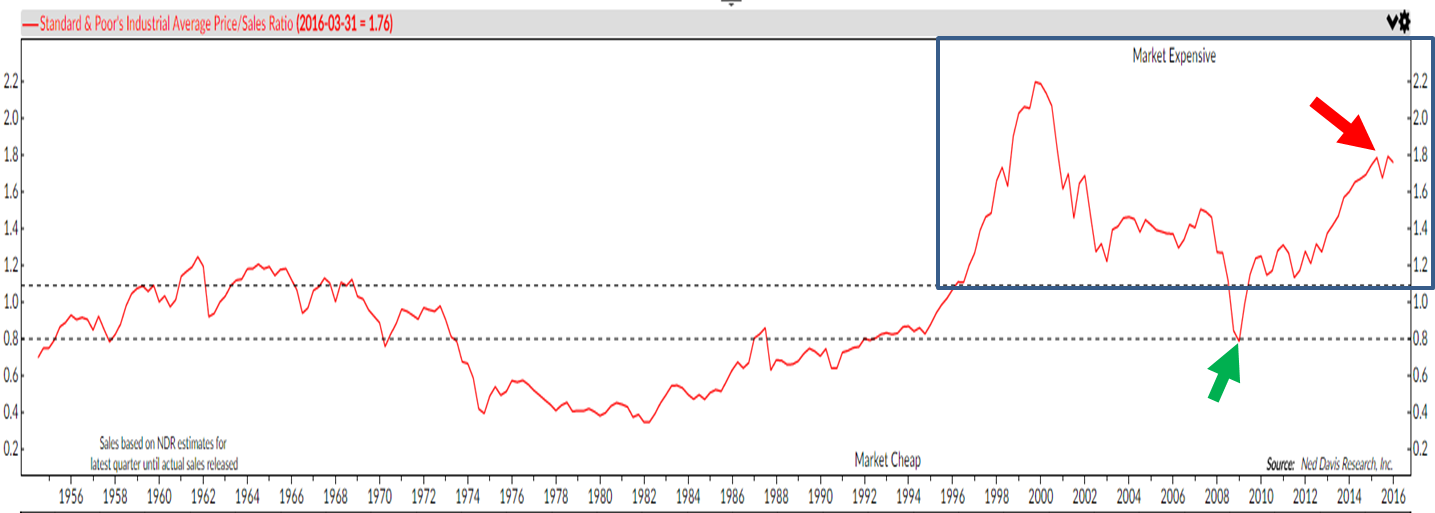

- Price-to-Sales

The blue rectangle shows the level at which prices are high relative to sales.

The next chart show what the returns for the S&P Industrial Average looks like (data 1954 through March 2016) when the price of the market was high:

The conclusion here is to expect 3.66% gains per annum.

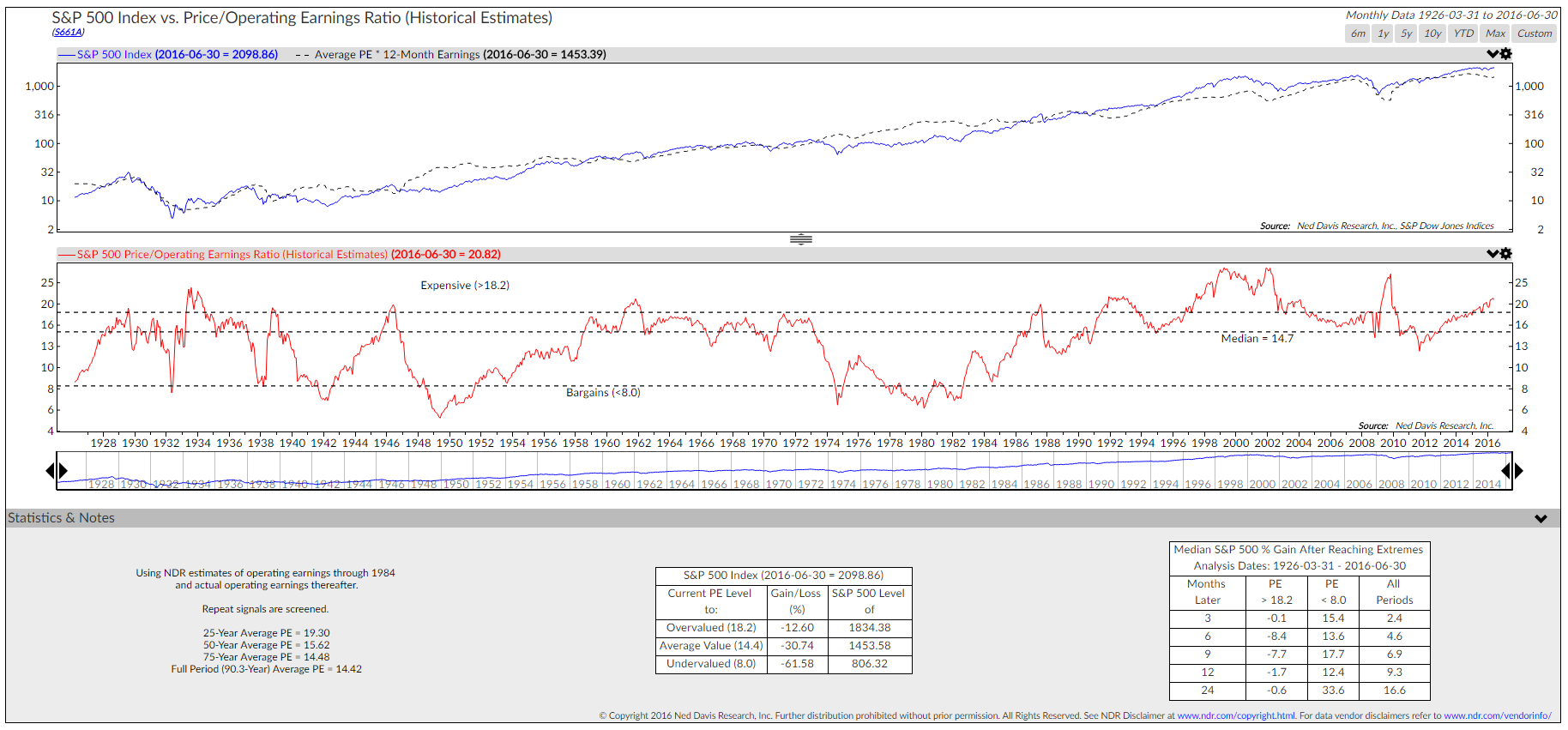

- Price-to-Operating Earnings

You’ll see in the middle section of the chart that prices are expensive relative to operating earnings. The current reading is 20.82. Based on that figure, take a look at the bottom right hand corner of the chart and see what the returns were when the number is greater than 18.2. Also, take a look at the data in the bottom middle section and bottom left hand section of the chart.

- Buffett’s Favorite Valuation Indicator – Stock Market Cap as a Percentage of Nominal GDP (Look and get dizzy or jump to the conclusion – here too: “Very Overvalued”)

Below charts a select number of times to give you a feel of what 10 year annualized returns historically when you have various starting median P/E.

And what does median P/E tell us about risk? Quintile 5’s are riskiest (next chart).

What Household Equity Ownership Tells Us About Coming 10-Year Equity Market Returns:

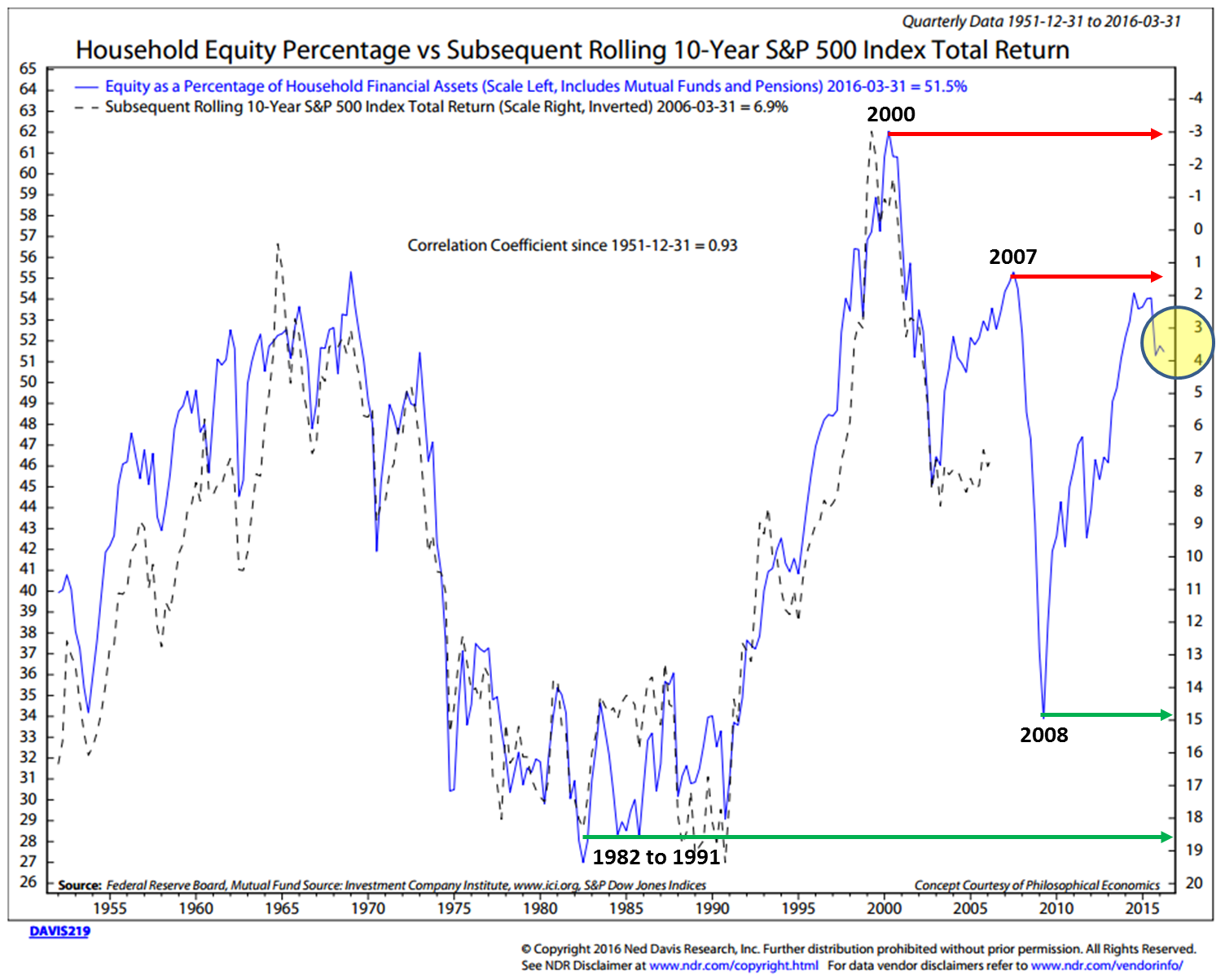

Put this next chart in the “really cool” category. It takes a look the percentage households have invested in equities. Think about it in these terms: when investors already have a high percentage of their assets in stocks, there is less money available to buy more and less potential buying demand. The reverse is true when they are underinvested in stocks.

The solid blue line tracks the percentage of household money in equities (those percentages are reflected on the left hand side of the chart). The dotted line plots what the subsequent rolling 10-year return for the S&P 500 index turned out to be. The dotted line ends at the last 10-year number (April 2006 through March 2016).

I’ve noted several prior periods. The dates and arrows are my mark-up on NDR’s chart. When percentage in equities was high, such as in 2000 and 2007 (red arrows), subsequent returns were low. And what a buy it was in the 1980’s and 2009 (green arrows).

Note the very high correlation coefficient of 0.93. 1.0 is perfect correlation. In short, this process has done a great job at predicting what annualized total returns for the S&P 500 Index are likely to be over the coming 10 years. See highlighted yellow circle.

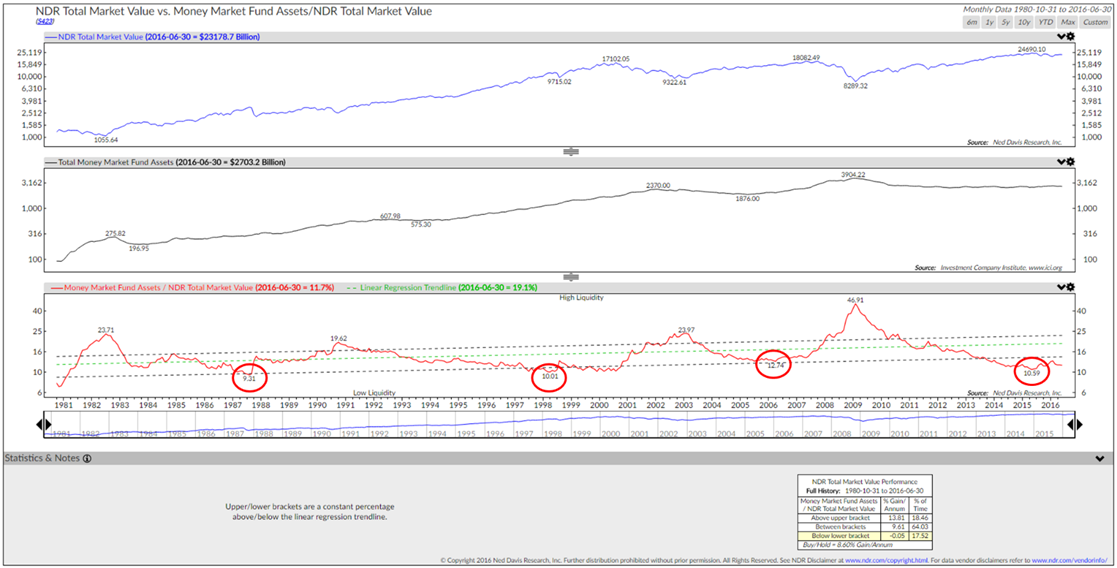

Not only is household equity percentage ownership high, but the amount of money in money market funds (think of it as potential buying power to fuel prices higher) is low (red circles):

Note the high levels of money market assets in 2002/3 and 2009. That was fear driving investors out of stocks. That is when we want to be a buyer (when everyone else is selling).

Value Line – What Value Line Research is Saying About Forward 3-5 Year Equity Returns:

Value Line reports stock appreciation potential on thousands of individual stocks. NDR took the estimate of the median price appreciation potential by first calculating the percentage change between the current price of each stock in the Value Line universe and the middle of its 3 to 5 year Target Price Range as determined by Value Line analysts. The figures are then arrayed, and the median price appreciation potential is determined. This is what they found (data 1980 to July 1, 2016):

Since May 23, 1980, the indicator has been as low as 26 and as high as 222. The lower the number, the lower the expected appreciation potential. Here is the one-year, two-year and three-year return data when the indicator reading was “Above 110” and “Below 70” (the current reading is 50):

The data reflects cumulative (not annualized) returns over the periods presented. In sum, expect low one- to three-year equity market returns.

Finally, here is the latest from Jeremy Grantham and team at GMO. Note that the forward seven-year annualized return estimate for large-cap stocks is lower than it was in December 1999.

OK – enough said. Hedge that equity exposure so that you can be in a position to get more aggressive when the getting gets good again.

What’s Been Driving Stocks Higher? Aggregate Cash Spent on Acquisitions

If you have been wondering what’s been fueling the market’s advance, take a look at the amount of cash spent (yellow circle) versus the amount spent in 2007 and the late 1990’s.

Source: S&P Capital IQ Compustat and NDR

Trade Signals – A Great First Half for Long Duration Bonds and High Yield

Click through to find the most recent trade signals. My favorite weight of evidence indicator, The CMG NDR Large Cap Momentum Index, remains in a sell signal. Trades Signals is posted each Wednesday. Here is a link to the Trade Signals blog page.

Concluding Thoughts and a Few Ideas

In the short term, here’s the bet we are facing:

- The Fed and global central bankers (the monetary policymakers that raise and lower rates, print money and buy stocks and bonds) are able to partner with thefiscal authorities (politicians that write laws and are capable of legislating grand infrastructure projects, education reform, entitlement reform, tax reform, debt reform/amnesty, etc.) and create a potential soft landing.

- The politicians here and in Japan, China, and the E.U. are unable to get their acts together. This has to happen globally. To date, the fiscal side of the equation has been non-existent.

Which is more probable? I’m solidly in the #2 camp. I believe it will likely take a crisis to wake the fiscal authorities up. I hope I’m wrong.

Which brings me back to valuations and the title of this piece, “The Only Game in Town.” It is about a rush to safety. Remember the Cyprus banking crisis and the investor “bail-ins” that followed. Think about this potential in Italy, Portugal and France. Big money will flee risk, high regulation and high taxation. This is a mess, folks, and I don’t think the politicians are keen on making their governments small or cutting their own benefits.

What if Brexit is the tip of the iceberg? What if an Italian, Portuguese or French sovereign debt crisis causes money to flee? The Italian banks are screwed and individual investors own much of that debt. The destination will likely be U.S. equities and U.S. fixed income. I think this is likely to happen.

I remember back in 2007, I was wondering who kept buying all of those mortgage bonds. Synthetically packaged and sliced and diced into created securities; then resold again and again to, as it turned out, some unsuspecting German institutional investors. High yield too kept rising. It lasted until it didn’t.

We may see an influx of capital into the U.S. like we did in the late 1920’s. Money will flow to where it is perceived to be treated best. It is a relative thing. So add that to the bet. We may just race even higher in U.S. high-yield bonds, U.S. equities, and U.S. corporate and government bonds, like in the 1920’s and 2007. More buyers than sellers will drive prices higher. It could happen, but it will be short lived. So how do you size your portfolios? Can we take that bet? I think valuations and probable forward returns should stay front of mind.

If we break valuations down into five categories (1-5 with 1 being least expensive and 5 most expensive), and we found ourselves with stocks that were reasonable/attractively priced (categories 1, 2 and 3), I’d say it’s going to be bumpy but our 10-year forward returns still look pretty good. The problem is we find ourselves in category 5 with a 10-year forward return outlook, before inflation, of approximately 2% to 4%.

Show the valuation and probable return charts to your clients. This doesn’t mean that one can’t generate return. It just means we have to find more flexible and unconstrained and risk-managed ways to get from here to there. “There” being the point when forward equity returns are in the 10% to 15% range. “There” being the point when risk of loss is far less.

And between here and there is another recession. And it is the cleansing of recession that will create the next opportunity. Risk is high. We’ve got to get across the bridge with capital largely intact.

What You Can Do

I recommend an overweight to tactical and liquid alternatives. Hedge that equity exposure and be tactical with fixed income. That 1.38% 10-year Treasury is not going to help the 60/40 mix like it has done in years past. I like following the Zweig model to guide me with short-term or long-term high quality bond exposure. Be tactical and remain flexible.

Add a global tactical all asset strategy into your portfolio. Mix a few managers that have sound processes and a seasoned team. There are several managed futures funds that performed well during the several days of Brexit meltdown. You don’t want to invest in them because of that, but you do want to invest in managers that are unconstrained in how they can drive returns. Non-correlating strategies add to your portfolios diversification and help to reduce overall portfolio risk.

Next week we’ll take a look at a few of my favorite recession prediction data. Nothing in this business is perfect but there are a few processes with high win rates. Since recessions are only known after the fact and since equity markets decline 30% to 60% during recessions, we must get defensive before or near the time that they begin.

5,000 years and never a negative interest rate! Interesting times for you and me, my good friend.

Personal Note

I’m flying to Chicago next Wednesday for a large advisor conference. Avi and Jason are attending as well. I present on Friday. We are looking forward to catching up with some good friends.

The boys and I are headed to the Philadelphia Union’s home game on Saturday. Beer and peanuts are in dad’s immediate future and Chickie’s and Pete’s chicken fingers and crab fries, along with Wawa ice cream, await the boys. Our MLS soccer team is doing well this year. It’s been tough to be a Philadelphia sports fan for way too many years. Our fingers remain crossed.

Wishing you and your family a wonderful weekend!

If you find the “On My Radar” weekly research letter helpful, please tell a friend … they can sign up for the letter by clicking the “subscribe here” link that follows:

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.