What You Will Learn:

- How analyzing R&D can reveal a moat

- What insight you gain from Gross Profitability to Assets

- The intrinsic value range of Gilead Sciences

(note: this article was originally written on Oct 1)

One of the things I'm not good at is acting like I know everything.

That's the position I'm taking today with Gilead Sciences (GILD). When I write articles, my goal is not to cover and write about every granular detail. There are other articles that provide those details.

Am I an expert in Gilead Sciences?

No.

But do I know my numbers, understand the financial statement analysis and know how to interpret it? Yes, yes and yes.

And due to requests from my previous article on my case for Apple based on the numbers, I'll take a similar approach with Gilead Sciences.

When I look at a company, I try not to use a cookie-cutter method. With Apple, I focused on FCF and its valuation to FCF and multiples.

However, Gilead Sciences is obviously different.

Simplifying the important qualitative aspects of Gilead, it's a biopharma company that focuses on:

- Great research and development;

- specific niche markets instead of spreading itself too thin;

- dominating its market; and

- expanding margins.

2014 is a prime example of what I'm seeing with the way Gilead Sciences operates. Its dominant position in the HCV market in such a short time deserves praise. Sure the Sovaldi pills are extremely expensive at about $1,000 a pill. However, when you look at the full context of low side effects and complete heal rate, it's a different story.

Quality drugs that work obviously cost more upfront compared to cheaper alternatives that “seem” cheaper but cost more over the full duration of the treatment. It's no wonder that revenues grew 122% in 2014. Such growth isn't sustainable. The initial launch was a huge success with many patients having waited for the drug, adding to the spike in revenues in 2014.

It's why analyst and growth predictions are at 0% for next year. Keep in mind that analyst and expected growth predictions are all very short term.

Here's what Ben Graham, the father of value investing, said about short-term growth and expectations:

In the short run, the market is a voting machine but in the long run, it is a weighing machine.

R&D Shows Why Gilead Has A Strong Moat

R&D spending is the heart and soul for companies in the pharma and biotech sector. Strong companies are able to maintain fairly consistent numbers on their spending. They don't have to overspend to catch up with competitors and they aren't spending too little to allow competitors to catch up.

The easiest example I use is Intel and AMD. Intel for the most part has R&D expenses in the mid teens (recently increased to 20% range) while AMD was up in the 30% range until 2009 and has cut it down to 20%. On an absolute basis, Intel has increased the amount while AMD has cut the dollar value.

Here's how Gilead Sciences is spending on R&D. On a percentage basis, it's lower than average, but from an absolute basis, R&D spending increased 34.6% in 2014 compared to 2013. A good sign because the company is making money faster than it can use it.

GILD Annual R&D Margin Reveals Future Growth | Enlarge

However, the TTM R&D spending looks low, but when you dig in by checking the quarterly numbers, the signs are positive.

GILD Quarterly R&D Expense | Enlarge

GILD Quarterly R&D Expense | Enlarge

By comparing the same periods, current Q2 R&D spending is ahead of last year's Q2 spending.

Management CROIC Adds To Moat Strength

Another method I use to verify competitive advantage is by looking at the managements' performance based on the cash they return on invested capital (CROIC).

Invested Capital = Shareholders' Equity + Interest-Bearing Debt + Short-Term Debt + Long-Term Debt

It looks at how much free cash flow is generated for every dollar of invested capital. The higher the better. On average, companies that can maintain CROIC above 15% are considered to have strong competitive advantages.

Strong CROIC at GILD | Enlarge

Strong CROIC at GILD | Enlarge

2013 was the lowest the management achieved, but over a 10-year period, the average has been about 30%. Over the past 5 years, you can see the median value is 26.1%, thanks to the big growth in 2014.

High Gross Profitability Signals Outperformance

Another fundamental metric/signal I look at is Gross Profitability (GPA) created by Robert Novy-Marx.

The idea is that great companies achieve greater profits off of their existing assets. A lot of value traps are cash boxes that don't deliver value. They hold a lot of cash, but they don't generate anything with it. A high GPA is better, and I've conducted internal tests where a GPA at or above 1 yields excellent performing stocks.

So here's the GPA trend for Gilead Sciences:

GPA Shows Efficiency of Assets (HIgher is Better) | Enlarge

With the way Sovaldi and Harvoni have exploded onto the scenes, I can see GPA increasing as revenue increases over the years. There are recent concerns that the subscriptions to the drug is declining just one year in which is causing jitters in the stock.

What Are The Market Expectations For GILD?

For stocks I'm not sure about, one of the first things I do is to calculate what the market is pricing in the stock.

I mentioned that the market is jittery with Gilead right?

Let's find out what those jitters are.

First, analysts are projecting zero growth. Actually, Yahoo Finance shows that analysts are expecting -1.4% in revenues in 2016 and -0.4% in EPS.

Past numbers don't help that much when valuing biotech stocks because it's truly a case of past performance doesn't indicate future performance. That's why I'm first focusing on making sure that the company is well run, has good management and owns a strong moat.

So, let's do things backwards.

Crunching the Reverse Valuation To Determine Expectations

Start with the current stock price and do a reverse DCF to see whether the current expectations are realistic.

The main benefit of a reverse DCF is that you don't have to know what growth rate. The objective is to play with the growth rate until you can match the value to the stock price. That way, you can see what the market implied growth rate is and decide whether it's realistic or not.

After all, Ben Graham said that:

You don't have to know a man's exact weight to know that he's fat.

Here's what I mean.

Known variables:

- Stock price of $98 (at the time of writing)

- analyst expected EPS growth of -0.4%

- TTM net income of $15.04b

- discount rate of 9% (my choice)

- terminal value of 2%

With these numbers, it's possible to find the market implied growth rate as shown in this screenshot.

Reverse DCF Shows Low Growth | Enlarge

Reverse DCF Shows Low Growth | Enlarge

The market is expecting a growth rate of -0.6%. Very close to the -0.4% that analysts are expecting.

Based on this, the important question is this.

Is the negative expected growth realistic or unrealistic?

Maybe for a single year, the negative growth is understandable. However, the past 5 years Gilead Sciences has achieved an EPS growth rate of 39% and sales growth rate of 28.8% – without Sovaldi and Harvoni.

Gilead Sciences Is Worth…

With the reverse DCF out of the way, the lower end of the valuation is the current stock price in the $90 range. Somewhere around $93-98.

Note that I'm referring to intrinsic value and not price.

The stock price can easily fall below $98, but the intrinsic value isn't going to change as quickly.

Don't mistake the stock price for intrinsic value.

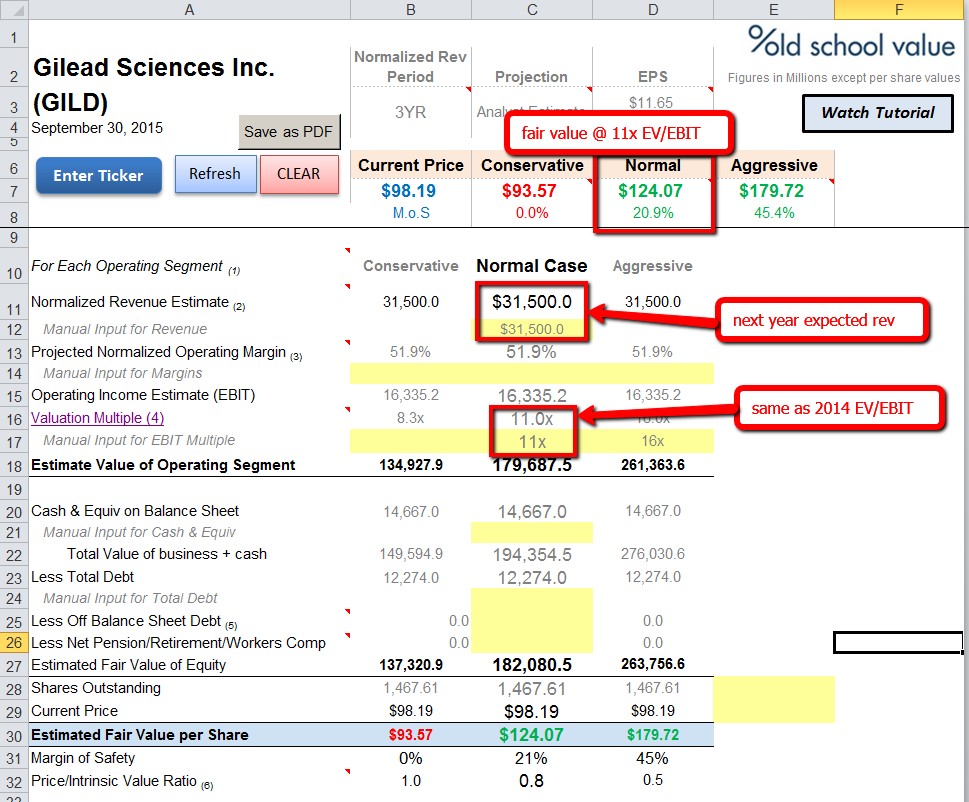

Now look at the screenshot below to see that the low range is $93 when I use the 5-year minimum EV/EBIT multiple.

The normal valuation at 11x EV/EBIT based on 2014 numbers comes out to $124.

The aggressive multiple of 16x EV/EBIT is $180, but based on historical valuations, it's not a realistic intrinsic value range.

Based on this, my intrinsic value range is between $93 and $125.

I like to buy with a 25% margin of safety, which means the stock price should be between $74 and $93 to start a position.

It's not far off, but I'd need to let it fall more before taking a position. After all, it's the buy price that determines whether you make money or not.

Disclosure

No position.

This post was first published at old school value.

You can read the original blog post here Is Gilead Sciences Worth $100 or Not?.