“Davidson” submits:

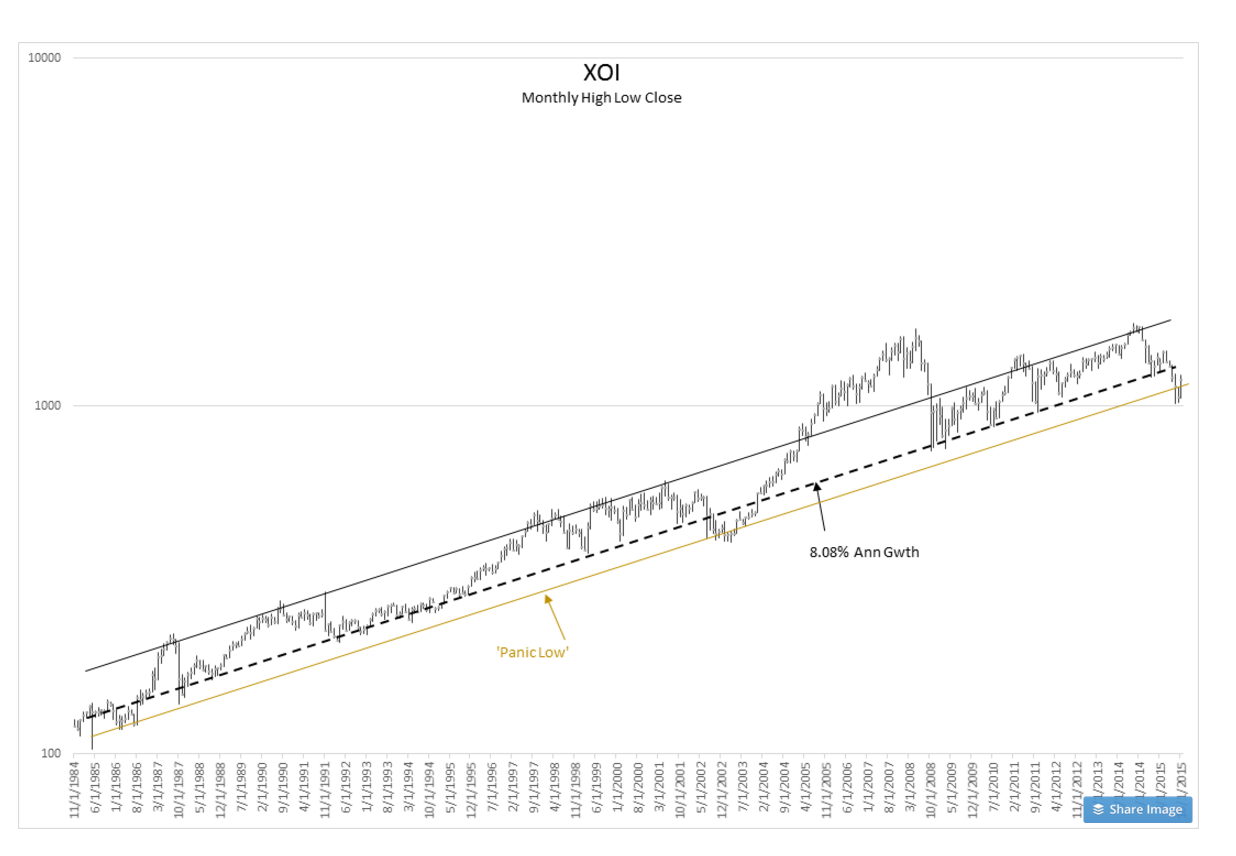

n my experience (this is an experience and investment judgement thing and not a ‘math thing’) the best way to judge current energy markets and oil ($OIL) ($USO) price trends is to look long term using the $XOI Index, an energy industry company index with a long history. This index is long enough to factor in sufficient history to include impact from inflation, changes in the import/export relationships, growth of emerging markets, changes in tax laws, political agendas, growth in global GDP, changes in population, changes in environmental efficiencies, emergence of alternative sources of energy and advances in technology all of which is impossible to calculate except by seeing how we acted and priced these impacts in the past. In my experience the history of the XOI is the best means we have of determining what the future is most likely to present investors. Because this method trusts that more of the ‘same’ is likely going forward, it is called the empirical method of analysis. One must use a semi-log plot for the data as it is the only means to handle data which represents a growth series-see below. This is not to be confused with Technical Analysis which does not use semi-log plots. The 20 members of the XOI are shown at the bottom.

My interpretation is that energy prices have likely bottomed even with the latest cost reductions from additional ‘fracking’ discoveries. In my opinion the 2015 drop of the XOI to the trend line representing ‘Panic Lows’ signals we have reached our low point. There are economics at the current levels of energy prices which make additional production efforts non-economic. The forecasts for substantially lower prices from current levels with producers somehow being forced to continue non-economic production has never held up at past market lows. Production always adjusted lower during previous price lows, till global consumption gradually pulled prices higher. Acceleration in consumption during periods of low pricing has never been the basis of market rebalancing as much as production declines.

No one has a record of predicting when ‘Panic Lows’ will occur. This does not mean that one cannot use the historical record to enhance investment decisions. I recommended in early 2015 that investors add to Natural Resources. I continue to recommend this action. Changes in investor psychology which differs from broad economic trends offer opportunities to patient investors who are able to look long term. Current conditions offer such an opportunity. In my opinion the precipitous drop in oil prices in 2014-2015 was due to Hedge Funds repositioning out of inflation bets which never materialized. They panicked! As a result oil pricing has fallen below levels which make production economic. Prices will rise in the future as consumption works inventories down to the level at which production activity resumes.