For weekend reading, Gary Alexander, senior writer at Navellier & Associates, offers the following commentary:

When Bear Markets Die

You can look at October with fear (a mistake), or with the rational hope that many bear markets tend to die in October, especially in mid-term election years. You can probably recall a few by memory, like…

Q3 2022 hedge fund letters, conferences and more

Find A Qualified Financial Advisor

Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

- 60 years ago this week, in 1962, the Cuban Missile Crisis was resolved in the last week of October after the S&P 500 bottomed on October 23 and soared by over 10% in November.

- 35 years ago, in 1987, Black Monday saw the biggest one-day drop in the market ever (-22%), but then came a 13.7% gain over the next two weeks in the S&P 500 and +15.8% in the Dow.

- In 1990, the S&P 500 dipped to 295 on October 11 (down 20% in under three months, due in part to Saddam Hussein invading Kuwait), but then it gained nearly 12% by year’s end.

- In 1998, the S&P 500 fell 15% from July 8 to October 8 (mostly due to a hedge fund failure at Long-Term Capital Management), but then it gained back 21% by Thanksgiving week.

- 20 years ago, in 2002, the S&P bottomed out at 776.76 on October 9 after losing 49% in just over two years, but then it gained 14% by October 31 and doubled in five years, setting new highs.

Four of those five examples came in mid-term election years, like this year (the only exception is 1987).

This year, so far, the bottom in the S&P came while I was at the New Orleans Investment Conference listening to the super-bears talking about a “coming” crash (that was ending). As it turned out, the closing bell on Wednesday, October 12 found the S&P’s low close of the year at 3,577.

It opened much lower, down another 2.4% on Thursday morning, October 13, before recovering. That’s when a New Orleans super-bear was saying that the market had a lot further to go down.

We can’t claim the worst is over yet, but in less than seven trading days since that “Thursday the 13th” low, the S&P is up 7.48% as of last Friday’s close. NASDAQ is up 7.64%, and the Dow is up 8.45%.

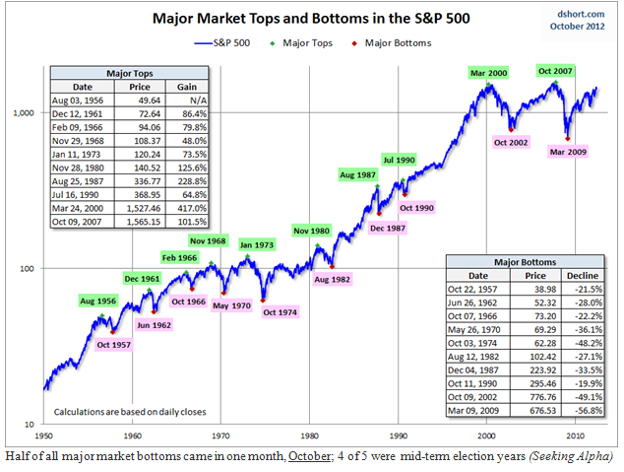

If you look at all of the bottoming dates above, past October lows came on October 8, 9, 11, 19, and 23.

Previous bear market lows came later in the month, on October 27, 1923, October 22, 1957, and October 25, 1960, so this year’s low is right in the sweet spot of past October lows, “when bear markets die,” or if you prefer a more peaceful analogy, a time when most well-fed bears go into a long winter hibernation.

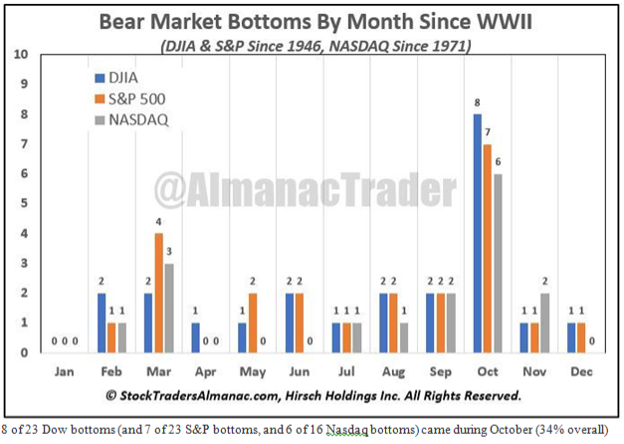

According to a September 23 post in TheStreet, the Stock Trader’s Almanac reports what we have said here often: “September is the worst month for stocks,” not October.

In fact, October is better than average – the 5th best month since 1950, and “returns are substantially better than usual in mid-term election years, with the S&P 500 and NASDAQ returning 2.7% and 3.1% on average.

Between 1999 and 2003, Octobers were big winners during the Internet bust when high-valuation stocks were similarly entrenched in a vicious bear market. The Stock Trader’s Almanac writes that October ‘turned the tide in 12 post-WWII bear markets: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002, and 2011.’”

“October also ends the Almanac’s ‘worst six months of the year,’ setting the stage for historically stronger returns. According to the Almanac, November is NASDAQ’s best month of the year during mid-term election years, returning 3.5% since 1971.

Furthermore, the six months from November through April have generated an average return of 7.5% on the Dow Jones Industrial Average, versus a 0.8% average gain from May through October. Since many bear markets have coincidentally ended in October, it’s called a ‘bear killer.’”

Ed Yardeni and his chief quantitative strategist Joe Abbott confirm this, saying that “since 1928, the S&P 500 fell 1.1% on average during September, by far the worst performance of any month. October, November, and December were up 0.5%, 0.6%, and 1.4% on average.”

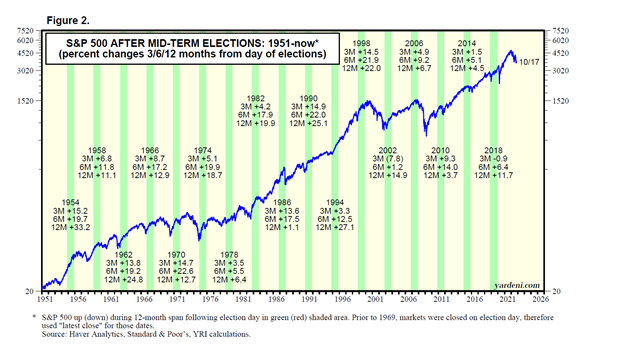

Abbott calculates that “since 1942, during each of the 3-month, 6-month, and 12-month periods following each of the 20 mid-term elections the S&P 500 was up on average by 7.6%, 14.1%, and 14.9% (see chart).

Only the Fed Can Scuttle This Recovery – So They Need to Read Some History

At the end of September, October has been the best month of the year in mid-term election years like this, gaining an average +3.33% in the 60 years (15 election cycles) since 1962, including a devastating 7% loss in 2018, last time around, due to Fed Chair Powell raising rates one or two times too many, a mistake he will certainly (one hopes) learn not to repeat this time around, right?

Inflation issues are driving a lot of voters to the polls in two weeks – if they can afford the gas (or EVs). The September CPI report shows 8.2% overall inflation, and 6.6% core inflation (excluding energy and food), the biggest annual rise since August 1982.

This raises fears that the Fed will “overshoot” again, as they did in 2018, ignoring lag times by raising rates by huge giant steps at every FOMC meeting this year.

The Fed is the biggest threat to a potential fourth-quarter recovery in the stock market and the economy.

The Federal Reserve was born as a result of what happened 115 years ago this week, when an aging J.P. Morgan, Sr., was a one-man central banker who rescued the economy in one night. Maybe there are some lessons we can learn from Morgan’s 1907 actions that this Federal Reserve can apply to the Crisis of ‘22.

On Monday, October 21, 1907, the Panic began with a run on the Knickerbocker Trust Company, the third-largest bank in the city. John Steele Gordon wrote (in “The Great Game: The Emergence of Wall Street,” pp. 190-191): “Bedlam reigned as depositors fought to get to a teller and withdraw their assets from the bank’s imposing new headquarters on Fifth Avenue.

Many thought that the Clearing House would have no option but to come to the aid of a bank as large as the Knickerbocker, but it did nothing.”

On Tuesday, Knickerbocker’s president bravely opened the doors – not a wise move. Within a few hours, depositors withdrew $8 million. By afternoon, Knickerbocker declared its insolvency and closed its doors

On October 23, lower Manhattan was choked with anxious depositors lined up in front of even the soundest of banks. After Knickerbocker failed, the Trust Company of America looked suspect. By 1:00 p.m., they had only $1.2 million cash on hand.

By 1:20, it was down to $800,000. By 1:45, they had $500,000 and at 2:15 they were down to $180,000. About then, the bank’s president, Oakleigh Thorne, rushed over to J.P. Morgan’s office to seek help.

When Morgan was convinced that the Trust was sound, he said, “Then this is the place to stop the trouble,” and he ordered money sent to tide the bank over for the rest of the day. The U.S. Treasury (before the Federal Reserve was born) was not authorized to bail out banks, so Morgan deposited $35 million in troubled banks and told those banks to lend the money out.

On Thursday, October 24, the New York Stock Exchange came to J.P. Morgan’s door and said, in effect, “Please make enough cash available to our banks and brokers to meet their obligations, or we will close the Stock Exchange.”

Morgan refused to let the Exchange close, so he called all the major bankers to his office. Within five minutes, he raised $27 million. Then, he said that any bears would be “dealt with.”

That night, Morgan called every important banker in the city to his private library on East 36th Street. After hours of indecision, the bankers came up with a bold plan to use clearinghouse certificates instead of cash to settle transactions. The effect was to increase the money supply by a then-huge $84 million.

As quickly as that, the Panic of 1907 was over. It was J.P. Morgan’s shining and defining moment. Even his competitors compared his leadership to great generalship in a war, and President Theodore Roosevelt, who earlier that year had railed against “the malefactors of great wealth” now said, “Those substantial businessmen acted with wisdom and public spirit.”

Maybe our Federal Reserve can do the same today.