Homeowners across the country and much of the world are seeing their mortgage rates jump, as central banks continue to bump up prime interest rates in an ongoing effort to dampen stubbornly high inflation.

In the United States, the average 30-year-fixed-mortgage rate went up by 20 basis points to 6.66% on Monday, February 13. During the same period, the average 20-year refinance rate increased to 6.77%, during the same period after jumping upwards by 26 basis points from the week before.

Q4 2022 hedge fund letters, conferences and more

While inflation has remained steady, ending December at 6.5%, the Federal Open Market Committee (FOMC) hawkishly raised rates again during its February meeting by 25 basis points to 4.5%-4.75%. Several aggressive hikes last year, and the most recent has pushed the cost of borrowing to its highest levels since the 2008 financial crisis.

It’s not only American homeowners and would-be buyers that are seeing mortgage rates and house prices rise faster than what their income has over the last several months.

In the United Kingdom, the Bank of England raised its prime base interest rates by 0.5 percentage points to 4% at the beginning of February this year. The ongoing increase has led to a sudden slowdown in home loan approvals, which dropped to 35,600 in December, marking the fourth consecutive decline.

In Canada, nearly 45% of homeowners with variable mortgages have said they would have to sell their properties in the coming nine months as many are struggling to grapple with increasing borrowing rates in a recent Yahoo/Maru Poll.

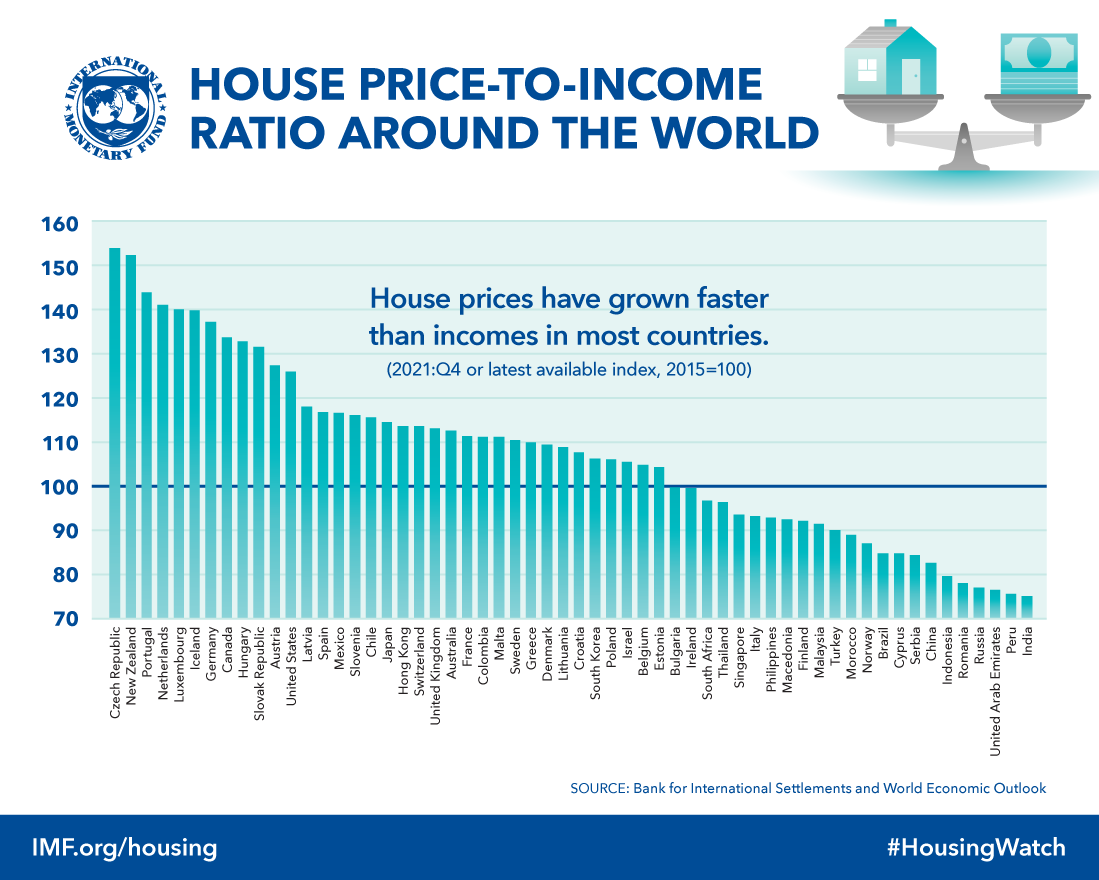

Countries including the Czech Republic, New Zealand, Portugal, Netherlands, and Luxembourg, among other developed nations have seen house prices rise faster and more rapidly than buyers’ income has according to fourth-quarter figures released by the IMF.

After enjoying a banner year of red-hot sales during the early months of the pandemic as rates fell to near zero, and demand soared, potential buyers have now been priced out of the market, only to be met with painstakingly high lending rates.

Those that are unable to enter the market, due to low supply, pent-up demand, and higher-than-expected prices, they’re perhaps sitting on the right side of the fence and conditions only deteriorate further and experts predict a housing market correction looming on the horizon.

On the other side, those with fixed and variable mortgages have had to make some rapid adjustments in an attempt to keep their balance sheets on track as the central bank initiates a flurry of rate hikes.

Moving Away From Deferred Payments

During the height of the pandemic in 2020, a majority of homeowners chose to skip payments on their mortgages, as financial instability, unemployment, and market volatility pressured them to use their cash for other essentials. A poll from 2021 revealed that 62% of homeowners agreed that they felt pressured about making repayments in the future.

In the same poll, 59% of those surveyed who were in forbearance said that their financial stability depended largely on delaying mortgage payments. While in time mortgage repayment has sped up again, homeowners are trying to avoid forbearance as much as possible as a way to cope with fluctuating economic and market conditions.

Opting For Fixed-Mortgage Rates

Due to the pace at which the central bank has increased interest rates in recent months, more and more would-be buyers and current homeowners are opting for fixed-mortgage rates as the coming months remain uncertain.

Those with better credit scores are making the effort to apply for conventional or fixed-mortgage rates instead of adjustable rates. This way they are certain that their repayments will remain on track in the coming months, and they can budget accordingly to ensure they make repayments on time.

Holding Off On Refinancing

During the early days of the pandemic, countless homeowners rushed to refinance their mortgage loans as rates fell to near zero. The chances of that happening anytime soon again is perhaps unlike, even with the potential of mortgage rates coming down in the last half of the year.

Signing a better deal right now could seem impossible, and those that bought a house in 2022, when rates were already high, could only look to refinance in the next year or so, perhaps at the end of 2024 even. Some experts suggest that it would only make sense to refinance mortgage loans if rates are at 1% or lower, but the chances of that happening anytime soon again are looking slim.

Paying Debt Off Quicker

There’s been a constant tug and pull between Americans and debt, and according to an Experian study, around 340 million Americans currently carry some form of debt. A further look revealed that in 2021, the average consumer debt balance stood at $96,371, an increase from the year before.

Large sums of debt, paired with the cost of living crisis, and slowing economic activity have made it harder for many Americans to pay off as much of their debt as possible. While there is still a large percentage that can make pay off their debt, many are opting to rid their balance sheets of smaller debt first and quicker in an attempt to stabilize their financial position.

Choosing Smaller Repayments And Budgeting Better

An alarming amount of Americans are unable to make it through the month with their current income and wages. As of December 2022, more than half, or 64.4% of American adults reported having no money left at the end of the month. Across most income levels, even those earning $100,000 per year are seeing themselves living paycheck-to-paycheck.

Instead of taking on more debt or burdening themselves with even more financial problems, homeowners and would-be buyers are striking up new ways to make ends meet and having to budget more appropriately. Improved budgeting, and caring for household income have largely been a way for many adults to ensure they can make mortgage payments or afford a new home.

The Bottom Line

While there is a potential chance for mortgage rates to come down in the later part of the year, those looking to enter the market right now will find themselves in a tight squeeze. What’s more, current homeowners are holding out to see whether rates could decrease slightly, to at least give them a bit of breathing room.

It’s hard to say which direction the pendulum will swing in the next few months, or even a year from now. Besides these uncertainties, it remains vital for homeowners and buyers to choose mortgage payments that they can afford, and consider putting down a larger deposit.

Ongoing economic problems are looking to remain for the next several months, but if homeowners can take better control of their finances, then they’ll at least be able to stabilize their balance sheets.

{kind=link}