IPO investors set to accept more than 40% in losses in the go-private transaction but is it a lifeline bailout?

American outdoor grill manufacturer Weber Inc’s (NYSE:WEBR) stock rose 23.2% higher on Monday, closing at $8.01 after receiving a revised takeover offer worth $2.3 billion from private equity shareholder BDT Capital Partners.

Q3 2022 hedge fund letters, conferences and more

Find A Qualified Financial Advisor

Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

In early October, market sources in the sector first began leaking to the press that Weber management had begun considering debt financing options from its largest shareholder, BDT Capital Partners.

BDT Capital Partners currently owns around ~48% of the float with ownership of around 25.5 million shares.

A few weeks later, BDT Capital Partners in a 13D/A filing disclosed a proposal to acquire all outstanding WEBR shares at $6.25 per share in cash.

Following discussions with the Board, BDP Capital strengthened its offer to $8.05 per share, representing a ~60% premium to the closing price of shares on the 24th of October (when the first offer was announced). The new offer also represented a 28.8% further premium to the initial $6.25 offer.

A special committee of the Weber board, composed solely of independent directors determined that the proposed transaction is in the best interests of shareholders and unanimously recommended that the Board approve the transaction.

Weber’s Board approved the transaction with interim CEO Alan Matula commenting to shareholders stating “We are confident that this transaction provides immediate and fair value to Weber minority shareholders”.

The transaction is expected to be completed in the first half of 2023 subject to closing conditions which includes HSR clearance.

But is this a good deal for shareholders? The revised offer comes at a -42.5% discount to the $14 IPO price which was set 14 months earlier.

Analysts from BMO Capital Markets said on Monday that the offer price below the IPO price demonstrates the tough macroeconomic environment that grill manufacturers are facing after the significant Covid-related demand boosts over 2020 and 2021.

During the last financial investor update during August, Weber reported a net decline in sales by -21% to $528 million during the third quarter. WEBR generated a net loss of -$52 million compared to a net profit of $18 million in the prior year as demand and inflationary pressures hit the button line.

Later on Monday evening, several M&A and class action related law firms announced that they would be investigating the deal to see if the directors acted in the best interest of shareholders when approving the sale to its controlling shareholder.

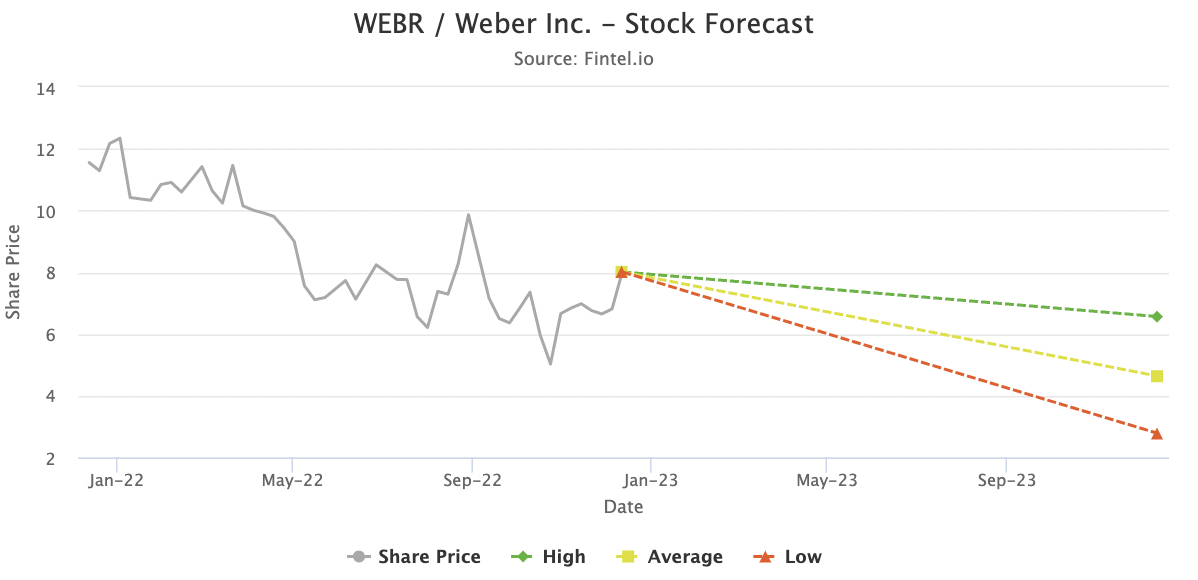

Fintel future forecast data for WEBR has an average consensus target price of $4.63 with a high target of $6.56 and a low target of $2.78. The chart below shows the forecasted range of share prices in the market prior to the offer.

Analysts remain bearish on the outlook for the company with the absence of an offer on the table.

Article by Ben Ward, Fintel