Boise Cascade Co (NYSE:BCC) is an integrated manufacturer of wood products and a wholesale distributor of building materials with operations primarily in the US. BCC’s products are used mainly in new residential construction, renovation projects, light commercial construction and industrial applications.

BCC is currently the stock with the second-highest Quality, Value & Momentum (QVM) score of 92.83 on the Fintel platform. The QVM score is derived from Fintel’s quantitative analysis that looks at the firm’s valuation (relative to peers), six-month momentum and the firm’s efficiency in generating cash.

Q1 2022 hedge fund letters, conferences and more

BCC trades at 3.7 times trailing earnings and has a rolling forward dividend yield of 5.9%, based on a quarterly dividend of 12 cents per share. This excludes the special dividends that BCC has been paying regularly. To highlight the recent significant supplementary dividends that have been paid, $2.50 was paid in June 2022, and the $3.00 was paid in December 2021 to distribute significant earnings to investors.

BCC also features on the Fintel Dividend leader board for US stocks in the 7th spot with a score of 96.43. This score is based on the firm’s consistent dividend growth rate and yield.

Boise Cascade reported first quarter results after market on the 5th of May that topped analysts’ expectations at the sales and profit levels. The firm posted EPS of $7.61 compared to a forecast of $6.60 per share and group revenue of $2.33 billion during the quarter vs a consensus estimate of around $2.2 billion. BCC’s shares fell -by 6.9% the following day on the results.

Management provided some outlook commentary for the year ahead, noting, “Demand for the products we manufacture and the products we purchase and distribute are correlated with new residential construction, residential repair-and-remodeling activity and light commercial construction.” Management went on to discuss how the work-from-home trend will continue to create a favorable demand environment for new residential construction that they expect will remain strong during 2022.

They also noted that increasing the prices of commodity products allows for higher sales and margins from the distribution business. Still, a declining price environment exposes BCC to declines in sales and profitability.

Analyst Views And Commentary

Post Q1 results, analyst Reuben Garner at the Benchmark Company downgraded the recommendation on the stock to ‘hold’ from ‘buy’ previously as the stock reached the $82 target. The firm notes that if commodity price pressures or housing concerns drive shares lower, it will be looking to take advantage of the volatility.

Kurt Yinger from DA Davidson noted that Q1 results outpaced the firm’s estimates which saw them raise their price target from $82 to $88 per share. They forecast that BCC will generate another $10 per share in cash by the end of 2022, which is likely to suggest additional supplementary distributions over 2022. The firm remains ‘buy-rated on the stock.

Susan Maklari from Goldman Sachs returned the Q1 result with confidence that Boise can leverage its favorable supply/demand dynamics despite unpredictable commodity prices. However, the current volatile nature of the wood products market and broader macro uncertainty as interest rates move higher has caused the firm to retain a ‘neutral’ rating with a target price of $88 that rose from $82 prior.

BCC has a consensus ‘overweight’ rating with an average target price of $85, implying 5.8% to the current share price.

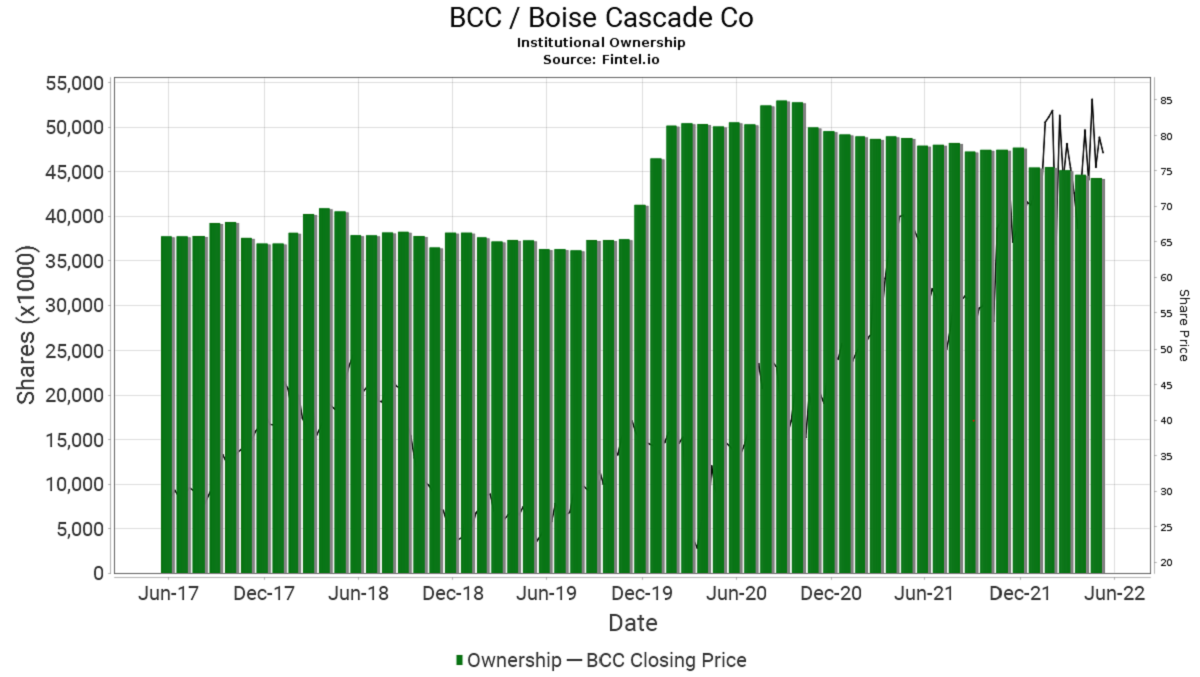

Fintel analysis on ownership accumulation showed that BCC has a score of 71.57, which ranks the company in the top 15% of 24,000 included peers. The score is based on a multi-factor quantitative model that helps identify companies with high levels of institutional accumulation. We note that BCC has 699 institutions that hold 44.3 million shares on the register. We have included a chart below showing the slow decline of institutional ownership over the last two years that has had an inverse relationship with the growing share price. This was likely attributed to institutions taking profits from large share gains in a volatile market.

Article by Ben Ward, Fintel