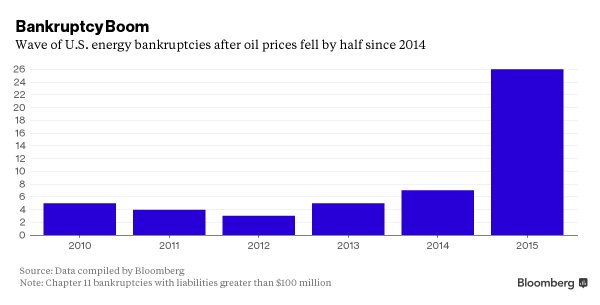

Energy Bankruptcy Boom 2015

Dozens of oil and gas companies went into bankruptcy last year. While energy E&P companies were dropping like flies in 2015, credit rating agencies and banks have remained awfully quiet and apparently buried their heads in the sand.

You see, the Fall Borrowing Base Redetermination by banks on the E&P sector was supposed to take place around October 2015. According to a Haynes and Boone, LLP survey conducted prior to the fall borrowing base redetermination season, industry observers and insiders are predicting a decrease in the ability to borrow against reserves by an average of 39%.

The result of base redetermination does not require public disclosure. Nevertheless, it seemed banks were extremely lenient as the average reduction for 17 companies disclosing the borrowing base reduction results was just 4%. Rating agencies, meanwhile, did not make major E&P downgrade actions till this month in 2016.

It’s About Time!

On Jan. 22, 2016 Moody’s Investors Service said it put 120 oil and gas companies on review for downgrades. Rival Standard & Poor’s Ratings Services was way ahead of Moody’s. S&P said it already downgraded the debt of 165 U.S. companies back in 4Q 2015, representing $1.5 trillion, led by the oil, gas, and commodity sectors. S&P also said for the full year, downgrades rose by 67%, to 461, the highest level since 2009. From late December to January 2016, Fitch also took individual downgrade action on companies such as NGL Energy (NGL: NYSE), Chesapeake Energy (CHK: NYSE) and Williams (WMB: NYSE).

Wall Street’s Lifeline to Frackers

We can see how banks do not want to write off and take the loss of the E&P debt on their books and have motivation to keep feeding the high leverage and not call in the energy loans during the base determination last October.

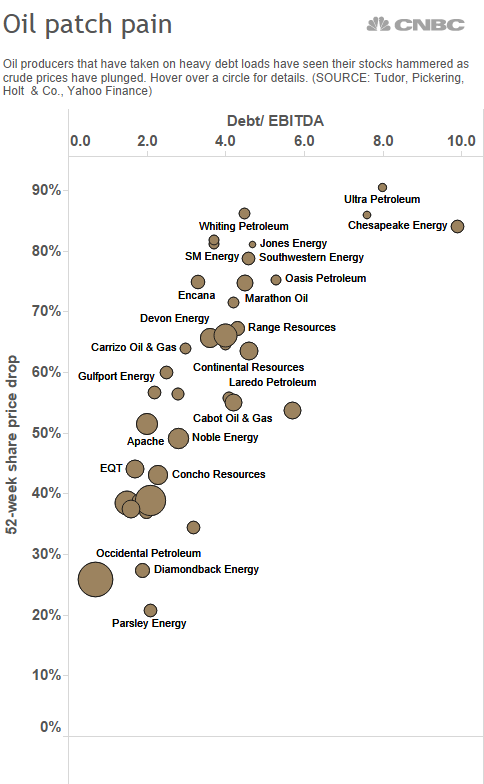

FT reports that as of September 2015, about a dozen E&Ps already had debts as high as more than 20 times their EBITDA. One of the reasons pushing down oil price to the current historical lows, and yet no sight of decline in U.S. production is that quite a few small frackers need to pump oil regardless (even below the economic threshold) just for the cashflow to pay bills and payrolls.

So the collective action by banks to sustain the life of many weak oil frackers (so not to incur losses) basically exacerbated the oil over-supply and price crash.

Why the Downgrade Delay?

On the other hand, we fail to see the motivation and logic behind the delay by rating agencies who are supposed to have independent evaluation model (from banks) to provide forward-looking financial risk indications.

It is so ironic to see how barely a year ago Moody’s essentially defended the frackers the same time when Einhorn slammed ‘Mother Frackers‘ (prompted a watershed event in oil E&P stocks) last May.

At the time, Moody’s said,

…[The oil and gas sector] liquidity-stress index (LSI) more than doubled….[however], the [LSI] index is still well below its 26% peak in March 2009 …..default risk remains benign ….

[Emphasis Ours]

From there, we can only draw two possible conclusions from rating agencies delayed reaction/action:

(1) Influences from Banks (or Others) — There is an inherent conflict of interest in the current Wall Street model that rating agencies are basically paid by the ones they are supposed to give ratings on. For readers who saw the movie “The Big Short” (from the book by Michael Lewis) should remember how rating agencies were prolifically profiled as influenced by big banks on their rating calls (perhaps that’s why S&P seems to have an earlier jump on the E&P downgrade than the two rivals?)

While nobody can say for sure if this conflict-of-interest situation has improved since the 2008 subprime crisis, it is not hard to draw a parallel Déjà vu from the 2008 subprime/housing sector with possible banks influencing rating agencies to the current E&P sector. A even better question right now would be: Is this to allow some insiders time to position themselves “on the right side of the trade”?

(2) Extremely flawed (perhaps even delusional) oil price assumption by rating agencies. While EconMatters outlined why WTI is a short as early as July 2013, it is pretty basic (if not alarmed by the booming oil bankruptcies and layoffs) for any competent Wall Street or rating agency analysts to at least reached a similar oil price scenario by 3Q 2015. But rating agencies did not come out and act accordingly until early 2016. (In the same vein, it is highly questionable why Moody’s all of a sudden jumped on the bandwaon of oil price forecast.)

Fracking Bubble 2015-2016

FT reports the 60 leading US independent oil and gas companies have total net debt of $206bn, more than doubled from about $100bn at the end of 2006. Supposedly almost a third of the 155 US oil and gas companies covered by Standard & Poor’s are rated B-minus or below (highly speculative, below investment grade).

We don’t always agree with Einhorn on a lot of his view including Apple long and some of his specific E&P shorts. However, we do see a bubble in the E&P sector not much different from the 2000 tech bubble. We noted last May that “the sector is long overdue for a shakeup” with 110+ publicly traded E&P companies in North America (mid to small caps), and many of them came to market just in the past five years to hit their IPO pay dirt.

More Pains To Come

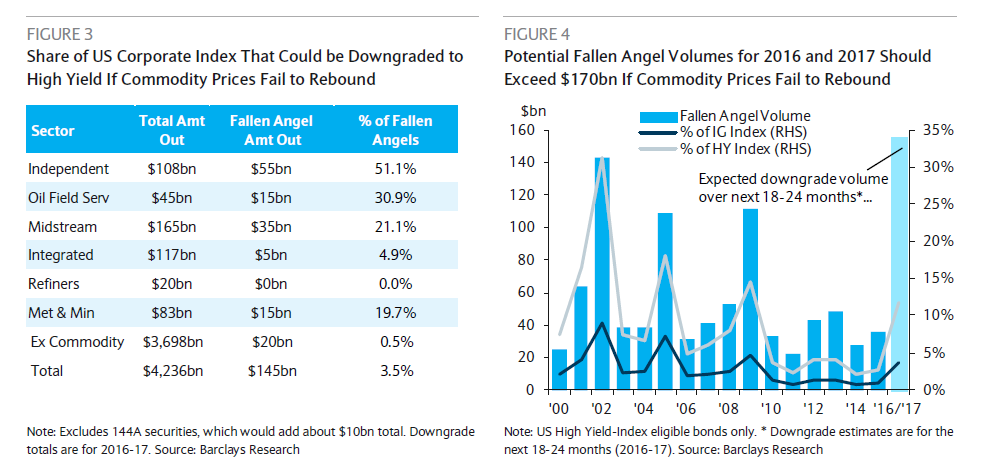

Many highly leveraged and poorly managed drillers have been able to hide under the cloak of high oil prices (and Wall Street) in the past few years. Now Barclays estimates that without a rebound in commodity prices, the potential oil bonds downgrade volume for 2016 and 2017 could exceed $170 Bn and another $155 billion worth of high-yield debt supply will enter the market.

|

| Chart Source: Bloomberg |

The long overdue credit agency downgrade is only the beginning of a tsunami hitting the entire oil E&Ps (bonds and stocks). More E&Ps will go out of business while some solid companies may get smacked down (but hopefully eventually survive) simply by the sector association.

Wall Street had a hand in this Frack Bubble of 2015-2016, not much different from the 2008 housing bubble. We know Shell just fired another 10,000 workers while blobal oil job losses top 250,000, and it is too early to tell how the world market and economy will turn out in this bubble aftermath.

But not to be despair, the better news for now is that with weak E&P companies going out of business, oil production should progress to reflect the logical supply volume in the current oil price environment. That should eventually lead to the rebalance of the oil market, price and the proper valuation of the remaining energy stocks.