The 10 Most Competitive Countries in the World

Since 1979, the World Economic Forum (WEF) has annually published its Global Competitiveness Index (GCI), which, as you can probably guess, ranks the competitiveness of nations for which the group is able to gather sufficient data. This year, the WEF ranks 140 economies—from Switzerland to Guinea.

This is a report I anticipate every year because it’s an indispensable tool that helps policymakers and business leaders better understand what works and what doesn’t in creating stronger, more transparent, more efficacious societies that foster success and prosperity.

For the very curious, the more-than-400-page report is available for download on the WEF’s website.

Global Growth Starts at Home

The WEF defines competitiveness as “the set of institutions, policies and factors that determine the level of productivity of an economy, which in turn sets the level of prosperity that the country can earn.”

I agree with this definition. I often point out that government policy is a precursor to change, that such policy changes, such as the one India recently instituted regarding gold-investing, have powerful—and sometimes damaging—consequences, many of them global. Here in the U.S., consider the recent implementation and impact of Dodd-Frank, or Obamacare, or FATCA (the Foreign Account Tax Compliance Act).

A recent Sovereign Man post makes this point very emphatically:

U.S. regulations have made its entire population guilty of crimes they’ve never heard of, often for the most innocent and innocuous activities.

Operating lemonade stands without a permit, collecting rainwater, failing to file a government survey are just a few activities now treated as criminal conspiracies.

And yet the government continues to publish upwards of a 1,000 pages PER DAY of new rules, regulations, and other proposals.

Presidential candidate Donald Trump agrees. In a Washington Times op-ed, he wrote that “government regulations cost us annually $1.75 trillion. They constitute a stealth tax that is larger than the amount the Internal Revenue Service collects every year from corporations and individuals combined.”

|

I invite you to check out a Business Insider slideshow of the 12 most ridiculous government regulations in the U.S. In Massachusetts, for instance, daycares are mandated by law—by law—to ensure that children brush their teeth after lunch.

Consider this. In the U.S., we cap debt. We cap pollution. Imagine if we did the same for rules and regulations.

Please don’t get me wrong. Every sport requires a rulebook and referee of some kind, but the game becomes increasingly difficult to play when the rules keep changing and getting more restrictive. At some point, government spending relating to such rules and regulations becomes too cumbersome. The cost exceeds the benefit, in other words, as you can see in the chart known as the “Rahn curve,” named for American economist Richard W. Rahn.

I also frequently comment that governments and economic partnerships, such as the European Union, must maintain a healthy balance between monetary and fiscal policy to remain competitive on the world stage. When economies rely only on monetary policy but fail to address fiscal issues such as punitive taxation and over-bloated entitlement spending, imbalances occur. These imbalances inevitably slow the engines of business and innovation, like cholesterol in one’s arteries.

|

As for gold, many CNBC reporters like to comment on the metal’s recent underperformance, when in fact gold was down substantially less than the S&P 500 Index this past quarter. Government policy is imbalanced with restrictive, choking global regulations for trade and focused instead on tax collection. We need to reform taxes and streamline regulations to stimulate economic activity.

Speaking of which: Every year, the GCI lists what policymakers and business leaders identify as the most “problematic factors” for doing business in individual countries. It should come as no surprise that the top five factors on average include, in ranking order, 1) government bureaucracy, 2) tax rates, 3) restrictive labor regulations, 4) access to finance and 5) complexity of tax regulations.

Regarding access to finance, the GCI notes that it has worsened in recent years. This worsening is certainly the result of the global financial crisis seven years ago, but financial regulation has gone too far, paralyzing the flow of credit.

As proof of this, the group writes: “Access to finance is now almost as problematic in advanced as in developing economies.”

The WEF’s insight, research and guidance are as needed now as they’ve ever been. We continue to see deterioration in the global purchasing managers’ index, mostly as a result of the “problematic factors” listed above.

As large and important as China’s economy is, we can’t place the blame solely at the feet of its slowing economy for the world’s problems. If we truly wish to see an upturn in business and manufacturing activity, individual governments need to address the ever-amassing regulations, tax complexity and bureaucracy that act like sandpaper to the progress of business, innovations and prosperity.

Biggest Gainers and Losers

Before I share with you the top 10 most competitive nations—which haven’t really changed from the previous year—I want to highlight a few countries that made either some significant gains or losses.

|

The country that leaped the most was India, rising 16 spots from number 71 last year to 55. I don’t think many people will find this surprising. Prime Minister Narendra Modi’s election last year ushered in a new era of business development, foreign investment and anti-corruption. The “Make in India” initiative, launched by Modi in September 2014, has helped the country surpass China as the world’s top destination for foreign direct investment.

As I shared with you in March, India was the best-performing emerging market in 2014, rising more than 29 percent. Many analysts, furthermore, estimate that the country will emerge sometime this century as the world’s third-largest economy, following China and the U.S.

The GCI points out, however, that India continues to face significant challenges. Infrastructure deterioration, a huge lack of access to electricity and slow technological readiness are concerns Modi’s administration must take urgent action on.

Other notable climbers were the Czech Republic (gaining six points), Kazakhstan (eight points), Russia (eight points) and Vietnam (12 points). I shared with you last month that the Czech Republic has the highest PMI reading among emerging European countries and the fastest-growing economy in all of Europe, so its ascent was very much expected.

You might be taken aback, however, to see Russia rise so much, especially after the plunge in oil prices—so important to the country’s budget—the weakening of its currency and the imposition of additional sanctions following its invasion of Ukraine. The WEF no doubt anticipated readers’ disbelief as well, because it writes: “[T]his is explained mostly by a major revision of purchasing power parity estimates by the IMF (International Monetary Fund), which led to a 40 percent increase in Russia’s GDP when valued at PPP.”

|

The country that plummeted the most was one of India and Russia’s fellow BRIC countries, Brazil. Falling 18 spots, the South American nation now sits at number 75 out of 140, compared to last year’s 57.

As with India, no one should be shocked by this. The Marxist policies of President Dilma Rousseff, in office since 2011, have only managed to suffocate business development. Brazil ranks as one of the very worst countries in terms of burdensome government regulations, ethical business practices, effect of taxation on incentives to invest and hiring and firing procedures.

Besides a loss of trust in public and private institutions because of rampant corruption, the GCI cites Brazil’s “large fiscal deficit,” “rising inflationary pressure” and “weak macroeconomic performance.”

Another BRIC country, China, holds steady at 28. You might recall that back in August, I reacted to the news of China’s stock market correction and economic slowdown, writing that “the world’s second-largest economy has begun to shift away from manufacturing and more toward consumption and the service industries.”

My views here are quite validated by the GCI’s assessment of the Asian country’s current economic condition, stating that China must “evolve to a model” that emphasizes “demand through domestic consumption.”

Crème de la Crème

In the map below, you can see the current top 10 most competitive countries, according to The Global Competitiveness Report.

As I mentioned earlier, not much has changed since last year. No new countries have entered or exited this exalted list, and there was very little rank-shuffling. For the seventh consecutive year, Switzerland is the most competitive country. For the fifth straight year, Singapore is number two. The U.S. comes in at number three for the second year. And so on.

For this reason, I won’t spend much time rehashing what I already said in my coverage of last year’s report. It’s likely you can already identify many of the probable reasons why these nations appear so highly in the index: access to good infrastructure and electricity, quality education and research institutions, availability of the latest technology, strong intellectual property rights and protectionism and much more.

Each one of these 10 countries has its own unique strengths and weaknesses, for sure, but the common theme among them can be traced back to the WEF’s definition of competitiveness. The most successful countries foster “institutions, policies and factors that determine the level of productivity of an economy, which in turn sets the level of prosperity that the country can earn.”

Recall my comparison of Singapore and Cuba in a March Frank Talk. Both small island-states were established in their present forms in 1959—but with two starkly different economic visions. Whereas one government chose to stress sound fiscal policies and an open business environment, the other all but abolished private enterprise.

Today, Singapore is the second-most competitive nation on earth, according to the World Economic Forum. Meanwhile, Cuba doesn’t even rank among the 140 countries the group studied.

To get global growth back on track, it’s imperative that countries follow the leads of Switzerland, Singapore, the U.S. and others that made it to the top of the WEF’s list.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.97 percent. The S&P 500 Stock Index rose 1.04 percent, while the Nasdaq Composite climbed 0.45 percent. The Russell 2000 small capitalization index lost 0.77 percent this week.

- The Hang Seng Composite gained 1.72 percent this week; while Taiwan was up 2.12 percent and the KOSPI rose 1.38 percent.

- The 10-year Treasury bond yield fell 17 basis points to 1.99 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector in the S&P 500 Index this week as the group was overdue for an oversold bounce. Oil prices remained more-or-less flat during the week. The S&P 500 Energy Index closed up 2.81 percent.

- Materials was another strong performing sector this week as China’s purchasing managers’ index (PMI) data for the month of September came in higher than expected. The S&P 500 Materials Index rose 2.71 percent this week.

- Construction spending in the U.S. grew by 0.7 percent between July and August, according to official data released this week. Economists were expecting a slower growth rate of 0.5 percent.

Weaknesses

- Telecommunication services was the worst performing sector in the S&P 500 Index this week, dragged down by Verizon Communications. The S&P 500 Telecommunication Services Index fell 1.06 percent this week.

- Friday’s employment data shocked the markets as the U.S. added only 142,000 jobs in September. Furthermore, a change in nonfarm payrolls for the month of August was revised down to 136,000 from 173,000.

- Average hourly earnings failed to grow between August and September, according to official data released this week. The reemergence of disinflationary pressures looks concerning.

Opportunities

- Given the weak wage and employment data released on Friday, it seems less likely that the Federal Reserve will raise interest rates anytime soon. A few more months of zero interest rates should be good for equities.

- The Conference Board’s Consumer Confidence Index jumped up to 103.0 in September from 101.5 in August, widely beating analyst estimates. Retail stocks should see benefits.

- The Markit U.S. Manufacturing PMI rose to 53.1 for the month of September, beating analyst estimates. Well above the key 50 level, the index remains strong.

Threats

- In direct contrast to the Markit PMI data, the ISM Manufacturing PMI fell in September to 50.2 from 51.1 in August.

- Presidential hopeful Hillary Clinton has certainly created problems recently for the health care industry with her comments pertaining to price gouging. These comments will likely remain a threat moving forward.

- The slowdown in China remains the biggest single threat to the global economy and has the potential to drag down the U.S. economy.

The Economy and Bond Market

Strengths

- Bonds rallied this week, particularly on Friday, as weak employment data and weak wage inflation data out of the U.S. led investors to assume that the Federal Reserve is not close to raising rates.

- China’s manufacturing purchasing managers’ index (PMI) data came in stronger than expected this week. Given the global economy’s dependence on the Asian nation, improvement in China’s economy is directly linked to the U.S. and the eurozone.

- Eurozone’s Markit manufacturing PMI came in unchanged for the month of September, and still remains above the key 50 level.

Weaknesses

- The Markit/BME Germany manufacturing PMI ticked down in September to 52.3 from 52.5 in August, according to official data released this week. On a positive note, the index is above the key 50 level.

- Factory orders in the United States contracted by 1.7 percent between August and September, underperforming analyst expectations. Industrials will be negatively affected by this contraction.

- Deflation has found its way back to the eurozone as the group’s consumer price index (CPI) data fell 0.1 percent year-over-year for the month of September. The return of deflation is particularly concerning given the excessive monetary easing taking place globally.

Opportunities

- Fed funds futures are showing that investors are not expecting a rate hike until March, at the earliest. Lower-than-expected interest rates should boost fixed-income securities.

- Economic confidence in the eurozone rose to a four-year high, according to official data released this week.

- German factory orders are estimated to have risen 0.5 percent between July and August, a sharp improvement from the prior reading. The official data will be released next week.

Threats

- Month-over-month retail sales growth for August is expected to remain flat in the eurozone. Consumer-oriented stocks may be negatively affected if the estimates are correct.

- The weak employment and wage inflation data released on Friday could be the first of many weak readings to come as the global economy begins to falter.

- China’s slowing growth rate and faltering economy remain the largest threat to the global economy. Many analysts are particularly bearish on the contagion effects that could emerge if China’s economic conditions worsen.

Gold Market

For the week, spot gold closed at $1,138.82 down $7.58 per ounce, or -0.66 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, gained 2.65 percent. The senior miners got a reprieve with the late week surge in gold prices and outpaced the junior miners while the S&P/TSX Venture Index lost 2.94 percent. The U.S. Trade-Weighted Dollar Index slipped 0.40 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct -2 | US Change in Nonfarm Payrolls | 201K | 142K | 173K |

| Oct -8 | US Initial Jobless Claims | 275K | — | 277K |

Strengths

- Palladium was the best performing precious metal, gaining 5.26 percent for the week, with continued follow-through from the Volkswagen scandal. The gains are largely speculative as it is not likely that Europe or Volkswagen will abandon diesel vehicles as their main staple.

- September’s nonfarm payrolls disappointed, rising 142,000, which was nowhere near the consensus estimate of 201,000. There was also a decline in workweek data from 34.6 hours in August to 34.5 in September, which equates to an added 348,000 in job losses. Additionally, ratios from the Household report showed that the job participation rate fell to its lowest level since October 1977 (from 62.4 percent to 62.7 percent). Consequently, gold prices jumped $25 in the first 15 minutes after the jobs report was released on Friday.

- In response to their country’s stock market selloff, Chinese investors may be returning to precious metals as a safe haven. Retail sales of gold and silver in China during August rose 17.4 percent year-over-year, representing about $3.9 billion in sales.

Weaknesses

- Platinum was the worst performing precious metal this week as traders shorted platinum to go long palladium, where there might be a shift in demand.

- Gold just had its worst quarterly loss in a year at the close of the third quarter, and close to its worst weekly loss since March. However, the shortfall in the jobs numbers on Friday was a sentiment changer on the likelihood of a Federal Reserve interest rate hike in October or December. Earlier in the week Janet Yellen gave a speech reiterating the Fed’s intention to raise interest rates this year.

- In response to the Fed’s decision to not raise rates in September, and considering Yellen’s comments, Citigroup was espousing that the woes for gold were only delayed rather than avoided. Some analysts have now pushed estimates for a rate hike out into 2016 with the disappointing jobs data.

Opportunities

- Bullion coin sales data indicate impressive figures. American Eagle gold coin sales totaled nearly 400,000 ounces in the third quarter of 2015, compared to 127,000 ounces sold in the prior quarter. Additionally, government mints are witnessing unprecedented demands for silver coins as a result of its price drop to a six-year low, and are even taking steps to ration the sales of silver bullion coins. It appears that someone, other than the Wall Street pundits, thinks investors should add precious metals to their portfolio when prices are cheap.

- Chinese gold imports show continued strength, as Shanghai Gold Exchange reports indicate over 800 tonnes for the third quarter alone. The Chinese government was also active during August with the purchase of about 16 tonnes of gold, likely financed with the proceeds from a record sale of $83 billion in U.S. Treasuries.

- Contrary to the majority, UBS and HSBC see gold as an excellent investment at current prices. UBS noted its belief that gold’s upside potential currently outweighs its downside risk.

Threats

- Morgan Stanley warns that commodities are set for their worst quarter since 2008 and that more losses may still be ahead. The bank cut long-term forecasts for metals by as much as 12 percent.

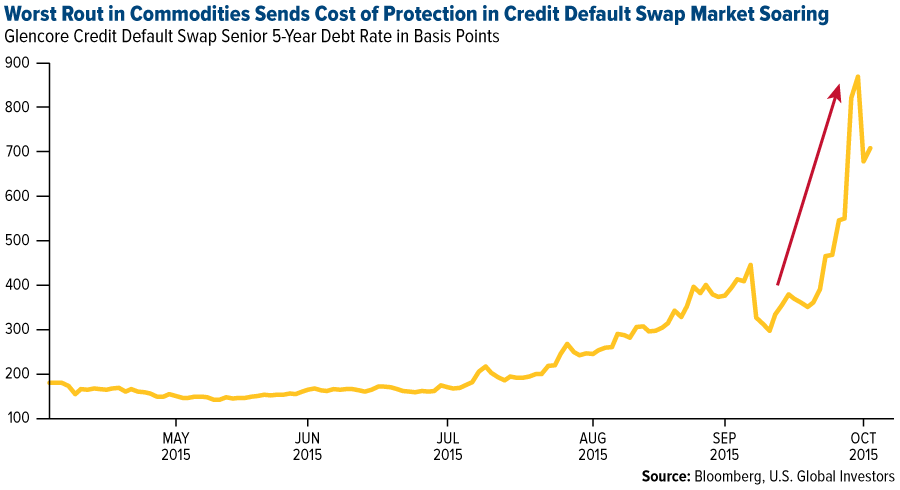

- Glencore may seek more than $1 billion in streaming deals in an effort to recover from plummeting share prices. These deals would most likely be focused on future production of gold and silver from some of its South African mines. Glencore’s share price plunged at the start of the week as analysts speculated the company could lose its credit rating.

- Swiss regulators identified seven banks that are being investigated to determine if they were involved in an effort to manipulate the prices of gold, silver and other precious metals. Although the investigation could last until 2017, it is unlikely that these banks would be prosecuted. Many of these banks have been investigated dozens of times in the past for metal price manipulation; however, none of these investigations have ever resulted in criminal prosecution or significant fines against them.

Energy and Natural Resources Market

Strengths

- Oil and gas exploration and production stocks led all natural resource sectors this week. The performance came from the combination of recovering oil prices as well as expectations for another Federal Reserve rate hike delay, following September’s disappointing unemployment report. The S&P 500 Oil Exploration & Production Index increased 5 percent this week.

- Rail stocks bounced during the week on improved investor sentiment following a Wall Street upgrade and a recovering equity market. The S&P 500 Railroad Index increased 4.6 percent this week.

- Master Limited Partnerships (MLPs) surged off of annual lows as valuations and higher dividend yields became more attractive. The Alerian MLP Index gained 3.6 percent this week.

Weaknesses

- Dry bulk shipping stocks saw profit taking after last week’s gains, as the price of iron ore into China declined following disappointing purchasing managers’ index (PMI) numbers. The Bloomberg Dry Ships Index fell nearly 5 percent this week.

- Similar to dry bulk stocks, iron and steel equities lagged natural resources due to weaker steel and iron ore prices.

- Oversupply, soft pricing and stretched balance sheets continue to pressure coal stocks. The Market Vectors Global Coal Index dropped 1 percent this week.

Opportunities

- The Department of Energy (DOE) is set to release its short-term oil outlook next week, which could show signs of declining U.S. production and continued demand strength.

- Iron ore will average $60 per barrel in 2017 and climb every year through 2020 to $75 per barrel as demand growth accelerates and supply increases slow, according to a quarterly outlook from Australia’s Department of Industry & Science.

- Russia’s energy focus towards Asia won’t be slowed by a slump in commodities and cooling economic growth in China, according to the state-run energy giant Gazprom PJSC. The world’s largest natural gas exporter sees its supply negotiations with China unaffected by the Asian nation’s falling demand this year for imported fuel.

Threats

- Weak commodity prices continue to pressure balance sheets of oil and gas MLPs. Further weakness in oil and gas prices and the limited duration of hedge books will place greater scrutiny on the ability of exploration & production MLPs to pay distributions.

- Following a recent trip to China, Wall-Street analysts came away bearish toward further industrial growth. They warned that their forecasts for GDP growth could fall in the back half of the year from 5-6 percent, to 3-4 percent.

- There are further headwinds for grain prices as old crop stocks of corn, soybeans and wheat are substantially larger than a year ago. This will add significantly to new-crop supplies, according to the U.S. Department of Agriculture’s quarterly Grain Stocks report released on Wednesday.

China Region

Strengths

- Taiwanese stocks were the best performers in the region this week, led by semiconductors. Taiwan’s manufacturing purchasing managers’ index (PMI) rose to 46.9 in September from 46.1 in August. The Taiwan Stock Exchange Weighted Index rose 2.12 percent this week.

- The Korean won was the best performing currency in the region this week as the nation’s industrial production and exports fell less than expected, paired with strengthening manufacturing PMI data. The currency appreciated 1.55 percent against the U.S. dollar this week.

- Consumer staples was the best performing sector in the region this week. The MSCI AC Asia ex Japan Consumer Staples Index rose 2.70 percent this week.

Weaknesses

- Thailand was the worst performing market in the region this week as exports contracted more than expected, while the government revised down its GPD and inflation forecasts. The Stock Exchange of Thailand SET Index fell 2.21 percent this week.

- The Thai baht was the worst performing currency in the region this week as weaker fundamental data leads investors to speculate that the government will cut rates in the near future. The currency depreciated 0.83 percent against the U.S. dollar this week.

- Telecommunications was the worst performing sector in the region this week. The MSCI AC Asia ex Japan Telecommunication Services Index fell 1.05 percent this week.

Opportunities

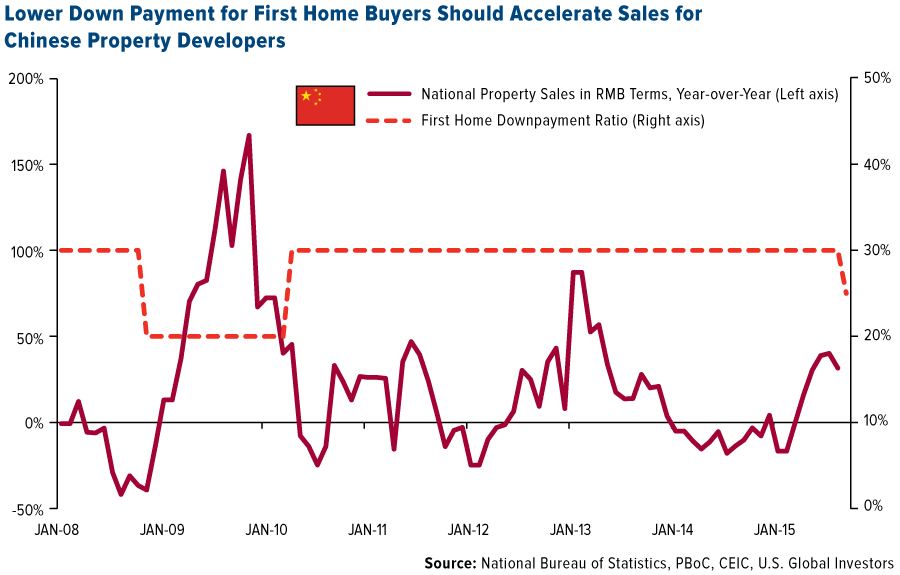

- China’s recent announcement to reduce the down payment ratio for first-time home buyers, from 30 percent to 25 percent in lower tier cities, sends yet another unambiguous government policy signal to support the property sector. This is a key lever for economic growth given its significance as a demand driver for upstream raw materials and downstream durable household goods. Enhanced housing affordability should help property developers further digest housing inventories by accelerating sales based on historical experience in China.

- China’s manufacturing PMI was better than expected for the month of September, according to official data released this week. Although the index remains under the key 50 level, it does seem to be a step in the right direction.

- Given the weak U.S. employment and wage inflation data released this week it seems less likely that the Federal Reserve will raise interest rates anytime soon. Keeping rates lower for longer should prop up emerging markets, or at least postpone any correction resulting from a rate hike.

Threats

- Macau casino operators face tangible challenges from Chinese authorities’ current efforts to stem capital flight by placing more stringent limits on bank card withdrawals in Macau, as announced this week. The latest policy change, coupled with stricter enforcement of maximum cash allowed for Chinese travelers overseas, should constitute headwinds. This is especially true for casino operators catering to mass-market gamblers from mainland China, and bodes ill for revenue trends for the gaming sector overall.

- Indonesia’s manufacturing PMI fell to 47.4 in September from 48.4 in August. The decline highlights the struggle that most emerging markets are currently facing.

- Singapore will release its advanced third-quarter GDP growth estimates next week. Analysts are expecting GDP to have risen by only 1.3 percent in the third quarter, down from 1.8 percent in the second quarter.

Emerging Europe

Strengths

- The Czech Republic was the strongest market this week, gaining 20 basis points. GDP for the second quarter was reported at 4.6 percent, stronger than prior reading of 4.4 percent. September’s purchasing managers’ index (PMI) data was reported at 55.5, well above the key 50 level that separates growth from contraction. The Czech Republic benefits from a low interest rate environment, with the main interest rate remaining at .05 percent for more than two years.

- The Turkish lira was the strongest currency this week, gaining 1.83 percent in the past five days. The lira appreciated as much as 1.2 percent on Friday after weaker job data was announced in U.S., leading investors into speculations that the Federal Reserve may delay the rate hike. Since Turkey funds its borrowing costs in U.S. dollars, a delay in U.S. rate hikes benefits the lira.

- The industrials sector was the strongest sector within the emerging European countries this week.

Weaknesses

- Greece was the weakest performing market this week. After Alexis Tsipra’s left-wing Syriza party’s second victory, Greek banks have been under pressure. The Athens Stock Exchange Index lost 5.06 percent in a week and banks on average lost 30 percent during the same period.

- The Russian ruble was the weakest currency this week, losing 96 basis points. Russia proposed an additional tax on oil producers in order to raise further revenue for the budget, pulling energy equities and the currency lower.

- In a down week, telecommunication services was the weakest sector within the emerging European countries.

Opportunities

- Mario Draghi, the European Central Bank (ECB) president, may be getting ready to expand quantitative easing (QE) in order to fight deflation. Two-thirds of economists in a Bloomberg survey this month said that the ECB will add to its 1.1 trillion euro-asset purchase plan. A majority of analysts predicted that a QE increase will be announced later this year, boosting economic growth and pushing equities higher.

- The Polish zloty’s three-month historic volatility is at the lowest rate of fluctuation among 24 of its developing peers tracked by Bloomberg. Exceptions include the Bulgarian lev, the Czech koruna and Romania’s leu, which are closely controlled by central banks. Marek Belka, governor of the National Bank of Poland, commented that the zloty has been largely immune ahead of the October 25 general election because of Poland’s “very good fundamentals.” He expects the zloty to remain more stable than other emerging currencies, besides the leu and the koruna.

- The MSCI Emerging Markets Index slid 19 percent last quarter to its lowest closing level in six years, creating a buying opportunity after the selloff.

Threats

- During the United Nations Assembly meeting in New York this week, Vladimir Putin and Barack Obama presented different approaches on how to fight the Islamic State. Putin sees Bashar al-Assad, the president of Syria, as part of the resolution to the conflict in the region, while Obama repeatedly called for an end to Assad’s rule in Syria. After the United Nations meeting, and without coordinated response to the Syrian crisis, Russia launched airstrikes in Syria. Putin’s spokesman, Dmitry Peskov, said that Russia would practically be the only country in Syria to be conducing operations “on a legitimate basis,” and at the request of “the legitimate president of Syria.”

- The euro area’s inflation rate turned negative in September for the first time in six months. Consumer prices fell 0.1 percent from a year earlier while economists were predicting an inflation rate of zero. The euro currency weakened after the consumer price index (CPI) data was released.

- Eurozone manufacturing PMI data weakened in September. The number came in at 52.0, slightly lower than August reading of 52.3. On a positive note, the data has been above the key 50 level for more than two years.

(c) US Global Investors