Sustainable Finance And Retail Investors Should Consider It By Jane Duscherer and Steven Hyland Jr.

Q2 2021 hedge fund letters, conferences and more

It has been a busy 2021 for the European Union’s push to steer the region’s and its trading partners’ economies onto a long-term sustainable path. The Eurozone, however, has not been the lone actor. Activist investors and judicial systems are pushing companies to more fully account for and report on their environmental impacts and policies for its mitigation. Furthermore, the number of investment firms publicly committing themselves to responsible and sustainable investing grows apace. Sustainable funds received more than $51 billion in new investments in 2020, doubling the previous record set in 2019. This number represented one-fourth of all new investments in 2020. Global sustainable investments under management, which amounted to $30.6 trillion in 2018, could reach as much as $53 trillion in 2025. Sustainable finance, so it seems, is on the march.[1]

As individual investors consider where to place their savings, sustainable finance will become an increasingly predominant strategy. And given the baskets of instruments and securities emphasizing environmental, social, and corporate governance (ESG) considerations grow, it strikes us as important to unpack what this approach entails, the problems it endures, and why the business case for it remains compelling.

What Is Sustainable Finance?

Sustainable finance is the steering of capital to investments that “provide environmental benefits in the broader context of environmentally sustainable development (green finance) as well as finance for education, social development, health and other aspects of sustainable development.”[2] Put another way, sustainable finance looks at the non-financial impacts and material outcomes of investments as well as its return on capital. More philosophically, it is an attempt to re-embed the financial sector into the real economy and the societies within which it operates.[3]

These non-financial considerations are framed in the ESG investment strategy. ESG, coined in 2005, includes factors ranging from climate change and resource depletion to human rights and workplace safety to bribery and corruption and executive pay. The key idea is to assess material risks a firm produces during its operations. A basic example of ESG strategy is exclusion. For instance, Norway’s sovereign wealth fund – the world’s largest – does not invest in many publicly traded companies that are extractivist and pollutive, such as mining firms Glencore and Anglo American. Exclusion made up the biggest portion of ESG investing in 2018, representing $20 trillion.[4]

Sustainable finance and ESG investment strategies are closely linked to the United Nations’ 2030 Agenda, the Sustainable Development Goals, and increasingly the 2015 Paris Agreement. Combined, these three blueprints for greater socioeconomic inclusion and stewardship of the world’s natural capital have inspired international frameworks for sustainable practices in such realms of finance and insurance as the Principles for Responsible Investing, the Principles for Responsible Banking, and the Principles for Sustainable Insurance.[5]

And while the momentum towards states, firms, and institutional and individual investors integrating ESG strategies builds, there exists a series of problems and challenges that sustainable finance must confront for it to have the impact it seeks and produce the outcomes societies demand.

The Challenges For ESG

Investing in ESG funds is not an easy landscape to navigate. One would be forgiven if they felt overwhelmed. There are lots of organisations and providers of information around ESG. TCFD, UNPI, SDGs, PSI, GRI, and the SASB are just some of the ESG-related acronyms to get one’s head around. In theory sustainability is measured by assessing the performance according to environmental, social and governance principles. The trend has been one of increased reporting by firms. In 2019, for instance, 90 percent of companies in the S&P500 index published sustainability reports, up from about 20 percent in 2011.[6]

In reality, there are many challenges to measuring the impact of sustainability, with the largest being the lack of any true global regulations or set of internationally recognized standard requirements. Currently, there is a mishmash of reporting methods filling this vacuum. Different companies will have particular requirements, discrete goals to reach, and because of this it can be confusing as to what a company is really doing to ensure they are meeting their ESG targets and requirements. Devoted climate activists and sustainability leaders have observed that measurement and reporting have become ends to themselves and devoid of the social and environmental impact they were designed to produce.

This phenomenon is known as greenwashing, a word popular in press accounts and increasingly part of the public lexicon. Greenwashing is the process of conveying a false impression or providing misleading information about how a company’s products are environmentally sound. A former ESG investment manager quipped that the rush to celebrate this surge in ESG impact disclosure and pronouncements of socially responsible investments as “greenwishing” by all parties. The former head of sustainable investment at Blackrock, the world’s largest asset management firm with more than $8 trillion worth under management, derided Wall Street’s commitment to sustainable investment as little more than a cynical public relations campaign.[7]

The tension between the increasing demand for sustainable investments and the distance yet to travel to discern between sustainable and unsustainable investments continues to mount. That the EU, the UK, and Singapore, for instance, have each produced so-called green taxonomies signals two critical realities. First, moves by regulatory agencies to give structure and shape to ESG marks a realization that this investment strategy is here to stay and urgently so. Second, there needs to be internationally co-ordinated guidance for national governmental regulation to standardize and make transparent the field of sustainable investible products for investors.[8]

Greenwashing and the hodgepodge of regulatory guidance and frameworks illustrates the importance of the European Union’s adoption of a first set of policies in early July outlining green investments, permitting producers of renewable energy, rechargeable batteries, low-emission automobiles, and energy efficient equipment to earn a “green” credential. Given that the EU is home to half a billion people with a nearly $6 trillion market capitalization of listed domestic companies in 2018, the moves to define and standardize sustainable finance will set the terms of the debate among sovereign states and empower the work of such non-governmental institutions as the International Organization of Securities Commissions (IOSCO) and the University of Cambridge Institute for Sustainability Leadership (CISL).[9]

This importance is further underlined by the significant increase in the issuance of green bonds and loans, surpassing US $500 billion in April; a result in part to the EU’s efforts to deliver on their objectives under the European Green Deal and commitments to climate and sustainability objectives. Investor demand is set to push green bonds issuances past $1 trillion this year. Furthermore, the increase in borrowers looking to change how they do business and to put ESG considerations and initiatives to the forefront of their business adds to the momentum.[10]

The Business Case For Sustainable Finance

These significant challenges notwithstanding, the fact remains that a strong business case exists for ESG investment strategies. And the pool of investible securities will only continue to grow, giving investors ample opportunities to have a positive impact while achieving their risk-adjusted return targets. The European Union sees a need for $415 billion per year in green energy investments alone through 2030 and some analysts estimate that emerging markets green bond issuance could reach $100 billion annually by 2023. All told, an astonishing $3.2 trillion in private investment is needed annually to fund renewable energy projects globally, according to the UN’s International Renewable Energy Agency.[11]

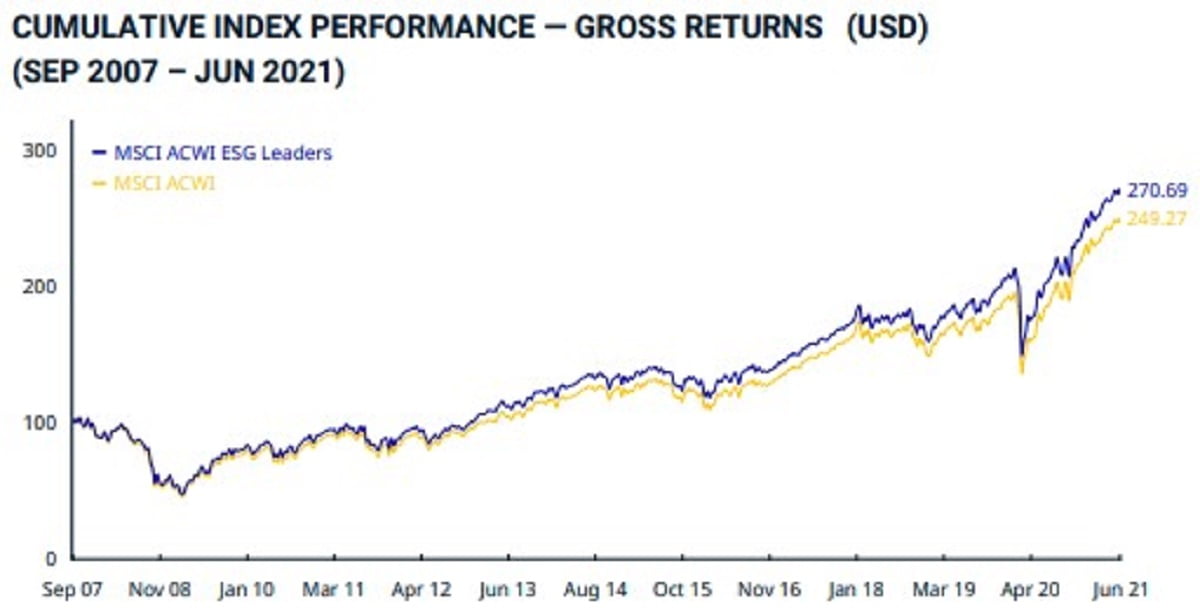

Opportunity, thus, abounds and the numbers increasingly prove the case. ESG-weighted government bonds in emerging markets have outperformed unweighted ones in 2021. MSCI’s ACWI ESG securities index exceeded its sister index ACWI between September 2007 and June 2021, averaging an annualized 7.50 percent rate of return to 6.86 percent. The ACWI ESG is a capitalization weighted index featuring securities of mid- and large-cap firms from 23 developed markets and 27 emerging markets that have scored high on ESG performance metrics. The ACWI is MSCI’s “flagship global equity index” consisting of nearly 3,000 firms across 11 sectors that account for roughly 85 percent of the free float-adjusted market capitalization in each market.[12] Put another way, the increasing weight of evidence is demonstrating that there is no discount to the ESG investment strategy.

Source: MSCI.com

Individual investors should neither fear nor shy away from ESG. The rules will gain clarity, regulators and investors will come to penalize greenwashers, and an intelligible market of sustainable investments will only grow in size and diversity. The moment for responsible and sustainable investments is at hand.

Over a career spanning 30 years, Jane Duscherer has utilized her strong understanding of financial markets, credit risk, technology and infrastructure to meet clients’ needs, most recently as Director of Product Management at IHS Markit. Steven Hyland Jr., Ph.D. teaches in the Department of History and Political Science at Wingate University. Please connect with Jane and Steven on LinkedIn.

This article is the first in a series examining sustainable finance and ESG investing for individual investors.

[1] Jennifer Hill and Svea Herbst-Bayliss, “Exxon loses board seats to activist hedge fund in landmark climate vote,” Reuters, 26 May 2021, https://www.reuters.com/business/sustainable-business/shareholder-activism-reaches-milestone-exxon-board-vote-nears-end-2021-05-26/; “Shell: Netherlands court orders oil giant to cut emissions,” BBC, 26 May 2021, https://www.bbc.com/news/world-europe-57257982; Alicia Adamczyk, “Sustainable investments hit record highs in 2020 – and they’re earning good returns,” CNBC, 11 February 2021, https://www.cnbc.com/2021/02/11/sustainable-investments-hit-record-highs-in-2020.html; “ESG assets may hit $53 trillion by 2025, a third of global AUM,” Bloomberg Intelligence, 23 February 2021, https://www.bloomberg.com/professional/blog/esg-assets-may-hit-53-trillion-by-2025-a-third-of-global-aum/. [2] Jeremy McDaniels and Nick Robins, Greening the Rules of the Game: How Sustainability Factors Are Being Incorporated into Financial Policy and Regulation, Nairobi: UNEP Inquiry, May 2018. [3] Jürgen Kocka, Capitalism: A Short History (Princeton: Princeton University Press, 2016), 114-124. [4] Georg Kell, “The Remarkable Rise of ESG Investing,” Forbes.com, 11 July 2018, http://www.georgkell.com/opinions/https/wwwforbescom/sites/georgkell/2018/07/11/the-remarkable-rise-of-esg/3dd3f3501695; Gwladys Fouche and Terje Solsvik, “Norway wealth fund blacklists Glencore, other commodity giants over coal,” Reuters, 12 May 2020, https://www.reuters.com/article/us-norway-swf/norway-wealth-fund-blacklists-glencore-other-commodity-giants-over-coal-idUSKBN22P05Y; “ESG assets may hit $53 trillion by 2025, a third of global AUM,” Bloomberg Intelligence, 23 February 2021, https://www.bloomberg.com/professional/blog/esg-assets-may-hit-53-trillion-by-2025-a-third-of-global-aum/. [5] See United Nations Environment Programme – Finance Initiative, https://www.unepfi.org/. [6] Dieter Holger and Fabiana Negrin Ochoa, “Companies Grapple With Sustainability Data,” The Wall Street Journal, 13 October 2020. [7] David O’Mahoney and Annual Awan, “ESG Greenwashing and the EU Taxonomy Regulation Part 1 – Greenwashing, what is it?,” Lexology, https://www.lexology.com/library/detail.aspx?g=432ab313-01d1-4020-ac28-b41df8f3caaa [Accessed 12 July 2021]; Kenneth P. Pucker, “Overselling Sustainability Reporting,” Harvard Business Review, May-June 2021, https://hbr.org/2021/05/overselling-sustainability-reporting; Tariq Fancy, “Financial world greenwashing the public with deadly distraction in sustainable investing practices,” USA Today, 16 March 2021, https://www.usatoday.com/story/opinion/2021/03/16/wall-street-esg-sustainable-investing-greenwashing-column/6948923002/ [8] Natasha Teja, “Sustainable disclosure struggles with global harmonisation,” IFLR, 6 July 2021, https://www.iflr.com/article/b1sjc4b1353xpk/sustainable-disclosure-struggles-with-global-harmonisation; Max Krahé, “For sustainable finance to work, we will need central planning,” Financial Times, 11 July 2021, https://www.ft.com/content/54237547-4e83-471c-8dd1-8a8dcebc0382; Jill Ward, Silla Brush, and John Ainger, “Why EU Climate Weapon Is in the Financial Fine Print,” Washington Post, 6 July 2021, https://www.washingtonpost.com/business/energy/why-eu-climate-weapon-is-in-the-financial-fine-print/2021/07/06/b7e85b9a-de66-11eb-a27f-8b294930e95b_story.html. [9] Huw Jones, “EU turns to finance to achieve climate neutral continent,” Reuters, 6 July 2021, https://www.reuters.com/business/environment/eu-harnesses-finance-create-climate-neutral-continent-by-2050-2021-07-06/; Mark Segal, “IOSCO Outlines its Vision for Sustainability Disclosure,” ESG Today, 28 June 2021, https://www.esgtoday.com/iosco-outlines-its-vision-for-sustainability-disclosure/; See among the rich resources at CISL, University of Cambridge Institute for Sustainability Leadership (CISL), Rewiring the Economy: Ten tasks, ten years, July 2015; updated 2017, November, https://www.cisl.cam.ac.uk/resources/cisl-frameworks/rewiring-the-economy. [10] Liam Jones, “Europe reaches $500bn in green investment – Climate Bonds Market Intel Reports, Climate Bonds Initiative, 17 May 2021, https://www.climatebonds.net/2021/05/europe-reaches-500bn-green-investment-climate-bonds-market-intel-reports; David Caleb Mutua, “ESG Bond Sales Sprint to $1 Trillion as Investors Force Change,” Bloomberg, 13 July 2021, https://www.bloomberg.com/news/articles/2021-07-13/esg-bond-sales-sprint-to-1-trillion-as-investors-force-change. [11] John Ainger and Ewa Krukowska, “EU Targets Finance for $415-Billion-a-Year Green Transition,” Bloomberg, 6 July 2021, https://www.bloomberg.com/news/articles/2021-07-06/eu-targets-finance-to-fund-415-billion-a-year-green-transition; John Pieere Lacombe, “EM green bond issuance forecast to cross $100bn in 2023,” Environmental Finance, 20 April 2021, https://www.environmental-finance.com/content/news/em-green-bond-issuance-forecast-to-cross-$100bn-in-2023.html; Anthony Di Paola, “‘Decisive’ Decade in Climate Change Fight Needs Lending Surge,” Bloomberg, 30 June 2021, https://www.bloomberg.com/news/articles/2021-06-30/-decisive-decade-in-climate-change-fight-needs-lending-surge. [12] Leo Laikola and Hanna Hoikkala, “ESG Investors Turn to Emerging Markets, Defying Skeptics,” Bloomberg, 16 May 2021, https://www.bloomberg.com/news/articles/2021-05-16/-esg-provokes-laughter-and-nightmares-as-funds-tap-new-markets; “ACWI,” MSCI, https://www.msci.com/acwi [Accessed 13 July 2021]; “MSCI ACWI ESG Global Leaders Index (USD),” MSCI, https://www.msci.com/documents/10199/9a760a3b-4dc0-4059-b33e-fe67eae92460 [Accessed 13 July 2021].