Starvine Capital Corporation investment commentary for the second quarter ended June 30, 2018.

Q2 hedge fund letters, conference, scoops etc

Overview

- Q2 2018: A ‘One-Off’ Quarter

- Peak Buybacks: The Perfect Contra-Indicator?

Dear Starvine Capital Client:

In Q2 2018, accounts open and fully invested in the Starvine Flagship Strategy since the beginning of the quarter increased 15.5% – 15.6%, while fully-invested accounts in the Mid-Large Cap Strategy increased 13.7% – 13.8%. During the quarter, the S&P TSX Total Return Index increased 6.8% and the S&P 500 Total Return Index increased 5.5% in Canadian dollars (3.4% in USD). The share prices of certain holdings common to both strategies advanced significantly, which can be attributed to quarterly earnings results that exceeded consensus expectations, in addition to a rebound effect that happened off of a general decline in equity markets in the closing weeks of Q1.

Currency again had a moderately positive impact on results. I estimate the 1.9% appreciation of the U.S. dollar in Q2 aided performance by approximately 1.3% and 0.8% for Flagship and Mid-Large Cap, respectively.

Last quarter, I wrote about how the lollapalooza effect had an outsized impact on Graftech’s business results. In Q2, the Starvine strategies benefitted from a ‘baby’ lollapalooza effect in that the confluence of different factors contributed to a one-off type result. Although I spend considerable time reviewing quarterly earnings results and conference calls, there is an inherent randomness in a company’s business results between any three-month reporting period. So when several holdings in different industries all happen to have a strong earnings quarter – and the exchange rate goes the right way again – I realize the chance of a similar result in the near future is slim.

Trading in the Starvine strategies has been close to non-existent in 2018. As I stated last quarter, certain positions will need to be rebalanced for risk management reasons. I came close to rebalancing the outsized positions on numerous occasions during the quarter, but ultimately held back because valuation on those names was sufficiently attractive (even after the run-up) such that I elected to let the ‘absolute max weight’ risk control rules trigger the selling. My self-imposed rule is to sell a minimum of 25% of a position that crosses the max threshold for any single holding.

This is the last letter to be published on a quarterly basis, as explained in Q1. I will write these letters semi-annually following the second and fourth quarter of each calendar year. However, each client will continue to receive customized emails every quarter, along with the performance statements.

Outlook – Contra-Indicators Unite

In previous quarters, I discussed indicators that paint a challenging long-term picture for equities. I wrote about the Shiller P/E ratio hovering near all-time highs and the irrefutable reality that the attraction of equities must lessen with increasing interest rates.

Another telling contra-indicator in the media recently is the heightened level of share buyback activity. To review, a share buyback (a.k.a. share repurchase) occurs when a company buys its own shares and then cancels them, thereby reducing the overall number of shares. Each remaining shareholder is therefore entitled to a larger percentage of profits. For example, if a company has 100 shares and buys back half of them, there will be 50 shares remaining. If, for simplicity’s sake, the company earns $100 per annum, each share now earns $2 ($100/50) vs. $1 ($100/100) before the buyback. All else being equal, higher earnings per share should equate to a higher share price.

Share buybacks can be very beneficial to shareholders, but only on condition that the shares are repurchased at a discount to intrinsic value. So why is it that share buybacks tend to spike up near market peaks? On the surface, it seems silly to suggest that CEOs have more courage to repurchase when share prices are expensive and clam-up when conditions to buy-back are most favorable, which is when prices are low.

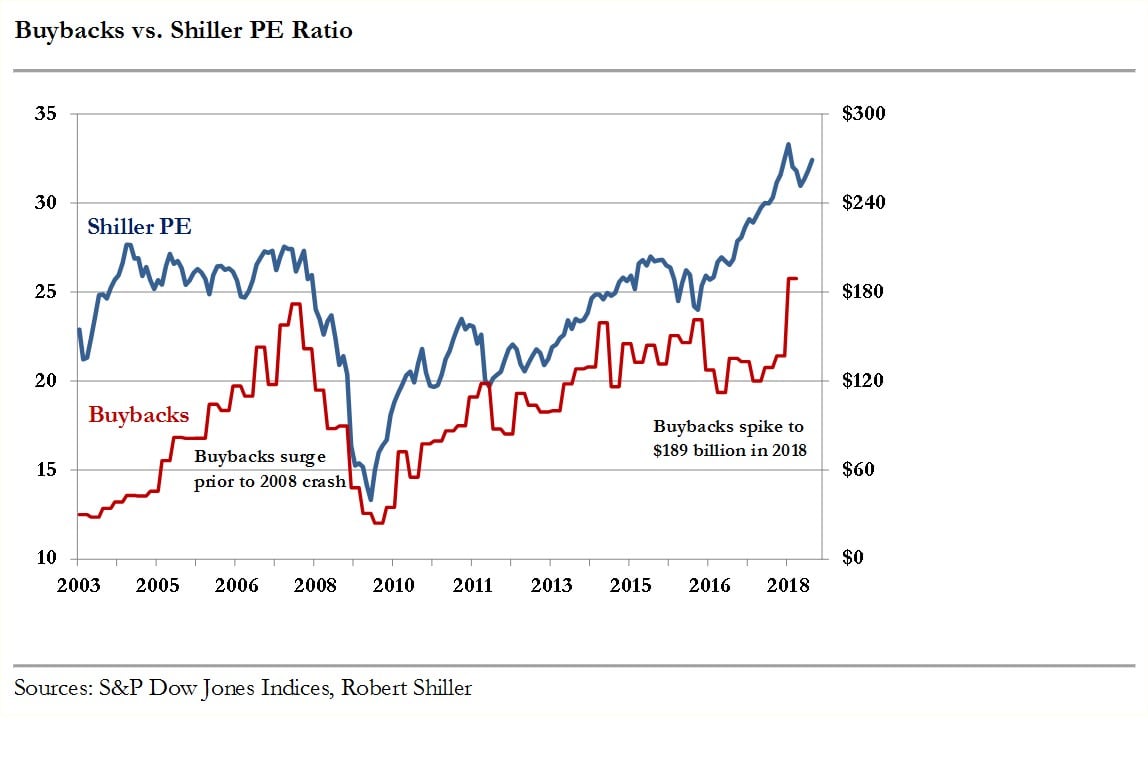

Below, I superimpose buyback activity in the S&P with valuation (Shiller PE ratio) dating back to 2003. It is clear that buybacks climaxed just in time for the 2008 market crash. And now, after nearly a decade of bull markets, we are witnessing a renewed surge in repurchases.

Share buybacks reached $189 billion in Q1 of 2018, the most recent data point available. The stars are lining up in the exact opposite positioning of what a typical value investor would like to see. A key thing for fund managers to remain cognizant of when reviewing portfolio holdings is companies that (a) are trading at a full or lofty valuation, and that (b) have heightened their spend on repurchasing shares. Such a combo may result in a double-whammy: the stock eventually plummets from multiple contraction, and moreover the company is not able to capitalize on opportunities in a down market due to having exhausted all its financial dry powder (i.e. increasing debt or spending its cash before the crash to repurchase shares).

And yet I am excited as ever about the stocks I own and their ability to generate sound long-term returns. My positivity is built from a brick-by-brick, bottom up view of the companies I have chosen and their market prices relative to values, both now and where I see the values growing years out. But such is the advantage of investing in a portfolio of securities truly constructed on a bottom up basis. It may not result in less volatility, but “driving manual” so to speak improves the quality of my sleep because I consciously avoid subjecting my clients’ capital to overpriced stocks, and moreover to companies that are behaving irrationally with their capital. On the contrary, an index approach just buys a basket of stocks representative of the market and thus makes no attempt to guard against overvaluation.

Sector Breakdown

Markets remain expensive, but even in this environment where the high level indicators do not appear favorable, there is value to find if one cares to look just one layer beneath the surface. Certain sectors are indisputably out of favor, clearly out of synch with indexes trading near all-time highs. At the end of the day, I don’t care whether a stock is in favor or out of favor; what matters is that the company checks the boxes as a vehicle to compound capital over the long term, and moreover that the stock is priced such that a compelling return is likely to be realized.

Sincerely,

Steven Ko

Portfolio Manager