The Broad Market Index was down 0.51% last week and 51% of stocks out-performed the index.

Q2 2021 hedge fund letters, conferences and more

This is the last update for financial statements from U.S. companies for the second quarter of 2021. Quite a remarkable juxtaposition to the implosion of sales that the virus brought on us last year.

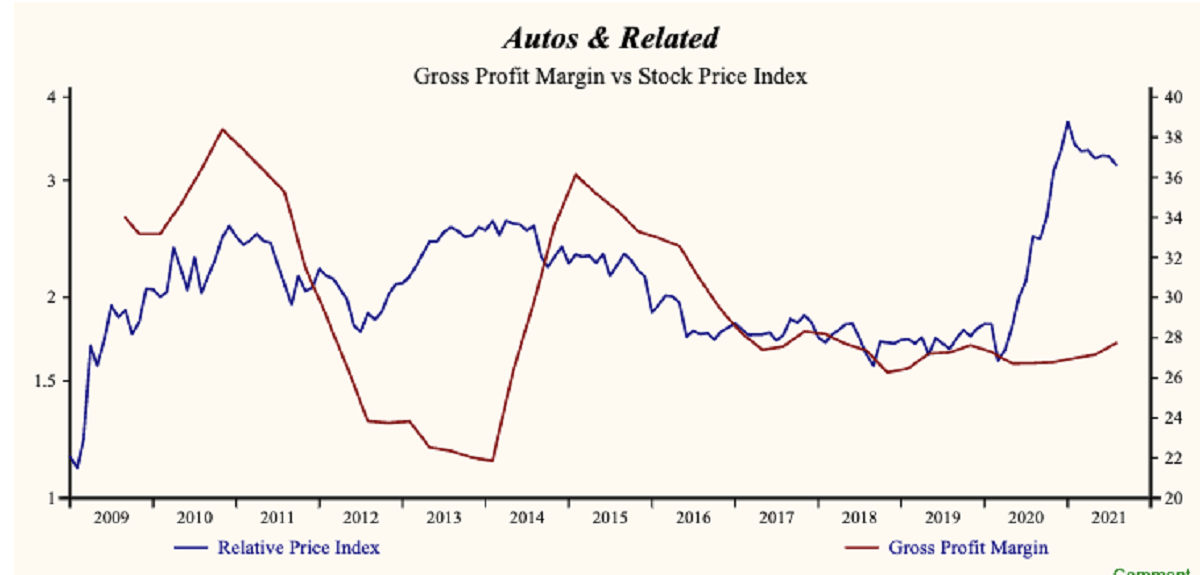

Strong Autos & Housing

Corporate growth has been invigorated by the ultra-loose money policy that has been prescribed as the solution to the virus crisis. Today’s financial data reveals that, behind the wave of improvement, is a strong automobiles and housing industry.

The autos and housing increase in sales growth is now spilling over, as it eventually does, to the broader industrial and commodity sectors. This sales growth uptrend is now in its 3rd quarter. These loose-money-driven consumer cycles have been seen and repeated over the last 60 years. Quantitative tools and active management such as Otos.io can predict how they end.

Cycle Peak

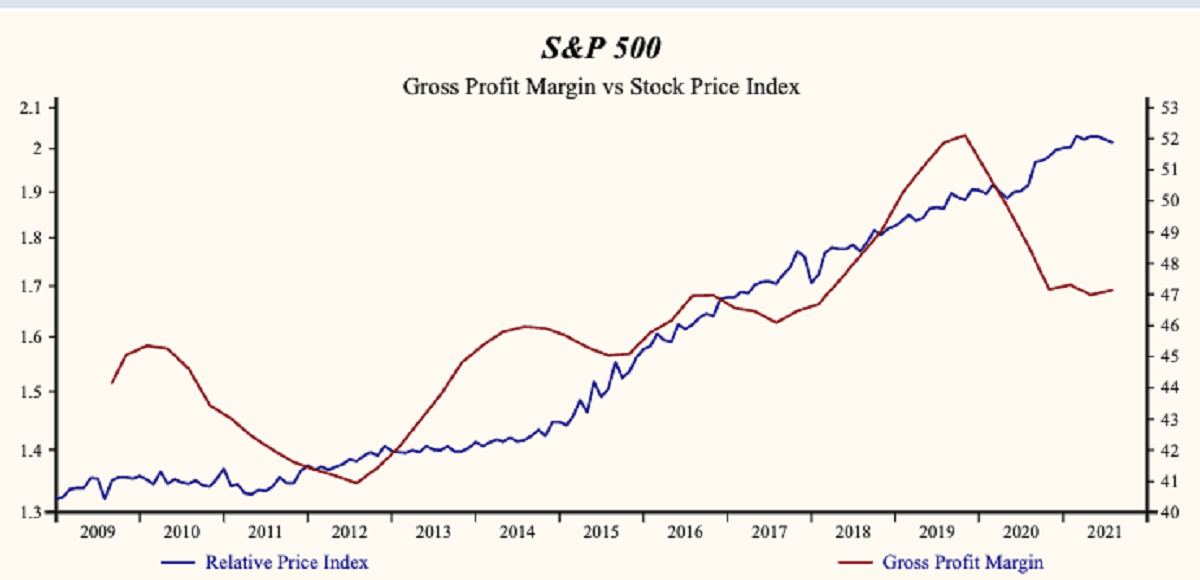

A clear sign of a cycle peak is marked by higher inventories and lower gross profit margins; the cycle is 8 to 10 quarters from trough to peak.

The wave of new financial statements for the 3rd quarter is just over the horizon. History shows that a broad industrial recovery is not fragile and takes a tighter monetary policy (less money available to lend and higher interest rates) to slow it down.

Sales Growth Predicted To Fall

The new wave of company numbers that Otos will sort through and analyze in the coming weeks will continue to show the effect of the virus impact last year. Sales growth is likely to fall from near the highest level ever. The critical and most predictive variable is the gross profit margin.

Gross Margin Distortion

The average gross margin decline in the recent quarter is a direct distortion from the virus. Companies in industries where the virus impact was most severe, industries such as airlines, leisure time and entertainment and gaming and lodging, all recorded margin declines steep enough to bring the average down even though 61% of companies accounting for 72% of market capital are achieving a gross profit margin improvement in the recent period.

Rising profit margins boost the cash flow effect of an improvement in sales growth and indicates that the company can increase output prices at a faster rate than input costs. This is critical to success in an economy with rising commodity prices and rising labor costs.

Portfolio Risk

The big risk is in the structure of popular indexes that form the basis for most ETFs and mutual funds that investors currently own. A very small number of jumbo companies have come to dominate the indexes after years of improving growth driven by higher-than-average sales growth and persistent margin improvements.

Profit-Margin Trend Is Key

With the broad acceleration elsewhere, the dominant growth companies already show declining relative growth.

Otos identifies decelerating companies “Sell MoneyTrees” with a red stem (even high and falling sales growth is a very negative attribute), a brown globe (falling profitability) and a trim red pot (falling profit margins and no operating/financial leverage).

Review your portfolio for these financial attributes and since the stock prices of these companies are currently and broadly extended now this a fantastic opportunity to sell growth and buy cyclicals.