This article was originally posted on SeekingAlpha (August 17th, 2011) by Andrew Shapiro. Andrew is PM of Lawndale Capital Management, an investment advisor that has managed activist hedge funds focused on small- and micro-cap companies for over 18 years. His full profile and archive of articles can be found here.

A movie theater operator/owner and real estate developer, Reading International (NASDAQ:RDI, RDIB), (highlighted in this Just One Stock interview and these other Seeking Alpha articles) recently released itssecond quarter June 2011 results, in which Reading’s overall cinema revenue growth of 18.7% y/y bested all three of the larger US public theater exhibitors.

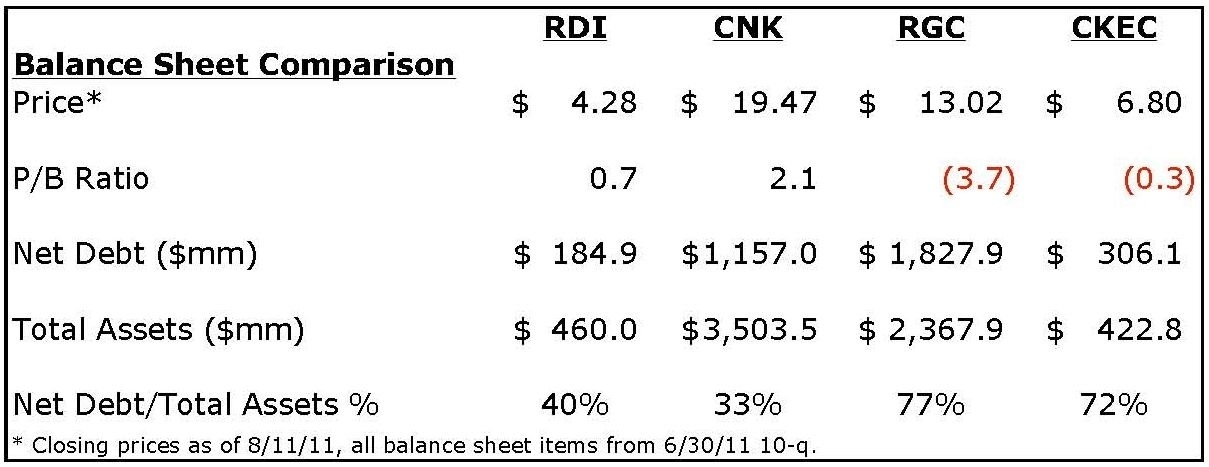

Furthermore, Reading’s stock price trades at the biggest discount to book value/share of all these public cinema operators. This book value is greatly understated due to substantial unrealized appreciation in Reading’s sizable real estate holdings. Together, these factors make Reading a compelling risk/reward investment. Reading’s detailed 10-Q for this quarter can be found here and certain salient findings of this filing are discussed, below.

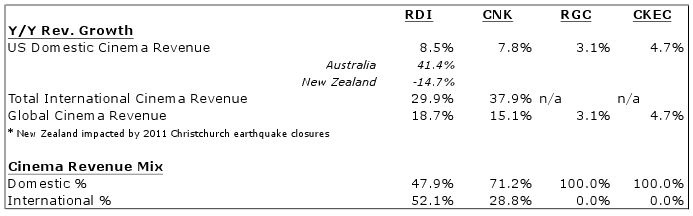

Box office results for Q2 2011 improved over the prior year industry-wide. Revenue growth at movie exhibitors with international operations such as Reading and Cinemark Holdings (CNK) continued to exceed exhibitors who rely solely on the US domestic market, like Regal Cinemas (RGC), and Carmike Cinemas (CKEC). This quarter’s faster international growth was a function of attendance growth and increases in average ticket prices, in addition to the foreign currency gains that have fueled past quarters.

While Reading’s Q2 domestic cinema revenue growth of 8.5% y/y was impressive and the best among these four companies, it was Reading’s substantial mix of international screens and its tremendous revenue growth in its Australian market (+41.4% y/y) that gave Reading its leading revenue growth rate among these four companies.

Q2 2011 y/y public movie exhibitor revenue comparisons are highlighted below (click to enlarge images):

Here is a summary of salient points from Reading’s 2nd quarter results:

- Reading International had strong Q2 y/y growth in both revenues and operating EBITDA. Both of Reading’s segments, cinema and real estate, contributed to total Q2 revenue growth of 17.7% from the prior year. Revenues of Reading’s larger cinema segment, which produces the bulk of the company’s cash flows, grew 18.7% y/y, while its smaller real estate segment revenues grew 5.8% y/y. Reading’s cinema segment revenue growth was the result of sizable attendance growth in both the US and Australia and increases in Australian average ticket prices, in addition to foreign currency gains against the US dollar.

- Operating Income (EBIT) of $7.3MM was 38.8% higher than the prior year’s Q2. Q2 2011 operating EBITDA (Operating Income + Depreciation + Amortization) of $11.6MM jumped 90.5% higher than 2010 Q2 operating EBITDA of $6.1MM. Reading’s cash flow growth came from both cinema and real estate segments. Reading’s cinema segment growth would have been even higher but for continued theater closures in Christchurch, NZ due to earthquake damage. The insurance recovery for the earthquake damage and business interruption has yet to be determined or included in Reading’s financial results. This contingent asset continues to grow while the theater and The Palms shopping center, where Reading’s large multiplex in Christchurch is located, remain closed.

- Operating margins jumped from the prior year, benefiting from operating leverage on fuller theaters, higher ticket prices and increased revenue mix from concessions, which carry much higher margin than admissions.

- The box office release schedule for the remainder of the year and into 2012 contains several well-known ‘franchise’ blockbusters and a high number of 3D movies.

- Reading’s book value per share grew 60% y/y to $6.03/share – on top of last quarter’s +20% y/y growth. As explained in this Just One Stock interview, Reading’s book value greatly understates the current fair market value of the company’s Australian, New Zealand, New York and Chicago real estate, much of which has appreciated in value over more than a decade of ownership, from population growth, up-zoning, and in some instances, successful development into rent-generating shopping centers and office buildings.

The table below illustrates that Reading’s stock price trades at the biggest discount to book value of all the public cinema operators. Reading’s net debt to total assets perecentage is amongst the industry’s most conservative and much safer than Regal Cinemas’ and Carmike Cinemas’ high leverage ratios. In fact, Regal and Carmike both have negative book value from sizable past losses, restructurings and distributions in excess of income. However, what makes the table below so compelling is that Reading’s true asset and book value is likely even higher because of sizable unrealized appreciation on the company’s real estate.

10-Q real estate disclosures and Reading’s annual meeting presentation:

- Part of Reading’s stock price stagnation reflects the lack of disclosed progress in its goal to monetize its most valuable undeveloped property, the 51-acre Burwood Square development parcel [PDF] in Melbourne Australia. As described in this May 23, 2011 articlereporting on Reading’s 2011 annual meeting, the company has decided that separately monetizing the parcel’s three zoned segments in a staged manner rather than all at once is more likely to maximize the parcel’s value (see this Burwood Square property diagram, presented at its May 2011 annual meeting, showing each of the residential [green], residential/commercial [blue], and retail [yellow] zones). The selling delay partly stems from this change in monetization approach.

With this change selling approach, footnote 6 of Reading’s10-Q for Q2 disclosed an accounting reclassification of the Burwood property from a “current asset – held for sale” back into a long-term asset that was required by GAAP because too much time had passed without an acceptable firm commitment from a buyer. The footnote also supported that Reading still aimed to sell much of the parcel and that, “based on recent valuations”, Reading believes “the fair market value of the property less costs to sell is greater than the current carrying value” of $55.9 million (AUS$52.1 million.)In fact, in a May 24, 2011 press release that Reading issued as a result of disclosures at its annual meeting, (see also the Burwood Square property diagram), it was disclosed that CBRE valued the 31- to 34-acre residential [green] zone at AUS$1.7MM/acre and the 6+ acres of the residential/commercial [blue] zone at AUS$11.5MM. The final approximately 11-acres is slated to be an entertainment and retail zone [yellow] that Reading will develop directly either on its own or in JV. It should be noted that Reading’s valuable Burwood parcel remains completely mortgage free. Thus, sales proceeds would provide additional debt reduction and capital to develop the property’s [yellow] entertainment and retail zone. - In addition to pursuing the sale of most of Reading’s Burwood parcel, there is substantial activity taking place on several of Reading’s other major developable parcels (see the March 2011 Seeking Alpha article entitled “Reading International: There’s More Popping Than Just Corn”). As discussed at Reading’s May 2011 annual meeting and summarized in its May 24, 2011 press release, Reading has received offers and proposals for the potential sale or JV of both its Cinema 123 and Union Square theaters in New York City. Note also that in this quarter’s 10-Q, Reading has now listed its Lake Taupo (NZ) property and its Taringa (Brisbane, Aus) property as held for sale.

Other 10-Q disclosures of note:

- Reading increased its substantial liquidity during the quarter. At June 30, 2011, Reading had cash and marketable securities of $43.8MM plus a combined $23.2MM of availability on its several lines of credit. Subsequent to the quarter end, Reading paid down the revolver of its Australian loans by $9.9MM to a zero balance on August 2, 2011.

- Reading sold its 66.67% ownership interest in a Melbourne 5-plex to its JV partner for >15X multiple to the theater’s 2010 annual net income, generating $1.9MM in proceeds and a $1.7MM gain on sale.

- Reading’s improved prospects of sustained future Australian profits triggered a reduction in the valuation allowance and recognition of some deferred tax assets related to Reading’s sizable net operating loss tax carry forwards (“NOL’s”). At December 31, 2010, Reading had $58.5MM and $17.5MM, respectively, of Australian and New Zealand NOLs that don’t expire, and $26.5MM of US NOL’s expiring in 2025 and thereafter.

- Reading has entered into an agreement to purchase an established 17-plex in California.

- During Q2, Reading bought back 22,300 shares for a cost of $111,000 or an average of $4.98/share. Note that in 2010 Reading bought back 62,375 shares at an average cost of $4.02/share.

Trading at a substantial discount to a book value greatly understating the value of its sizable real estate holdings, Reading International’s favorable movie exhibition growth profile and conservative balance sheet make for a compelling risk/reward investment.

Disclosure: Funds I manage are long RDI, RDIB. These funds or its affiliates may buy or sell securities of this issuer at any time.

{kind=link}

{kind=link}