H/T to Joe Koster of http://www.valueinvestingworld.com/ for the great find:

A Primer on Scion Capital’s Subprime Mortgage Short, By Michael Burry. November 7, 2006

If you do not know who Burry is, do yourself a favor and read the masterpiece.

by Michael Leiws, The Big Short: Inside the Doomsday Machine

A Primer on Scion Capital’s Subprime Mortgage Short

Subprime mortgages, typically defined as those issued to borrowers with low credit scores, make up roughly the riskiest one third of all mortgages. The vast majority of these mortgages fall well within the loan size limits set by Fannie Mae and Freddie Mac, but are not deemed eligible for purchase by these two mortgage giants for other reasons.

That is, they are non-conforming. For these non-conforming subprime mortgages, the originator can certainly choose to hold onto the mortgage and retain credit risk in exchange for the interest payments.

Alternatively, the originator can sell subprime mortgages into the secondary market for mortgages. This secondary market is vast and deep thanks to the invention of mortgage-backed securitizations back in the 1970s.

In a securitization, a finance company buys up mortgages from the original lenders and aggregates these mortgages into large pools, which are then dumped into a trust structure. Each trust is divided into a set of tranches, and each tranche is defined and rated by the degree of subordination protecting the tranche’s principal from loss.

The tranches are then sold in the cash market to fixed income investors by a placement agent – typically a well-known securities dealer. The lower-rated tranches may not be offered to investors, but may be retained by the finance company.

Too, the dealer placing the securities with investors may choose to purchase some of these securities for its own account, either as an investment decision or to help ensure a full sale of the deal.

At the time of the creation of the trust, a servicer, also rated by the agencies, is hired to administer the mortgages within the trust. The trustee will manage the trust and all relations with investors, including monthly reports. The month’s end is typically the 25th.

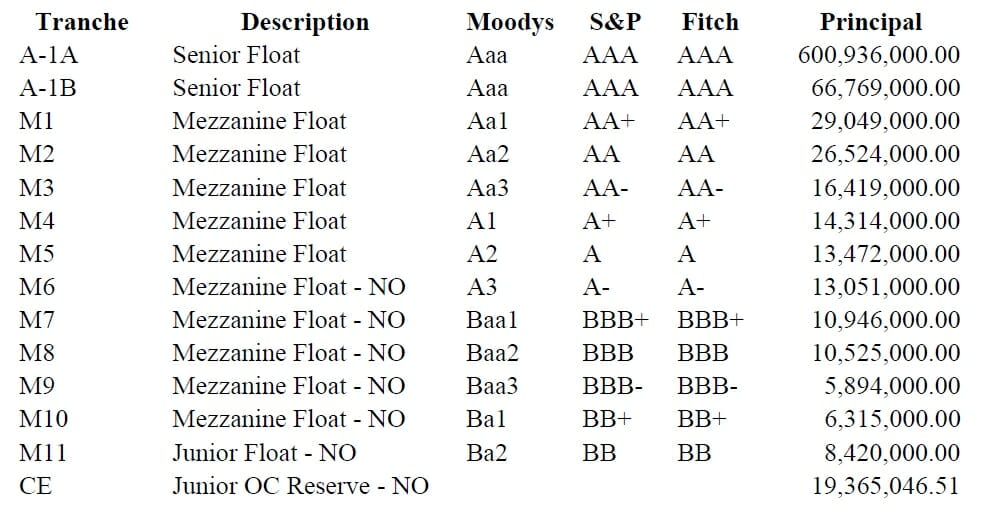

For instance, we can take a look at PPSI 2005-WLL1, an early 2005 mortgage deal.

Here, it happens that Argent Mortgage Company and Olympus Mortgage Company separately originated a set of subprime mortgages, and each sold these mortgages to Ameriquest Mortgage Company.

Ameriquest, which will be the seller in this deal, deposited these mortgages with a wholly owned subsidiary, Park Place Securities 1Incorporated – PPSI. Park Place is therefore the depositor. Park Place refashioned this pool of mortgages into a trust, with Wells Fargo Bank being the trustee and Litton Loan Servicing being the servicer as set out in the Pooling and Servicing Agreement, or PSA.

The Seller hired Merrill Lynch as the placement agent to sell the deal to investors. Those tranches designated “NO” were not offered to investors but rather retained by Ameriquest for other purposes. An investor buying a tranche will receive LIBOR plus a fixed spread that correlates with the tranche’s rating and perceived safety.

Note the senior tranches, designated A-1A and A-1B, make up 79% of this particular subprime pool. That is, these senior tranches can count on credit support amounting to 21% of the pool as well as any additional credit support that builds up during the life of these tranches.

If the pool experiences write-downs in excess of the credit support for the senior tranches, then the senior tranches will suffer erosion of their principal. This is deemed extremely unlikely by the ratings agencies, and these senior tranches therefore garner the AAA rating.

The mezzanine tranches in this pool include all those tranches that are rated, but not rated AAA. For the lowest rated tranche – M11 in this particular pool – credit support is just 2.3% at origination. Baa3, or equivalently BBB-, is considered the lowest “investment grade” rating, and the lowest investment grade tranche in this PPSI deal is M9, which had 4.05% in credit support at origination.

Note the M9 tranche is just under $6 million in size, less than 1% of the original deal size – these are tiny slices of a large risk pool. Still, the ratings agencies say each tranche is worthy of a difference in the rating due to the historically very low rate at which residential mortgages actually default and produce losses.

Because home prices have been rising so steadily for so long, troubled homeowners have been able to refinance, take cash out, and often reduce the monthly mortgage payment simultaneously.

This has had the effect of reducing the rate of foreclosures. Also because of rising home prices, foreclosures have not resulted in enough losses to counteract the credit support underlying mortgage-backed securities. To be perfectly clear, write-downs occur when realized losses on mortgages within the pool overwhelm the credit support for a given tranche.

Credit support is therefore a key feature worthy of more attention. A tranche will not experience losses if any credit support for the tranche still exists.

In addition to the structural subordination that contributes the bulk of credit support, finance companies build in overcollateralization – essentially, throwing more loans into the pool than necessary to meet the payment obligations of the pool – and the trust itself can engage in derivatives transactions to insure the pool against loss.

An example might be an interest rate swap that produces excess cash for the pool as rates rise. Over the first couple of years, which are typically relatively problem-free for mortgages, one already normally sees an increase in credit support for all tranches.

In an era of hysteria over a home price bubble, one would expect that the organizer of a new mortgage pool would include or extend use of these extra protections to help further bolster the credit support for the pool’s tranches.

As 2005 came to a close, this is exactly what happened, and this is why I find many more recent deals much less attractive from a short’s perspective than mid- 2005 deals.

As is always the case, timing is therefore important for an investor short-selling tranches of mortgage-backed securities. Catching a peak in home prices before it is generally recognized to be a peak would be critical to maximizing the chances for success.

Now, because the more subordinate tranches are so wafer thin, they are typically placed with either a single investor or very few investors. Securing a borrow on such tightly held subordinate tranches would be difficult, and as a result shorting these tranches directly is not terribly practical. A derivative method was needed – enter credit default swaps on asset-backed securities.

Credit default swap contracts on asset-backed securitizations have several features not common in other forms of swap contracts. One feature is cash settlement. Again, examining PPSI 2005-WLL1 M9 – the BBB- tranche – we see it has a size of $5,894,000.

Because credit default swaps on mortgage-backed securities are cash-settle contracts, the size of the tranche does not limit the amount of credit default swaps that can be written on the tranche, nor does it impair ultimate settlement of the contract in the event of default.

By cash-settle, I mean that the tranche itself need not be physically delivered to the counterparty in order to collect payment. An investor with a short view may therefore confidently buy more than $5,894,000 in credit default swap protection on this tranche.

As well, these credit default swap protection contracts are pay-as-you-go. This means the owner of protection on a given tranche need not hand over the contract before full payment is received, even across trustee reporting periods.

For instance, if only 50% of the PPSI 2005-WLL1 M9 tranche is written down in the first month, the owner of $10,000,000 in protection would collect $5,000,000 and would not need to forfeit the contract to do so. If in the second month the remaining 50% is written down, the owner of protection would collect the remaining $5,000,000.

A mortgage-backed securitization is of course a dynamic entity, and a short investor must monitor many different factors in addition to the aforementioned credit support. For instance, as a mortgage pool matures, mortgages are refinanced and prepaid, and the principal value of mortgages in the pool declines.

Prepayments reduce principal in the senior tranches first. Generally, the idea is that investors in subordinate tranches should not get capital returned until the senior tranches are paid off. There are some minor exceptions, but this is generally true.

For instance, today, the current face value of the AAA tranches in PPSI 2005-WLL1, which was issued in March of 2005, is roughly $243,691,000 versus the original face value of $667,705,000 due to a high rate of refinancing.

Those who can refinance will. Our focus is on those who cannot. For those who cannot, some mortgages will go bad. Lenders tend to consider loans delinquent for roughly 90 days of missed payments, and then the foreclosure process looms.

Typically within 90 days but occasionally up to 180 days after foreclosure, the real estate underlying the bad mortgage is sold.

If the proceeds cannot pay off the mortgage, a loss is realized. If the cash being generated by the mortgage pool cannot cover the degree of losses, the mortgage pool takes a loss. This is applied to the most subordinate tranche first.

Most of these subprime mortgage pools will likely see maximum foreclosures a little over two years into the life of the pool. The reason is that most subprime mortgages included in these pools – typically 80% of the mortgages in the pools – are adjustable rate mortgages.

As a result, the mortgage pool will experience its most significant stress when the initial teaser rate period ends on its set of adjustable rate mortgages. Generally, this period ends on average 20-24 months from the date of issuance of the mortgage pool.

Since the Funds shorted mortgage pools mostly originated in spring through late summer 2005, I expect the pools shorted will see maximum stress during the latter half of 2007. No one shorting these tranches would expect to see a payoff during the first year of holding the short and likely not even during the second year.

In fact, the apparent credit support under each rated tranche will grow during the first year or two. If the thesis plays out as originally contemplated, the reduction in credit support and ultimately the payouts on credit default swaps would come shortly after the mortgage pools face their peak stress, or roughly 2-2.5 years after deal issuance.

In the interim, the value of these credit default swap contracts should fluctuate. In a worsening residential housing pricing environment, and with poor mortgage performance in the pools, one would expect that protection purchased on tranches closer to peak stress would garner higher prices, provided that home prices have not appreciated significantly during the interim.

As well, credit protection purchased on tranches more likely to default should garner higher prices. I would note that during the summer of 2005, national residential home prices in the United States peaked along with the easiest credit provided to mortgage borrowers in the history of the nation. Recent year over year price declines have not been seen since the Great Depression.

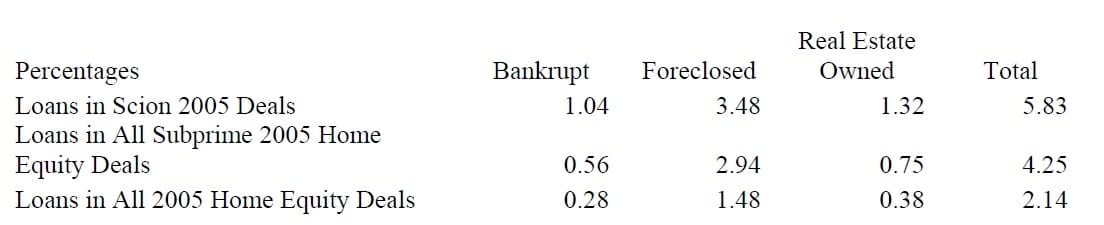

With that in mind, let us examine how the tranches I selected as shorts are performing relative to the other 2005-vintage deals. The data in this table was compiled by a third party data provider. This provider captures approximately 80% of all 2005 home equity deals in its database, which is up to date through August.

I do believe trends such as these validate the proprietary criteria upon which I selected the pools for the mortgage short portfolio. While these numbers seem low, the Funds shorted the more subordinate tranches within these pools specifically so that the short position would not be dependent on the Armageddon scenario for U.S. residential housing.

Fundamental developments, however, do not necessarily play into pricing of these credit default swaps while we await peak defaults because most off-the-run deals simply do not have an active market.

So, how exactly are the values of the Funds’ positions priced 4during this time? In a nutshell, our counterparties set the values. The seller of credit default swap protection is the buyer’s counterparty, and vice versa.

The Funds have six counterparties from which credit protection on subordinated tranches of mortgage-backed securities has been purchased. The creditworthiness of our counterparties is an integral part of the investment thesis.

We have chosen counterparties that are among the largest banks and securities houses in the world, and we have negotiated ISDAs with each of these counterparties. ISDA stands for International Swap Dealer Association, and an ISDA is the common term for the contract governing the dealings between counterparties to a swap transaction.

Importantly, we negotiated ISDA contracts that give us the right to collateral should our swap positions move in our favor. To the extent the Funds see the values of our swap positions move the other way, the Funds send collateral to our counterparties covering the decline in value of the positions.

This mechanism protects each counterparty in the event of a default by the counterparty on the other side. The dealer counterparties are the marking agents for the Funds’ positions, and therefore the values set by these dealer counterparties determines how the collateral flows on a daily basis.

Scion Capital has been using these same counterparty-assigned contract values that we use for collateral purposes to determine the net asset value of the Funds. The value of credit default swaps on subprime mortgage-backed securities is a calculation involving certain assumptions.

For any buyer of protection to have confidence in the value assigned to his positions, he must have confidence in the methodologies behind the pricing data provided by his dealer counterparties.

The pricing data we receive from our counterparties is often very old or stale-dated. These prices are sometimes tied to movements in the on-the-run index products, which contain neither any of our deals nor any deals remotely similar to our deals- almost all of which are off-the-run. We have found the methodologies to be frankly inconsistent.

In the absence of confidence in counterparty marks, a third party may be considered, but today there is no sufficient third party marking agent for credit default swaps on mortgage-backed securities. Some may rather use a mathematical model to price the portfolio, but Scion Capital does not price its portfolio securities to models.

The Funds currently carry credit default swaps on subprime mortgage-backed securities amounting to $1.687 billion in notional value. As I selected these, I was not looking to set up a diversified portfolio of shorts.

Our shorts will have common characteristics that I deemed to be predictive of foreclosure, and therefore they should be highly correlated with each other in terms of both the timing and the degree of ultimate performance.

Again, ultimate performance matters much more than the valuation marks accorded us by our counterparties in the interim. In the worst case, I expect our mortgage short will fully amortize to nil value over the next three years, corresponding to an average annual cost of carry over that time of roughly six percent of current assets under management. Calibrating the more positive outcomes will become easier as 2007 progresses.

Michael J. Burry, M.D.

Scion Capital, LLC

RMBS CDS & Side Pockets – Some Good Questions

November 7, 2006

Can’t the servicers manipulate these pools? Don’t they advance interest?

Generally, servicers may advance interest payments to the pool when a mortgage goes delinquent. Once a mortgage is foreclosed upon, the servicer’s advance is typically billed to the mortgage pool.

Servicers are themselves rated and in my view would have little incentive to refuse to foreclose upon mortgages or delay sales of real estate during a time of declining home prices.

Recent data has implied that servicers have been more willing to take bigger losses on mortgages as national home price levels weaken. As far as deciding when a tranche should be written down, this duty is left to the trustee rather than the servicer. It is the trustee, not the servicer, which administers cash flows to investors within the trust.

Can’t the manager of the mortgage pool replace bad loans with good ones?

For reasons of fraud and similar concerns, it is often the case that a bad loan may be replaced during the first six months to one year of a trust’s existence. Nearly all our shorts involve deals for which this period is past.

To the extent such replacement of fraudulent loans happened, it was disclosed in servicer reports, and it was not significant.

What is loss severity?

Loss severity is the average percentage loss realized on mortgages during the trustee reporting period. Losses on mortgages are realized when the underlying foreclosed real estate is sold, but proceeds cannot fully repay the mortgage.

What is the deal with the step-down at three years? Is this a concern?

This is a somewhat complex mechanism built into most mortgage pools that allows for the senior tranches to be repaid relatively quickly if the pool is performing poorly and to be paid down more slowly if the pool is performing very well.

The 37 th month is a frequent date for this mechanism to kick in. Given the subordinated status of the tranches we are short and the accelerated deterioration of these pools, this mechanism would appear to be not very relevant to our position.

What is interest rate swap protection and is it relevant?

In the earlier years of a mortgage pool, income is relatively fixed, while the payout to investors in the pool floats based on LIBOR. Rising rates may cause payouts to exceed income, causing a mismatch.

At the time the mortgage pool is structured, the seller may purchase an interest rate swap that itself is profitable in the event of higher interest rates so as to mitigate risk of a mismatch. These swaps typically have a fixed term. This is relevant. Not all pools have this feature, and all else equal pools with this feature tend to be less interesting as shorts.

How is your portfolio of mortgage shorts split by rating?

On a notional basis, 41.6% and 49.8% of our shorts are on BBB- and BBB tranches, respectively. The remaining are A-rated tranches.

Is PPSI 2005-WLL1 representative of the rest of the portfolio?

No. This is an example, and it is not meant to be representative. For instance, many pools do not have a credit enhancement, certificate of equity, or CE, tranche, like PPSI 2005-WLL1 does. Commonly, there is an overcollateralization layer that is not specifically set out as a tranche.

Do you really believe the dealers are colluding to mark your book low?

No. I believe the dealers are acting in their best interests, but I have no evidence of collusion of any kind. I do not believe our counterparties best interests are necessarily aligned with the Funds’ best interests, and I feel it is the better part of prudence to maintain that opinion. I generally feel people follow the incentives before them.

Why did you ever allow the counterparties to mark your books?

I have not been aware of a better alternative. I have been wary of the conflicts of interest that would arise should we set foot on the slippery slope that is marking our own book. Do your concerns with day-to-day valuation affect the enforceability of the CDS contract in the event the underlying tranche experiences write-downs?

No. These are cash-settle, pay-as-you-go contracts backed by the full credit of our counterparty. When the trustee reports a tranche has had write-downs, we will have the contractual right to payment from our counterparty. There will be no assumptions involved, and valuation will not be a factor.

How will you mitigate losses if it doesn’t work out like you think?

Should I detect a reason for the Funds to exit some or all of these positions, I will seek out ways in which to liquidate the positions. I am hopeful that our careful monitoring of the Funds’ positions will lend us the insights necessary to mitigate losses should the need arise.

What is the longest these credit default swaps on mortgage-backed securities can be in force?

The stated life of each swap contract is technically 30 years. Practically however, prepayment speeds have determined the lifespan, or duration, of mortgage pools for nearly the entire history of the market in mortgage-backed securitizations. Most dealers estimate the life of the mortgage pools containing the tranches underlying the swaps in our portfolio at 2-3 years.

Isn’t there an active market in CDOs?

We do not invest in either cash CDOs or synthetic CDOs. The cash residential mortgage-backed securities, or RMBS, market is also very large, but we do not participate in this market. The securities we have invested in are credit default swaps, also known as CDS.

Do synthetic CDOs do the same thing as Scion?

No. Synthetic CDOs are roughly similar in architecture to the PPSI example above, but with credit default swaps on specific corporate names or on specific asset-backed securities substituting for mortgages.

Buyers of these swaps then provide the cash flows that will support the synthetic CDO. Generally, buyers of synthetic CDO securities go long a credit while the buyers of the swaps are going short the credit. Most of the supply of credit default swaps in 2006 is tightly linked to the issuance of new synthetic CDOs.

What is the ABX Index?

An ABX index is an index of credit default swaps on mortgagebacked securities. There are multiple ABX indices, each defined by a vintage and an average credit rating. The first ABX index was launched in early 2006, and the structure of the index bears very little resemblance to the Funds’ portfolio of mortgage shorts. I do not view any such index as a good proxy for the Funds’ positions.

What are the other side pockets again? Why do the side pockets fluctuate in value a bit?

From the perspective of an investor, the number and level of side pockets will depend on the timing of the investor’s capital additions to the Funds. The other side pockets are Livedoor, Blue Ocean Re, and Symetra. All continue to be represented at cost.

Any variation in side pocket value today comes from the fact that the Livedoor position is held in Japanese yen, while we report in dollars. This leaves that position exposed to foreign exchange movements. Additionally, side pockets may appear to loom larger when assets under management have fallen.

If you side pocket these and you get a lot of withdrawals, are the remaining investors stuck with very large positions in these side pockets?

No. The nature of a side pocket is that exiting investors retain their portion of the side pocket. As a result, the remaining investors see no increase in concentration in the side pocketed position. Will you allow investors transparency into all the different positions in the mortgage CDS side pocket?

I hold no plans to offer transparency into these positions, nor do I expect to compromise the opportunity to trade out of these positions at opportune times. Why are you not side pocketing the corporate CDS positions?

Although we hold offthe-run single name corporate credit default swaps that I do not find to be very liquid, there is a bona fide and adequate market in corporate credit default swaps. A side pocket is not necessary.

How big is the corporate CDS portfolio?

As of the end of October, single name corporate CDS amount to 3.27% and 3.55% of assets under management in the Scion Value Fund and the Scion Qualified Value Fund, respectively. The duration of this portfolio is roughly 3.5 years.

These credit protection contracts cover $4.27 billion in notional value, largely focused on financial companies. A number of these companies are engaged in the mortgage business.