| September 2013 | October 2013 | Comments |

| Information received since the Federal Open Market Committee met in July suggests that economic activity has been expanding at a moderate pace. | Information received since the Federal Open Market Committee met in September generally suggests that economic activity has continued to expand at a moderate pace. | No real change. What economy are they watching? |

| Some indicators of labor market conditions have shown further improvement in recent months, but the unemployment rate remains elevated. | Indicators of labor market conditions have shown some further improvement, but the unemployment rate remains elevated. | Weasel words because the participation rate is falling, and wages are stagnant. |

| Household spending and business fixed investment advanced, and the housing sector has been strengthening, but mortgage rates have risen further and fiscal policy is restraining economic growth. | Available data suggest that household spending and business fixed investment advanced, while the recovery in the housing sector slowed somewhat in recent months. Fiscal policy is restraining economic growth. | No change. |

| Apart from fluctuations due to changes in energy prices, inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable. | Apart from fluctuations due to changes in energy prices, inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable. | No change. TIPS are showing similar inflation expectations since the last meeting. 5y forward 5y inflation implied from TIPS is near 2.57%, down 0.12% from September. |

| Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. | Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. | No change. Any time they mention the “statutory mandate,” it is to excuse bad policy. |

| The Committee expects that, with appropriate policy accommodation, economic growth will pick up from its recent pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. | The Committee expects that, with appropriate policy accommodation, economic growth will pick up from its recent pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. | No change.Emphasizes that the FOMC will keep doing the same thing and expect a different result than before. Monetary policy is omnipotent on the asset side, right? |

| The Committee sees the downside risks to the outlook for the economy and the labor market as having diminished, on net, since last fall, but the tightening of financial conditions observed in recent months, if sustained, could slow the pace of improvement in the economy and labor market. | The Committee sees the downside risks to the outlook for the economy and the labor market as having diminished, on net, since last fall. | Financial conditions are looser. That’s largely due the end of imminent tapering. Also that the economy is weak. |

| The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, but it anticipates that inflation will move back toward its objective over the medium term. | The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, but it anticipates that inflation will move back toward its objective over the medium term. | No change. CPI is at 1.2% now, yoy. |

| Taking into account the extent of federal fiscal retrenchment, the Committee sees the improvement in economic activity and labor market conditions since it began its asset purchase program a year ago as consistent with growing underlying strength in the broader economy. However, the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases. | Taking into account the extent of federal fiscal retrenchment over the past year, the Committee sees the improvement in economic activity and labor market conditions since it began its asset purchase program as consistent with growing underlying strength in the broader economy. However, the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases. | No change. This notable paragraph, saying that the “taper” is not starting because fiscal policy is not as stimulative as the Fed wants. |

| Accordingly, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. | Accordingly, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. | No change.Operation Twist continues. Additional absorption of long Treasuries commences. Fed will make the empty “monetary base” move from $3 to 4 Trillion by the end of 2013.

|

| Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate. | Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate. | No change. |

| The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. | The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. | No change. Useless comment. |

| In judging when to moderate the pace of asset purchases, the Committee will, at its coming meetings, assess whether incoming information continues to support the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective. | In judging when to moderate the pace of asset purchases, the Committee will, at its coming meetings, assess whether incoming information continues to support the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective. | No change. |

| Asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s economic outlook as well as its assessment of the likely efficacy and costs of such purchases. | Asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s economic outlook as well as its assessment of the likely efficacy and costs of such purchases. | No change. |

| To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. | To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. | No change.Promises that they won’t change until the economy strengthens. Good luck with that. |

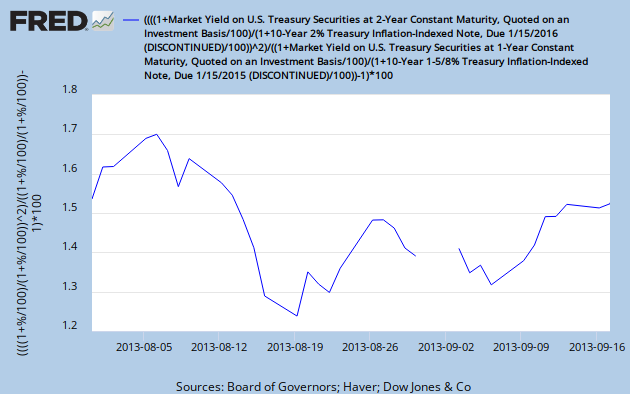

| In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. | In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. | Not a time limit but economic limits from inflation and employment.Just ran the calculation – TIPS implied forward inflation one year forward for one year – i.e., a rough forecast for 2015, is currently 1.52%. Here’s the graph. The FOMC has only ~1% of margin in their calculation.

|

| In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. | In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. | No change. |

| When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. | When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. | No change. |

| Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Charles L. Evans; Jerome H. Powell; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. | Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Charles L. Evans; Jerome H. Powell; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. | No change |

| Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations. | Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations. | No change. George continues to make her point that is the same as mine in my piece Easy In, Hard Out; that the Fed may have greater problems as a result of its abnormal policies, whatever they do in the future. |

Comments

- This announcement was a nothing-burger.

- No taper yet. Equities, and long bonds fall. Commodities do nothing. Feels like some market participants expected more QE.

- The FOMC says that any change to policy is contingent on almost everything.

- They think that if they use more words, they will be clearer. Longer statements are harder to parse and understand.

- Current proposed policy is an exercise in wishful thinking. Monetary policy does not work in reducing unemployment, and I think we should end the charade.

- In the past I have said, “When [holding down longer-term rates on the highest-quality debt] doesn’t work, what will they do? I have to imagine that they are wondering whether QE works at all, given the recent rise in long rates. The Fed is playing with forces bigger than themselves, and it isn’t dawning on them yet.

- The key variables on Fed Policy are capacity utilization, unemployment, inflation trends, and inflation expectations. As a result, the FOMC ain’t moving rates up, absent increases in employment, or a US Dollar crisis. Labor employment is the key metric.

- GDP growth is not improving much if at all, and much of the unemployment rate improvement comes more from discouraged workers, and part-time workers.

By David Merkel, CFA of alephblog.com

{kind=link}

{kind=link}