Discusses the partnership and the potential income it might generate with some highlights from the recent Q3 result

Technology-based biopharma company Xeris (NASDAQ:XERS) is set to boost its revenue with an upfront cash payment from a research collaboration and option agreement that was secured with mid-cap pharma Horizon Therapeutics (NASDAQ:HZNP).

Xeris opened 12.6% higher at $1.43 on the news before traders banked profits, with the stock drifting lower and closing with a 3.9% gain at $1.32 on Wednesday afternoon.

Q3 2022 hedge fund letters, conferences and more

Find A Qualified Financial Advisor

Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Xeris-Horizon Therapeutics Merger Agreement

The agreement will see Xeris use its proprietary formulation technology platform called Xeriject to develop an “ultra-concentrated, ready-to-use, subcutaneous injection of teprotumumab” and will give Horizon an option to licence XER’s technology.

Teprotumumab is currently the first and only treatment currently approved by the FDA to treat Thyroid Eye Disease (TED), a progressive visual autoimmune disease.

As part of the terms of the deal, Horizon will pay Xeris an upfront payment that has not been disclosed to the market. In addition to the upfront payment, Xeris may also be entitled to receive further payments for: development milestones, regulatory milestones, sales-based milestones and royalties on future sales if the commercial licence option is exercised.

Chairman and CEO Paul Edick commented on the partnership highlighting “This partnership demonstrates the potential value of our technology to enable large molecule subcutaneous injections that provide a more patient friendly regimen that is effective, safe, and more convenient, with potential for improved adherence.”

Xeris has risen 7 ranks this week and is currently the 69th most held security among retail investors. To gain access to retail trade flow data for free, click here.

Earlier in November, Xeris provided its third quarter update to investors with the company growing revenues by 31% over the year to $29.6 million. The result came in marginally ahead of consensus forecasts of around $29 million.

Xeris reduced its net loss from -$26 million in 2021 to -$21.8 million in 2022, equating to EPS of -16 cents per share. The net result came in broadly as expected by the street.

The firm ended the quarter with $84.1 million in cash and $9.3 million in short-term investments, as well as $27 million in net receivables.

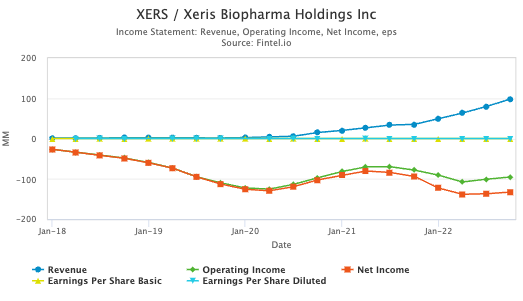

The chart provided to the right from the Fintel financial metrics and ratios page for Xeris shows the growing level of sales over time with net income expected to track towards 0 in the coming year.

At the time of the result, CEO Paul Edick narrowed full year guidance expectations to generate $105 to $110 million in next product revenue, from $90 to $110 million prior with increased visibility of sales for the final quarter of the fiscal year.

The company also raised its year-end cash balance guidance to $110-120 million and reaffirmed its guidance to generate $50 million of synergies, driving its ability to reach break-even profitability by the end of 2023.

Analysts Glen Santangelo and Peter Warendort from Jefferies investment bank reiterated their ‘buy’ recommendation and $4 target on the stock to investors following the result.

The firm believes that Xeris stock warrants a valuation premium because of the significant market opportunity and the expectation they will not need to raise capital before reaching break even. Jefferies thinks there is a significant opportunity to gain further market penetration in the next few years.

On average Xeris has a consensus ‘buy’ recommendation with an average $5.25 target price.

Article by Ben Ward, Fintel