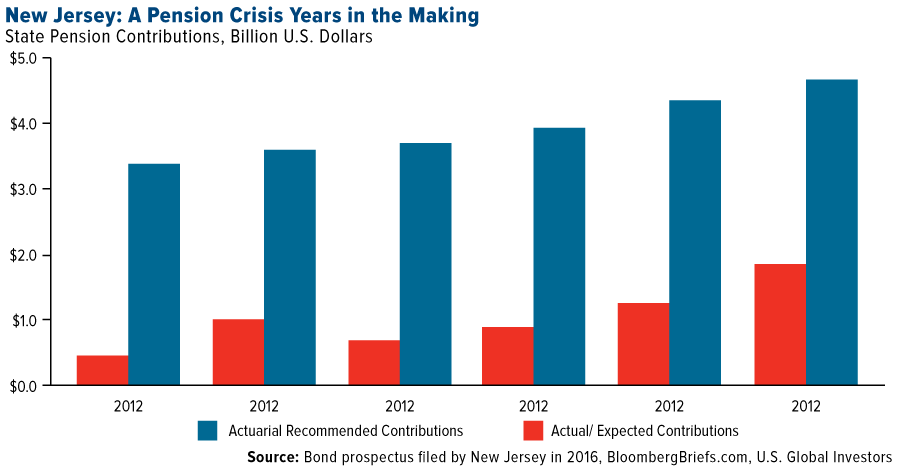

Also see JPMorgan On State Debt: No Mathematical Solution In New Jersey

This week I returned from Zurich, where I spoke at the European Gold Forum. Investor sentiment for the yellow metal was particularly strong on negative real interest rates and heightened geopolitical uncertainty in the U.S., Europe, Middle East and South Africa. A poll taken during the conference showed that 85 percent of attendees were bullish on gold, with a forecast of $1,495 an ounce by the end of the year.

The upcoming presidential election in France is certainly raising concerns among many international investors. On one end of the political spectrum is Marie Le Pen, the far-right National Front candidate who, if elected, might very well pursue a “Frexit.” On the other end is Jean-Luc Mélenchon, a socialist of such extreme views that he makes Bernie Sanders look like Ronald Reagan. I was shocked to read that Mélenchon has pledged to implement a top tax rate of 100 percent—and even more shocked to learn that he’s moving up in the polls. An insane 100 percent tax rate would surely return the country to medieval-era feudalism, which is just another name for slavery. All the wealth naturally goes to the very top, and corruption thrives.

It’s important to recognize that in civil law countries such as France, hard line socialism is much more likely to take hold. Just look at South Africa. While in Zurich, I had the pleasure to speak with Tim Wood, executive director of the Denver Gold Group and former associate of South Africa’s Chamber of Mines. According to Tim, the poor government policies of South Africa’s socialist president, Jacob Zuma, is driving business out of the country and has led to the resignations of several members of parliament. Tens of thousands of protestors have taken to the streets of Johannesburg demanding Zuma to step down, especially following his firing of Finance Minister Pravin Gordhan. The rand, meanwhile, has plummeted and the country was recently downgraded to “junk” status

One of the consequences of a weaker rand has been stronger gold priced in the local currency and higher South African gold mining stocks, as measured by the FTSE/JSE Africa Gold Mining Index. Among the gold companies that have seen some huge daily moves in recent days are Sibanye Gold and Harmony Gold.

South African gold stocks look very attractive in the short term. Over the long term, however, they might find it increasingly difficult to operate efficiently and profitably in such a mismanaged jurisdiction.

PMIs Show Impressive Manufacturing Growth

It’s been an eventful week, to say the least. The U.S., for the first time, became directly involved militarily in Syria’s years-long civil war. Senate Republicans invoked the “nuclear option” to prevent a Democratic filibuster, allowing federal judge Neil Gorsuch to obtain Supreme Court confirmation. President Donald Trump met with Chinese leader Xi Jinping at Mar-a-Lago, the so-called “Winter White House,” to discuss trade and North Korea, among other issues.

And today we learned the U.S. added only 98,000 jobs in March, down spectacularly from the 235,000 that came online in February. In response to this and the Syrian air strike, gold jumped more than 1 percent, touching $1,272 in intraday trading, its highest level in five months.

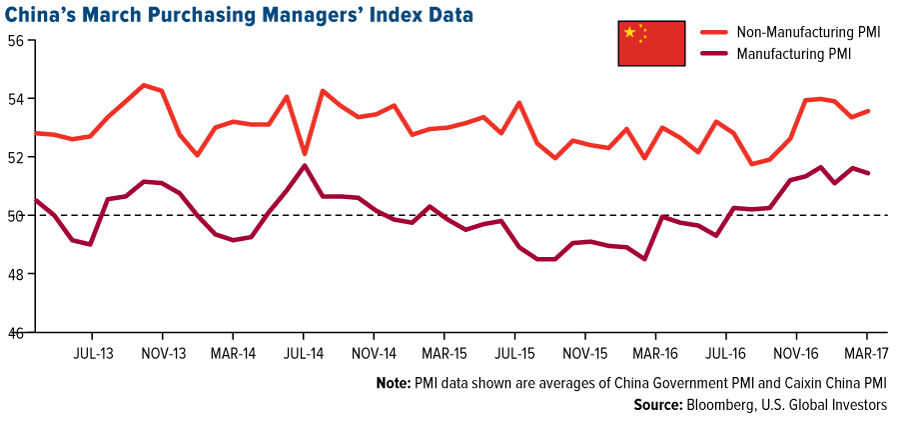

Fresh purchasing manager’s index (PMI) readings for the month of March were also released, showing continued manufacturing sector expansion in the world’s largest economies, including the U.S., China and the eurozone. All of Zurich was under construction, it seemed, with cranes filling the skyline in every direction. And when I flew back into San Antonio, sections of the international airport were also under heavy construction. This all reflects strong local and national economic growth in Switzerland and the U.S.

I especially like the Zurich Airport. I travel a lot, and it’s the only airport I know of where you can sit out on an open deck and watch and listen to the jets take off and land.

The official China PMI rose to 51.8, the fastest pace in nearly five years. Because the PMI is a forward-looking tool, this bodes well for industrial metals, as measured by the London Metal Exchange Index (LMEX). The Asian giant, as I’ve pointed out before, consistently ranks among the top importers of copper, aluminum, steel and more.

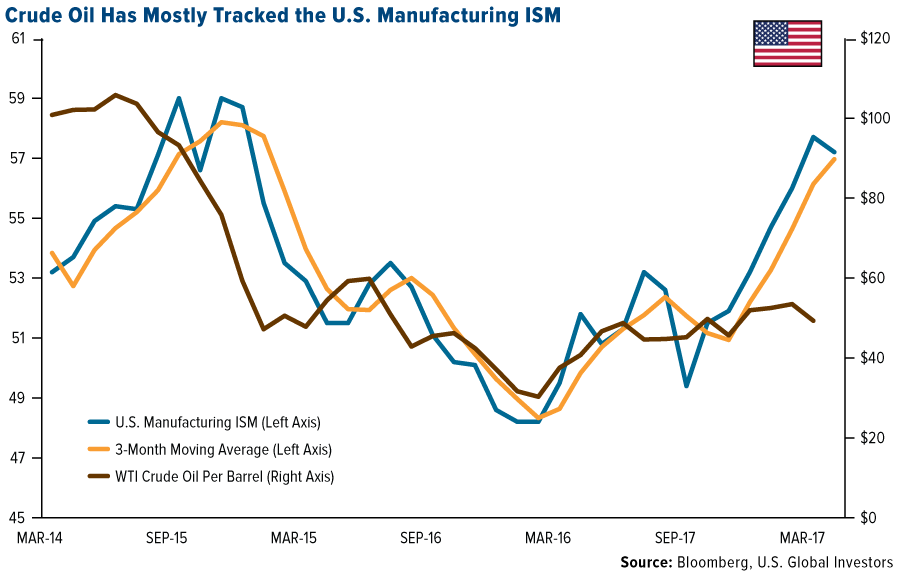

The U.S. Manufacturing ISM cooled slightly to 57.2, down from 57.7 in February. This still remains high on a historical basis. Because the U.S. is the number three producer of crude, following Russia and Saudi Arabia, oil prices have tended to track the country’s manufacturing index.

Trump Tackles U.S. Trade with China

Again, Trump met with China’s Xi, a man who can be considered the U.S. president’s counterpart in many more ways than one. In February, I included Xi in a list of four global leaders who have more in common with Trump than some people might realize. This week the Brookings Institute compiled a list of the many “striking similarities” between the two men. Among other commonalities, they’re both nationalists; they’re both populists and have expressed a desire to fight corruption; they both have a rocky relationship with the press and intellectual community; and they both prioritize domestic affairs over foreign affairs.

None of this stopped Trump from being very critical of China on the campaign trail. He threatened to name the country as a currency manipulator and raise tariffs as much as 35 percent. It will be interesting to see what agreements, if any, can come out of this meeting between the two leaders.

Trump is not wrong to raise the alarm over U.S.-China trade. In 2016, the U.S. trade deficit with China stood at a whopping $347 billion. This is down slightly from $367 billion in 2015, but still a huge number. If you look at the total U.S. balance of payments since 1960, you get an even greater sense of the imbalance.

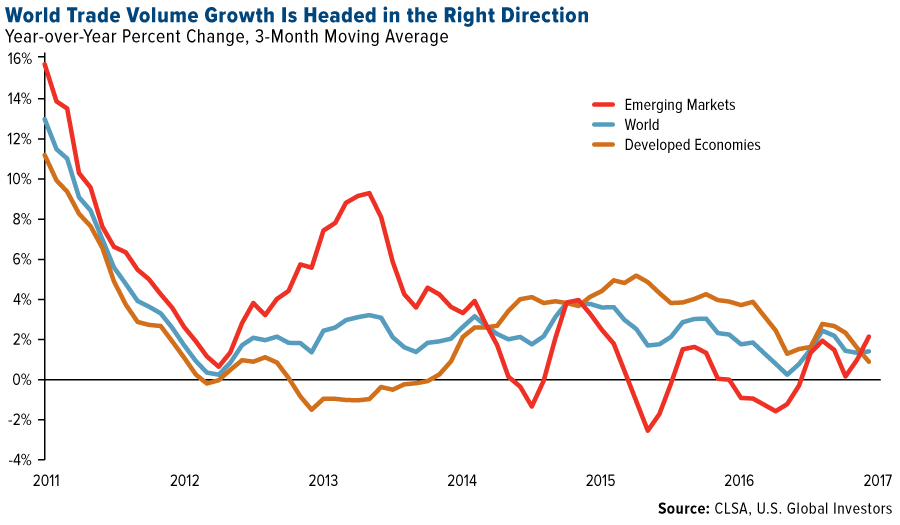

At the same time, world trade volume growth has improved in recent months, especially in emerging markets and Asia.

It’s important that Trump put ample thought into improvements on international trade. I’m not convinced tariffs and border adjustment taxes (BATs) are the solution. Look at what happened in the 1930s with the Smoot-Hawley Tariff Act. In an effort to “protect American jobs,” the U.S. raised tariffs on more than 20,000 goods coming into the country, many of them as high as 59 percent. Once the act went into effect in June 1930, a trade war promptly ensued and global trade all but dried up. Today, historians almost unanimously agree that the policy, which President Franklin Roosevelt later overturned, only exacerbated the effects of the Great Depression.

One of the biggest reasons why the U.S. has such a trade deficit is due to its abnormally high corporate tax rate. The country’s largest export is intellectual and human capital. Think Apple and Google, which are designs and ideas. The problem is that the dollars received in exchange for these goods and services are sitting in Ireland, or elsewhere, and are thus not counted in the official trade balance. Should the corporate tax rate decline to an average of around 18 to 20 percent, which is consistent with other developed countries, U.S. multinational companies would likely be more inclined to repatriate those profits and tilt the balance back in America’s favor.

Tax reform, therefore, is key in making sure the U.S. remains competitive on the world stage.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.03 percent. The S&P 500 Stock Index fell 0.30 percent, while the Nasdaq Composite fell 0.57 percent. The Russell 2000 small capitalization index lost 1.54 percent this week.

- The Hang Seng Composite rose 1.00 percent this week; while Taiwan was up 0.63 percent and the KOSPI fell 0.39 percent.

- The 10-year Treasury bond yield fell less than one basis point to 2.38 percent.

Domestic Equity Market

Strengths

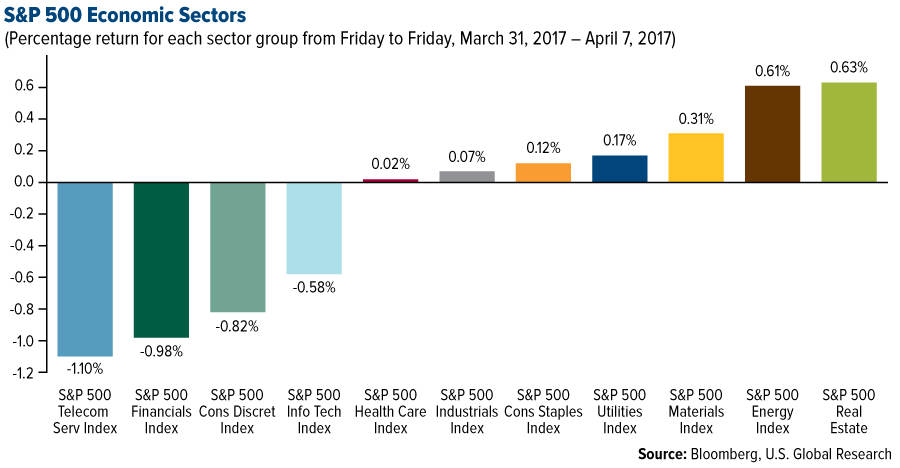

- Real estate was the best performing sector of the week, increasing by 0.63 percent versus an overall decrease of 0.27 percent for the S&P 500.

- Staples was the best performing stock for the week, increasing 11.17 percent.

- Samsung had a blockbuster quarter. The electronics giant said first-quarter operating profit was probably $8.8 billion, its best quarterly profit in more than three years, thanks to strong demand for memory chips.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling 1.10 percent versus an overall decrease of 0.27 percent for the S&P 500.

- Acuity Brands was the worst performing stock for the week, falling 15.14 percent.

- Snapchat’s lead underwriter made an error analyzing the stock. Morgan Stanley published an equity research note on Snapchat and gave the stock a $28 target. A day later the bank issued a correction, changing important metrics and reducing its forecast earnings in the model but not the $28 target.

Opportunities

- Okta, which develops software for cloud security and identity management, priced its initial public offering Thursday evening at $17 a share, giving it a valuation of $1.54 billion. Okta will trade on the Nasdaq under the ticker OKTA.

- Financials appear to be the least-valued sector of the stock market, according to Goldman Sachs equity analysts. The S&P 500 sector that includes insurance companies and banks doesn’t have the lowest expectations for earnings growth among investors. However, the gap between its current implied five-year earnings growth rate and its average over the past 10 years — an indication of how swiftly expectations have shifted — implies the lowest rate among all sectors.

- Apple’s profits might be boosted by 16 percent if Trump’s proposed tax reforms are enacted, according to an analysis by Citi. The proposals would make it likely that Apple would move its foreign cash back to the U.S. in order to pay the least amount of tax. In the most recent quarter, Apple said it was holding $246 billion in cash, of which $230 billion was held in foreign subsidiaries. Citi analysts Jim Suva and Asiya Merchant say they would expect Apple to use the cash to increase its stock buyback program, adding 10 percent to EPS. The lowered domestic tax rate would also improve earnings per share by 6 percent.

Threats

- Larry Fink, the chief executive at BlackRock, which with $5.1 trillion is the world’s largest investor, thinks U.S. stocks are overvalued. “We don’t have the tax reform that we’re expecting,” Fink told CNBC. “If we don’t see a true deregulation, I think the markets would have some setbacks there.”

- Twitter shares slid following a report that cofounder and board member Evan Williams plans to sell up to 30 percent of his shares. “After a year-and-a-half of no selling, I have filed a new 10b5–1 plan to liquidate a minority of my TWTR over the next year,” Williams wrote in a blog post on Medium after Business Insider inquired about the sale.

- Health insurance giant Aetna is pulling out of the Affordable Care Act individual insurance exchanges in Iowa. Aetna said the decision was due to uncertainty surrounding the future of the ACA, also known as Obamacare, and financial losses the company was taking.

The Economy and Bond Market

Strengths

- The unemployment rate dipped 0.2 percent to 4.5 percent, the lowest level since May 2007, while average hourly earnings rose 2.7 percent versus a year ago.

- Europe’s economy had its best quarter in six years. The latest PMI surveys from IHS Markit showed March’s composite reading of 56.4 was the best pace of expansion since the first quarter of 2011.

- Euro area unemployment hit an eight-year low. The region’s unemployment rate fell to 9.5 percent in February, its lowest reading since May 2009, according to Eurostat data released Monday.

Weaknesses

- The U.S. economy added 98,000 jobs in March. The report from the Bureau of Labor Statistics showed job growth decelerated in last month. The headline number was below the 180,000 expected by economists. In addition, both January and February payrolls were downwardly revised.

- U.S. manufacturing data came in mixed. The Institute for Supply Management and Markit Economics on Monday released reports on surveys of U.S. manufacturers conducted during March. Markit’s final PMI reading fell to 53.3, the lowest in six months and below the forecast for 53.5. The ISM’s was 57.2, down from 57.7 in February and in line with expectations.

- Automobile sales for the month of March missed expectations. Ford saw sales decline 7.2 percent, worse than the 5.9 percent decline expected by analysts. GM also missed expectations with a growth in sales of just 1.6 percent, lower than its 7 percent projection. Fiat Chrysler whiffed with a 5 percent decline in sales against a 0.4 percent growth expectation.

Opportunities

- The release of retail sales data is scheduled for Good Friday when most financial markets will be closed. Real consumer spending contracted in January and February. A rebound in March retail sales is needed to confirm that consumer fundamentals are still solid.

- In the last three months, core CPI has been rising somewhat faster than the 2 percent inflation objective. Another firm core CPI print would confirm a strengthening economy that’s gathering speed.

- The NFIB (Tuesday) and consumer sentiment (Thursday) surveys should be watched for sentiment toward the economy.

Threats

- New Jersey’s latest credit rating downgrade marks the state’s eleventh under Governor Chris Christie. Moody’s Investors Service cited the state’s significant under-funding of its pension plans as one reason for the downgrade to A3.

- According to New York Fed President William Dudley, the rising burden of student debt is weighing on interest rates in the U.S. Dudley and many of his colleagues have argued that the economy doesn’t have the potential to grow as fast as it did before the 2007-2008 financial crisis due to factors such as an aging population, low productivity growth and a reduced willingness by households to spend. Dudley and his staff presented data showing significant disparities in home-ownership between those who graduated from college with debt and those who graduated without it. In 2016, almost half of all 30-year-olds who left college with debt between 2006 and 2011 had missed at least one of their required monthly payments, according to the New York Fed researchers. Nearly a third of them had defaulted, meaning they missed nine straight months of payments. The median credit score of borrowers who missed at least one payment was below 670, which is near the dividing line between “prime” and “subprime” status. The median credit score of borrowers who defaulted on their debt was 549. The damage to those borrowers’ credit profiles from missed payments means it will be very hard for them to buy a home.

- Jamie Dimon released his annual letter to shareholders. Dimon said he was worried that “something was wrong” in the U.S. and there are six issues holding back economic growth. Dimon also expressed concerns over the low labor force participation rate in the U.S.

Gold Market

This week spot gold closed at $1,254.45, up $5.10 per ounce, or 0.41 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.54 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index rose 1.04 percent. The U.S. Trade-Weighted Dollar Index finished the week higher by 0.74 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Apr-3 |

U.S. ISM Manufacturing |

57.2 |

57.2 |

57.7 |

|

Apr-4 |

U.S. Durable Goods Orders |

1.7% |

1.8% |

1.7% |

|

Apr-5 |

U.S. ADP Employment Change |

180k |

263k |

245k |

|

Apr-6 |

U.S. Initial Jobless Claims |

245k |

234k |

259K |

|

Apr-7 |

U.S. Change in Nonfarm Payrolls |

180k |

98k |

219k |

|

Apr-11 |

Zew Survey Current Situation |

77.5 |

— |

77.3 |

|

Apr-11 |

Zew Survey Expectations |

14.0 |

— |

12.8 |

|

Apr-13 |

Germany CPI YoY |

1.6% |

— |

1.6% |

|

Apr-13 |

U.S. PPI Final Demand YoY |

2.4% |

— |

2.2% |

|

Apr-13 |

U.S. Initial Jobless Claims |

245k |

— |

234k |

|

Apr-14 |

U.S. CPI YoY |

2.6% |

— |

2.7% |

Strengths

- The best performing precious metal for the week was pretty much a tie between gold, platinum and palladium with roughly a 0.50 percent gain. Following the launch of a U.S. missile strike on Syria this week, gold rallied to its highest level in nearly five months, reports Bloomberg. Bullion was pushed back above its 200-day moving average, a level that analysts use to predict whether further gains will continue or stall.

- Earlier in the week, the minutes from the Federal Reserve’s March meeting “boosted gold prices with the mention of the shrinking of the balance sheet,” said Jingyi Pan, a Singapore-based market strategist, reports Bloomberg. “This agenda could potentially conflict with the pace of rate hikes, therefore placing pressure on the dollar.” In addition, gold advanced after automobile manufacturers reported worse-than-expected U.S. sales for March.

- Earlier in the week, the minutes from the Federal Reserve’s March meeting “boosted gold prices with the mention of the shrinking of the balance sheet,” said Jingyi Pan, a Singapore-based market strategist, reports Bloomberg. “This agenda could potentially conflict with the pace of rate hikes, therefore placing pressure on the dollar.” In addition, gold advanced after automobile manufacturers reported worse-than-expected U.S. sales for March.

Weaknesses

- The worst performing precious metal for the week was silver, with a fall of 1.30 percent. Late Friday CFTC data showed that money managers actually increased their bullish opinion on silver to the highest level in more than eight months. Profit taking, post the morning surge in precious metals prices, late Friday pulled silver into a loss for the week. Gold reserves in China’s central bank remained unchanged for the month of March, coming in at 59.24 million ounces, reports Bloomberg. This is the fifth straight month that gold reserves have remained unchanged.

- Despite Goldman Sachs encouraging investors to have “patience” for the commodity market in the wake of a waning price rally, inflows into ETFs linked to raw materials have significantly plunged in recent weeks, reports Bloomberg. Goldman believes the pace of economic growth in China will drive raw-materials consumption. In a similar fashion, RBC Mining & Material Equity Team cut its precious metals recommendation to underweight from market weight for the second quarter, reports Bloomberg. It upgraded bulk commodities to overweight from market weight and fertilizers to market weight from underweight.

- In Canaccord Genuity’s Precious Metals Note this week, the group says we may see potential NAV multiple compression in the sector. It notes margin compression, rising management compensation, declining IRR hurdle rates and rising operational and geopolitical risks as potential headwinds that could temper enthusiasm for gold producers.

Opportunities

- In its U.S. Economics report this week, Macquarie Research says that demographic forces are intensifying, as the share of population 75+ begins to rise. Because of this, the group says the economy is confronting two headwinds, or “double trouble”: 1) a closing of the output gap and the end of slack and 2) unprecedented demographic change that has accumulated over the past seven years is now intensifying. They believe the Fed Funds may normalize at 1.5 to 1.75 percent and the 10-year Treasury yield at around 2.3 percent, well below consensus of 3 percent for Fed Funds and 3.5 percent for 10-year yields. With CPI running at 2.7 percent, it is likely we will continue to see flat to negative real rates, thus supportive of gold. And in a note from BMI Research, the team says gold can be supported as the Fed is likely to raise rates only once more in 2017.

- The technical team from Desjardins says that the gold price (COMEX) has substantial potential upside. The team notes that total known ETF holdings of gold have increased around 2 million ounces year-to-date, implying a gold price of $1,310 per ounce. Similarly, Comex paper claims to physical gold continue to soar to 45:1, while deliverable gold has contracted by 50 percent since the start of the year.

- Zacks Investment Research highlights Klondex Mines in an article this week, calling the company an “off-the-radar potential winner” and saying it looks well positioned for a solid gain, but has been overlooked by investors lately. Klondex has seen estimates rise over the past month for the current fiscal year by about 22.2 percent, although that is not yet reflected in its price, as the stock lost 21.7 percent over the same time frame, Zacks writes. The company carries a Zacks Rank #2, a strong buy, further underscoring the potential for its outperformance. Another company with positive coverage this week is Rye Patch Gold, initiating a buy recommendation from George Topping from Industrial Alliance Securities. Topping predicts that Rye Patch will trade at 75 cents within a year, implying a potential 124 percent gain.

Threats

- The Senate voted along party lines on Thursday to change the Supreme Court’s longstanding rules and effectively eliminate the filibuster for Supreme Court nominees, reports Bloomberg. Now it will only require 51 votes, not 60, to bring a nominee up for a confirmation vote. The Senate confirmed on Friday Judge Neil Gorsuch as the new Supreme Court Justice, restoring the generally conservative majority. Some commentators noted that this may embolden President Trump to now pick even more judges for the bench that are more divisive, since a simple majority will be all that is needed to confirm. Similarly, Adam Posen, president of the Peterson Institute for International Economics, says that Trump is likely to pick a Fed chairman who is “very responsive to him.”

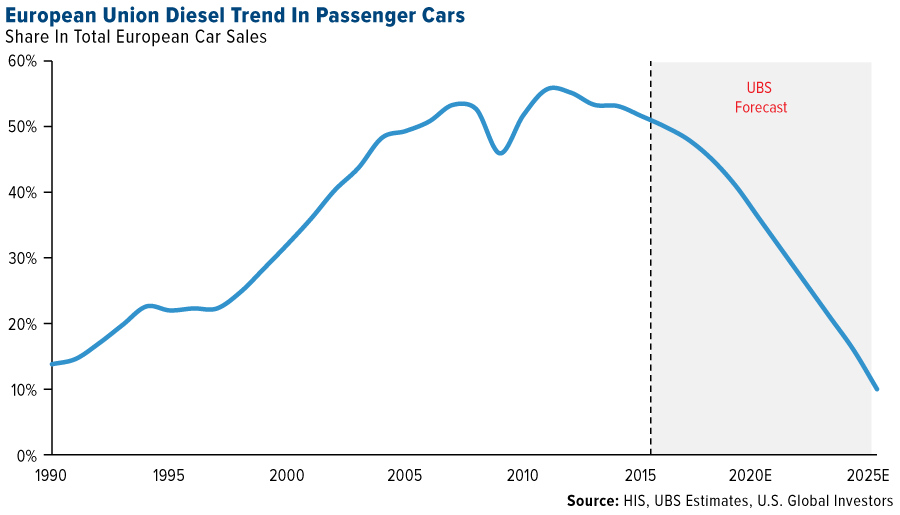

- In its Global Precious Metals Comment this week, UBS points out that European diesel share decline accelerated in March, supporting its view on platinum group metals (PGMs). Diesel share in the top five European auto markets declined, bringing the share of diesel vehicles to a multi-year low of 40.6 percent. The UBS Global Autos team expects this trend to accelerate further out, resulting in falling platinum demand.

- Goldman Sachs writes this week, that after five years of operating cost deflation, we expect costs to start responding to the 40 percent rebound in metal prices witnessed since January 2016. Once earnings tailwinds, we believe these core cost drivers should now start putting upward pressure on the full spectrum of global cost curves, Goldman continues. Additionally, the group notes that not all costs can be controlled, explaining that around 85 percent of the copper industry’s opex improvement was driven by what it considers to be “uncontrollable costs.”

April 5, 2017Gold Finds Strong Support from Negative Real Rates |

April 3, 2017Can Trump Dig Coal out of Its Slump? |

March 28, 20177 Reasons to Be Bullish on Emerging Europe |

Energy and Natural Resources Market

Strengths

- Crude oil prices rose 3.2 percent touching $56 a barrel this week on the back of geopolitical risks taking center stage as U.S. President Donald Trump issued a missile strike on Syria, according to the Financial Times. Although the conflict has little direct impact on oil supplies, market participants are extremely sensitive to such events as these actions can have broader global geopolitical consequences. It is too early to tell what kind of ramifications these actions will have on the price of oil; however, according to petroleum consultant Oliver Jakob of Petromatrix, the speed at which the U.S. took action is noteworthy to all participants of oil, and could translate into potentially bullish volatility in the near-term.

- The best performing sector for the week was the S&P/TSX Composite Diversified Metals & Mining Sub Industry Index. The index rose 5.22 on the back of rising precious metal prices this week as geopolitical risks take center stage of the global financial markets and investors seek safe-haven assets.

- Reliance Industries Ltd, an Indian energy giant, was the best performing stock this week finishing up 8.7 percent. The stock rose on the back of rallying oil prices.

Weaknesses

- Zinc was the worst performing commodity this week dropping 5.18 percent. The mineral has been dragged down on the back of falling steel and iron prices as market participants raise concerns over China’s outlook for construction and infrastructure demand. A negative read-through for zinc prices.

- The worst performing sector this week was the Bloomberg Auto Parts and Equipment Index. The index fell 5 percent on the back of poor first-quarter performance across the board for index members.

- The worst performing stock for the week was POSCO, one of the world’s largest steel making companies located in South Korea. The company fell 7.9 percent on the back of worry surrounding oversupply of steel across the globe which has negatively hit all steelmakers.

Opportunities

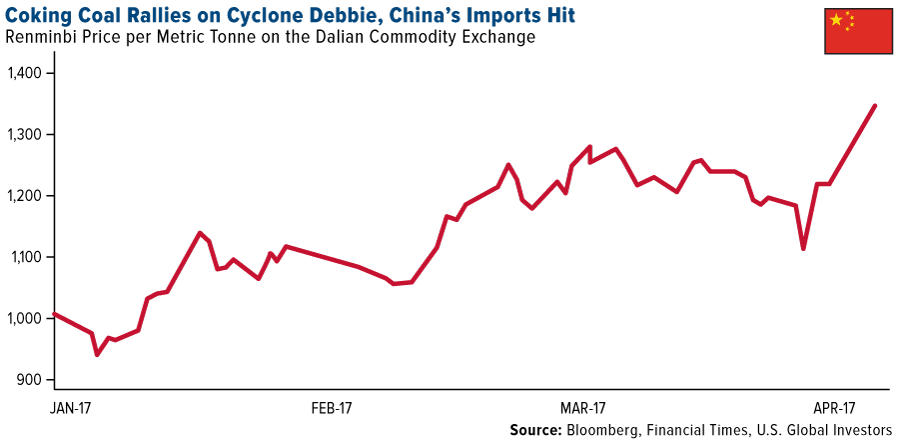

- Coking coal rallied this week 12.3 percent on the back of Cyclone Debbie knocking out a key supply route in the main mining area of Australia, according to the Financial Times. The disruption has forced steel mills across Asia to scramble for the commodity as Australia produces roughly half of the world’s coking coal supply and China is one of the largest consumers of the commodity. Until the area is alleviated of the storm and mining rails are repaired, coking coal’s fundamentals will be disrupted and could potentially rally further.

- Energy demand trends are improving in China, according to Goldman Sachs analyst Franklin Chow in a research note this week. Recent growth in economic and industrial activities has spurred a renewed appetite for demand of diesel and liquefied petroleum gas products as economic data for the months of January and February were very strong. Goldman is expecting this trend of increased demand to carry through for the rest of the year forecasting the country to consume above its average long-term consumption rate of 1.1 million barrels of oil per day (bpd) to 1.5 million bpd. A positive read-through for oil prices from one of the world’s largest emerging markets.

- Prices for shipping containers have risen to their highest level since October of 2015, according to Reuters. The Harpex Shipping Index, which tracks shipping container rates, has climbed 40 percent this year. Seaborne trade is often viewed as a bespoke indicator to world growth as these metal boxes account for transportation of 90 percent of the world’s manufactured goods. A positive read-through for global growth and raw material demand!

Threats

- The U.S. employment situation pertaining to nonfarm payrolls greatly disappointed expectations this week coming in at 98,000 versus expectations of 175,000, according to Bloomberg. This month’s print is a substantial and alarming print as the prior period came in at 235,000. This is a very negative development as nonfarm payrolls is considered to be one of the most important economic indicators of U.S. demand and growth. A negative read-through for raw materials.

- Crude oil inventories rose 7.4 percent, the equivalent of 1.6 million barrels, according to this week’s release by the Energy Information Administration (EIA). At a time when the OPEC cartel is cutting production in unison, global supply from other non-OPEC members around the globe is continuing to rise at steady rates, a negative read-through for oil prices globally.

- Purchases of automobiles declined in the month of March despite heavy incentives from automakers to spark demand and reduce inventory, according to Bloomberg. It is estimated that the number of unsold vehicles will take approximatively three months to clear if the rate of sales continues at its current pace. This is the highest level of inventory during any economic expansion since 1989 and could mark an expansion that has run too far, too fast, but only time will tell.

China Region

Strengths

- Malaysia’s exports expanded 26.5 percent in February from a year ago, and at the fastest pace since March 2010, reports Bloomberg. The increase was helped by a surge in demand for electrical and electronic products.

- China’s foreign-currency reserves picked up for a second month, reports Bloomberg, following a seven-month losing streak. The article notes that a weaker U.S. dollar lifted the valuation of the hoard while capital outflows eased.

- China’s official manufacturing PMI rose to 51.8 in March, reports Reuters, beating forecasts, and up slightly from February’s 51.6 reading. The country’s official non-manufacturing PMI also rose to 55.1 from 54.2 in the previous month. (In contrast, the Caixin manufacturing PMI index edged down slightly lower to 51.2 in March from 51.7 in February.)

Weaknesses

- China’s plan to launch a special economic zone (the “Xiongan New Area”) in Hebei province, near Beijing, caused a rush of excitement this week and spurred a burst of optimism. A note from NSBO China, however, carefully cautioned that while certainly positive, progress may well be slower than expected and markedly different from areas like Pudong and Shenzhen. Expected constraints like heavy environmental and industrial controls, for example, ought to temper the wild optimism of earlier this week, while it remains noteworthy that the area is already well-connected by lines of transportation. Pollution control is still a key priority for the hard-hit northern province. In the end, while President Xi Jinping most definitely wants to ensure the success of the area, he likely does not want it rushed.

- Korean automakers had a weak month in March, reports Business Korea. Sales from the group, which includes Hyundai Motor Group, GM Korea, Renault Samsung Motors and Ssangyong Motor, were down 7.7 percent compared to a year ago. Total exports declined 9 percent.

- Beijing has promised to boost spending to cut down on its growing mountains of garbage and waste, reports Reuters, but the Chinese capital is having a difficult time persuading its residents to sort their trash. Beijing is China’s biggest municipal trash producer, and with the Asian nation’s 246 large- and medium-sized cities producing 1.9 billion tonnes of solid waste in 2015, government plans were spurred to cut landfill and step up recycling and incineration, the article continues. However, a lack of incentives to reward compliance and punitive measures for disobedience has hampered this goal.

Opportunities

- According to a recent Bloomberg interview, dividends are potentially a key lure for investors to Chinese stocks, with “stocks of companies that consistently hand out the most cash outperforming the Shanghai Composite Index.” Catherine Yeung, an investment director at Fidelity International, told Bloomberg reporters that she sees the trend continuing, boding well for Chinese companies from a foreign investment perspective.

- U.S. President Donald Trump met with China’s leader Xi Jinping late this week, with a number of important issues on the table, including trade policy, the South China Sea and North Korea, to name a few. In a Financial Times interview, Trump said that China will be rewarded with trade if they help with a solution for North Korea.

- One 25-year-old entrepreneur could provide Hong Kong with its first billion-dollar startup, reports Bloomberg. Tink Labs Ltd., which leases phones to travelers, is in the process of raising about $40 million and is aiming for a valuation of more than $1 billion, the article continues. The young company is aiming to have their smart phones available in 1 million hotel rooms by 2018.

Threats

- Earlier in the week, North Korea fired a ballistic missile off the coast of the Korean Peninsula, according to U.S. and South Korean officials. This is one of several that the country has test-fired over the course of several months, reports Bloomberg. Although the U.S. has been insistent that China place pressure on North Korea to stop its missile program, President Trump reiterated on Sunday that the U.S. would be prepared to act alone to stop the country if need be. North Korea is almost sure to be a topic of discussion at Mar-a-lago.

- Details are still forthcoming on the topics and results of discussions between Presidents Trump and Xi. While both leaders are making optimistic statements about the talks, Trump has made clear his view of China as a currency manipulator and in addition, the meeting may be somewhat overshadowed by North Korea’s recent missile test and the U.S. strike on Syria.

- China saw the first ever downgrade of a local-government financing vehicle (LGFV) by S&P Global Ratings, which cited the city in eastern Jiangsu province’s high debt burden, reports Bloomberg. It seems traders and analysts are worried about China’s local government debt again, with 18 of 29 polled in a Bloomberg News survey saying “they’d sooner buy corporate debt than LGFV bonds,” the article continues.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 3 percent. The country’s strong economic data supports an uptrend in equites. Gains on the Budapest stock exchange were led by Mol, a Hungarian oil & gas company whose shares appreciated by 4.5 percent, and OTP Bank which rose by 3.3 percent.

- The Czech koruna was the best performing currency this week, gaining 1.3 percent against the dollar. As expected, the Czech National Bank removed a policy that kept the koruna weaker than 27 per euro after inflation returned to target.

- The materials sector was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 50 basis points. Investors are cautious before next week’s referendum on the executive presidency. Gezici polls show “Yes” votes ahead for the April 16 referendum at 53.3 percent versus “No” votes at 46.7 percent. The polls also state that if participation in the referendum falls, “Yes” votes could increase to 56 percent.

- The Turkish lira was the worst performing currency this week, losing 2.3 percent against the dollar. Turkey’s lira, Russia’s ruble and South Korea’s won weakened the most as investors treated the three currencies as the most vulnerable to political risks after the U.S. carried out missile strikes on Syria.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- Final March PMI for the eurozone was reported at 56.2. That is a 71-month high despite the political uncertainty caused not just by Brexit and the economic policies of U.S. President Donald Trump, but also the upcoming elections in France and Germany.

- Russia’s March inflation was reported at 4.3 percent, the lowest annual reading since June 2012. The central bank wants to bring inflation to 4 percent in 2017, which would be the lowest year-end level in modern Russian history. “The oil price recovery and the outperforming ruble became a game changer for the inflation and monetary-policy outlook this year”, Morgan Stanley analysts said. They also predict that Russia will cut its main rate by 25 basis points at each of the next six meeting.

- European Central Bank (ECB) President Mario Draghi told economists that it is too soon to reduce stimulus, as the underlying inflation is still weak. Low rates and quantitative easing programs will continue to support European recovery.

Threats

- U. S. sanctions on Russia will remain in place until the nation calls off its annexation of Crimea, Secretary of State Rex Tillerson said last Friday. According to survey of 20 economists conducted March 28 to March 30, just one in four said the U.S. will ease sanctions in the next 12 months, down from 60 percent in the prior survey.

- Wood & Company does not predict significant appreciation in the Czech koruna. Investors have been anticipating removal of the cap on the currency, and there is a sizeable bond positioning that will be gradually liquidated. Beyond 3-4 percent appreciation a year the Czech central bank will begin to question whether it is sustainable for the fundamentals of the economy. A rate tightening cycle could start in the second half of this year.

- U.S.-Russia relations are deteriorating further over policy disagreement in Syria .The U.S. blamed the Bashar al-Assad regime for the chemical attack in the northwest province of Idlib that killed more than 70 people. Russia accused President Trump of rushing to judgment and challenged U.S. to present a better strategy in Syria. Then the U.S. launched about 60 missiles against a Syrian air base, and Vladimir Putin called the strike an act of aggression.