The wild ride of Netflix, Inc. (NASDAQ:NFLX) shares continues. After plummeting from above $300 a share to around $60 all within the past year mostly due to poor management decision. Netflix shares spiked more than 21% in one week to close at $81.89, the highest level in two months, on Friday July 6.

Netflix is not scheduled to report its full earnings for Q2 until after the market close on July 24. Rather, this latest renewed enthusiasm came primarily from an upbeat Facebook update by CEO Reed Hastings:

“Netflix monthly viewing exceeded 1 billion hours for the first time ever in June. When House of Cards and Arrested Development debut, we’ll blow these records away.”

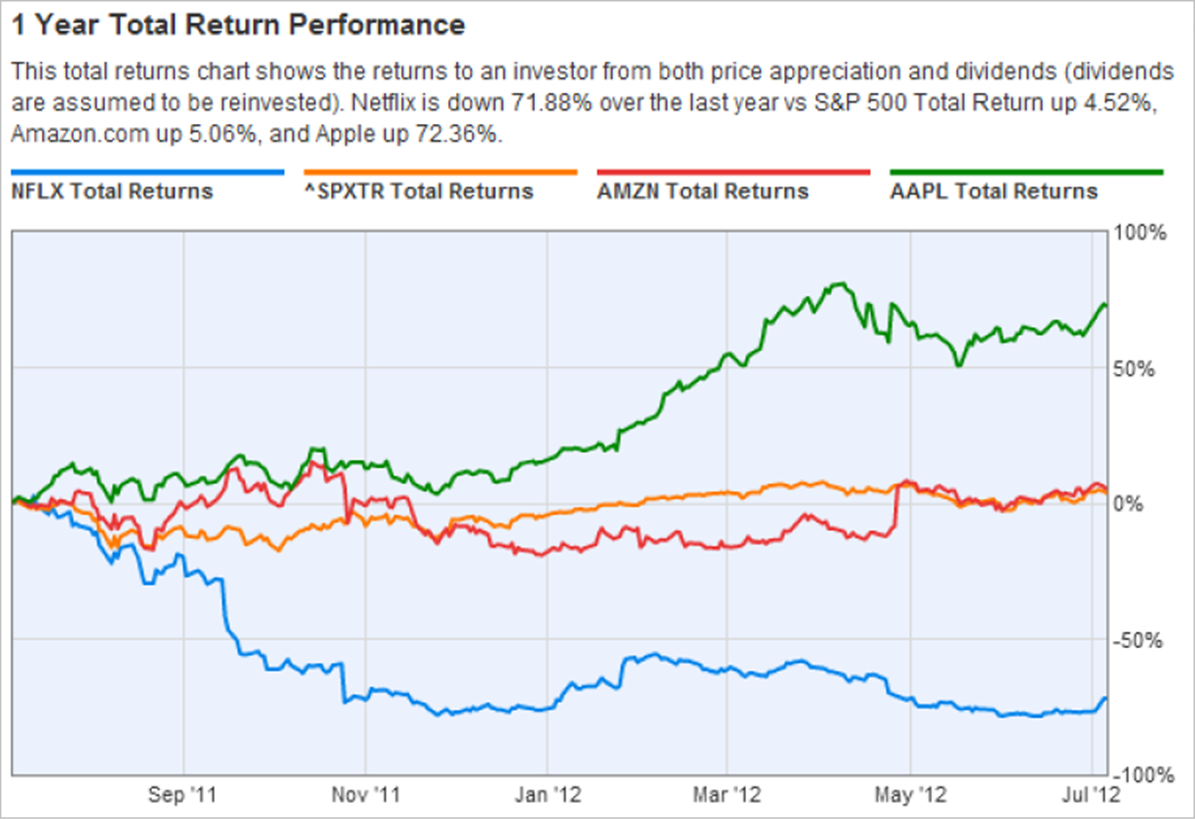

The stock also got a bump after Citigroup reiterated a ‘buy’ rating on Netflix shares, calling the price “highly reasonable” with a target of $130 a share, about 56% from the current level. Judging from the price movement, the unexpected buying action most likely also resulted a massive short squeeze. (Hastings’ Facebook page has almost 206,000 subscribers.) Nevertheless, Netflix shares are still down 26% in the last three months and off 72% in the past year.

Netflix has been beefing up its program offerings by acquiring exclusive content to stay competitive with rivals like Amazon.com, Inc. (NASDAQ:AMZN), Apple (AAPL), Hulu and Comcast (CMCSA). Bloomberg reports that Netflix said in January that viewing in Q4 of 2011 totaled just over 2 billion hours. So this new figure of one billion viewing hours in June alone does seem to suggest a faster growth rate for Netflix streaming service.

Nevertheless, since Netflix streaming service charges a flat fee per month, at least part of the increase in total hours could come from an increase of viewing hours per subscriber, which is actually bearish for the stock. So the one billion monthly streaming hours reflects more the content and marketing strength of Netflix, rather than a compelling story of the bottom line or growth in a very competitive market sector.

Fundamentally, a more troubling picture also emerges with a look at the company’s balance sheet. For the quarter ending March 31, 2012, the company has $804.5 million in cash, but $1.45 billion in current liability, with a scant quick ratio of 0.6, and a current ratio of 1.4, barely above the minimum threshold of 1.

Then there is also this $3.7 billion off-balance liability buried deep in the company’s 10Q filing. Based on a Bloomberg review, these off-balance liabilities are the minimum estimates (i.e., the actual could be a lot higher) for payments due for future contents already under contracts. Out of the $3.7 billion, $3.1 billion will come due within three years. Including this $3.7 billion, Netflix Debt-to-Capital would balloon to 618% from the current 60.3%!

From a valuation standpoint, since profit will likely get squeezed pretty hard with the company’s ambitious international expansion plan, Netflix stock looks over-valued with a current forward P/E of 38.63. For comparison purpose, the same ratio for Nasdaq 100 is 13.78, 12.95 for S&P 500, and under 12 for both Apple and Google. I guess Netflix share price is only “highly reasonable,” as described by Citigroup, if you compare it to the high flying stocks like Amazon, which has a forward P/E of 87.67.

|

| Chart Source: Ycharts.com, July 6, 2012 |

For now, Netflix does appear to be the leader of the video-on-demand (VOD) pact primarily benefiting from the first mover advantage. However, competition is becoming fierce and cut-throat. It looks like cable companies are getting anxious to punish Netflix for its sins of free-riding on their expensive fiber optic network. For example, in a clear declaration of war against Netflix, Comcast recently announced its intention to offer a similar service as Netflix, albeit with a much weaker library, for $5 per month, and many free movies to its Xfinity subscribers. Amazon Prime offers streaming video in addition to expedited shipping for $79 annually. Not to mention sooner or later, tech giants like Apple Inc. (NASDAQ:AAPL) and Google Inc (NASDAQ:GOOG) will start throwing cash around, and get more aggressive in this space as well.

Ultimately, “content is king” in this sector. So it is doubtful Netflix would keep getting exclusive contents, and maintain its lead in the long run, considering most of Netflix major rivals are equipped with much deeper pockets.

The self-congratulatory social media update from the CEO seems a bit pre-mature to suggest an entry into the stock. We maintain our recommendation to stay away from this stock, as there are more compelling stocks to invest in with either better growth, and/or value prospect.

For investors got in during the past week, instead of holding to Citigroup’s bullish-biased $130 target, it’d better to gradually cash out, since the stock most likely will have higher volatility going into the earnings next month.

Disclosure: No Positions

Via EconMatters