Muddy Waters Capital LLC (“Muddy Waters”) is an investment advisor to private funds. Muddy Waters has analyzed the U.K.-listed company IQE plc (“IQE”) and is hereby publishing the outcome and the conclusions of our analysis, which is based on publicly available information. Funds Muddy Waters manages are short shares of IQE and for this reason there might be a conflict of interest.

Muddy Waters is Short IQE plc (AIM: IQE LN)

Muddy Waters Capital LLC is short IQE. IQE is, in our opinion, an egregious accounting manipulator.

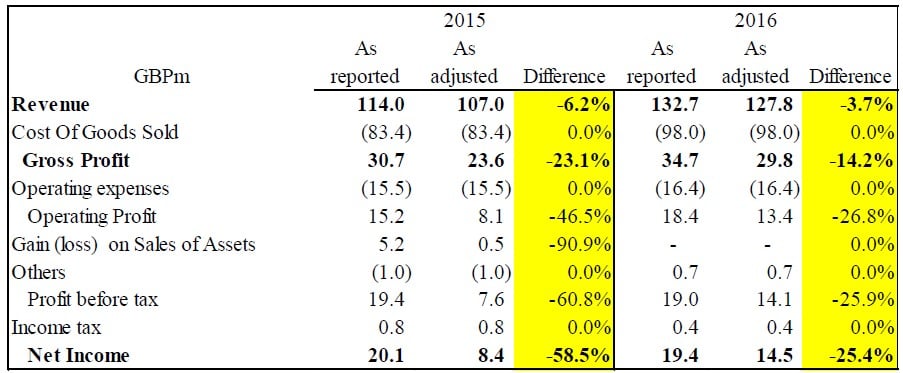

In August 2015, IQE formed a 50/50 joint venture with Cardiff University called Compound Semiconductor Centre Limited (“CSC”). In our analysis, IQE received substantial, but unsustainable, accounting benefits from CSC, at the cost of millions of pounds to the university. We adjust downward the company’s reported net income for 2015 and 2016, respectively, by 58.5% and 25.4%. We believe it is reasonable to adjust 1H 2017 net income down by approximately £5 million or 69% to account for likely aggressive capitalization of expenses.

On February 2nd, a firm called ShadowFall circulated a report criticizing IQE’s accounting for two joint ventures. IQE responded on February 5th, calling the contents of the report “without merit” and “misleading”. Our research has been independent of ShadowFall, and ShadowFall’s report does not address the vast majority of the issues with IQE’s accounts we have identified.

The 2015 and 2016 adjustments reflect our belief that IQE’s transactions with CSC are not substantive, and the accounting is possibly designed to deceive investors. We estimate that when IQE booked gains on transferring PP&E to CSC, it transferred the PP&E at a valuation 4.6x carrying value. This markup strains credulity. We call upon IQE to release the purportedly independent valuation report in full, and we will publicly opine on it (even if it convincingly supports the valuation). IQE was CSC’s only customer through 2016, and CSC generated an abysmal negative -105.9% gross margin! (It is almost amazing anyone would claim that it “holds itself to the highest standards of corporate governance, transparency, and integrity” with a straight face under these circumstances.1)

We identify five previously unknown issues with the accounting for transactions between IQE and CSC. Time and again, IQE seems to be employing “having one’s cake and eating it too” accounting. We feel that IQE dominates CSC, and CSC is therefore likely an alter ego for IQE.

We believe IQE began aggressively capitalizing expenses in 1H 2017. CSC’s funds were largely exhausted by the end of 2016, and we suspect IQE was desperate for some more earnings magic. We note that insiders, who presciently purchased a substantial number of shares just before the JVs’ accounting benefits began flowing to IQE, sold millions of pounds of stock around the end of 1H 2017. These sales could be a sign that IQE’s ability to generate profits has hit the wall as the result of the exhaustion of its financial engineering options.

Egregious Manipulation through CSC

Companies House filings state that “CSC’s mission is to provide Europe’s first prototyping facility dedicated to enabling businesses and academics to demonstrate new technologies based on compound semiconductor materials that will be production ready…” In addition, CSC is theoretically tasked to “facilitate a wide range of training and skills development to support a growing demand…” for technologies. Cardiff University has invested £23.8 million cash in CSC, including a £2.0 million loan and an additional £0.8 million investment in the first seven months of 2017. In contrast, IQE invested zero cash – it received its interest in exchange for contributing unspecified PP&E and intangible assets. We estimate the PP&E contribution was valued at 4.6x of its carrying value, which is one of several facts giving us concern that IQE might have taken advantage of Cardiff University.

We adjust downward IQE’s 2015 and 2016 net income by 58.5% and 25.4%, respectively, to exclude gains on transfers of assets to CSC, which we believe lack substance

These adjustments also bring the gross margins in line with those of prior periods.

To neutralize the effect of disposal and license transactions with CSC on IQE’s historical financials, we

make the following adjustments:

- reverse IP licensing revenue of £7.07 million and £4.93 million in 2015 and 2016, respectively, which carried a 100% operating margin, and

- reverse the realized £4.714 million gain on disposal of PP&E in 2015

In 2015 and 2016, IQE booked gains from transferring PP&E and licensing IP to CSC. In our opinion, these gains are misleading as to the economic health of IQE, and we accordingly adjust IQE’s financials to exclude them. We have identified issues with both the PP&E and IP transactions and accounting.

We estimate that the valuation given to the PP&E IQE transferred was 4.6x its book value, which is suspicious on its face. However, we have identified five accounting issues that solidify our doubts about these gains, and which cause us to believe that IQE’s accounting is egregiously manipulated through transactions with CSC. IQE insiders’ significant sales in mid-2017 – just after CSC seemingly lost its ability to boost IQE’s accounting profits – lend additional weight to our conviction that the transactions with CSC are manipulative and should be disregarded.

The five accounting issues that cast doubt on the substance of the gains from transacting with CSC are:

- CSC’s accounting for the transactions is inconsistent with that of IQE, which is problematic given the overlapping managers and directors between the companies. The having one’s cake and eating it too treatment suggests IQE is inappropriately accounting for these transactions.

- IQE has its cake and eats it too in yet another manner when accounting for transactions with CSC by selling to it at purportedly market (i.e., arms-length) prices, yet buying from it at cash cost (well below market / arms-length prices).

- IQE’s recognition of certain of these gains from these transactions in 2015 and 2016 is wholly inconsistent, leading us to conclude that at best, there is a concerning amount of arbitrariness to IQE’s accounting; and, at worst, its accounting is intended to deceive investors.

- CSC has lost prodigious amounts of money (and burned through substantially all the cash Cardiff University invested through 2016), yet IQE’s income statement has been immunized against recognizing its share of these losses through accounting we believe is highly aggressive. Once again, IQE is having its cake and eating it too by booking (highly questionable) material gains from CSC without recognizing its losses. (Note that we do not adjust IQE’s earnings downward for its share of CSC’s losses, which would effectively be double counting.)

- Our diligence leads us to believe that CSC is likely non-substantive and effectively an alter ego of IQE, supporting our view that IQE’s economic reality is more appropriately understood by adjusting for the transactions with CSC.

We estimate IQE’s PP&E contribution to CSC was valued at 4.6x its carrying value, straining credulity

In H2 2015, IQE realized a £4.7 million gain on the disposal of the contributed PP&E, which was equivalent to 30.1% of its net income during the period. IQE showed carrying value of all PP&E of which it disposed during the period as £3.4 million, and disclosures specific to the PP&E contributed in exchange for the £12.0 million equity stake imply IQE carried the PP&E at only £2.6 million. (Note that under IAS 28, IQE may not recognize a gain on the portion equal to the percentage owned by the transferor, which in this case is 50%. If we subtract £9.4 million (2 x £4.7 million) from £12.0 million, it implies the carrying value of the PP&E valued at £12.0 million was only £2.6 million.)

IQE noted in its response to ShadowFall that it engaged an “independent” valuation firm to determine the “market value” of this PP&E. Unlike audits, such valuation reports are not generally governed by statutory duties to public companies or their shareholders. In our past work, we have found numerous third-party reports to be merely fig leaves to justify egregious accounting (e.g., Noble Group Ltd.). We generally take purportedly independent valuation reports with a grain of salt; therefore, we call upon IQE to release the full valuation report used to support the £12.0 million figure. Should IQE release the report, we will publicly opine on it, even if we believe it convincingly supports the valuation (this is a serious offer).

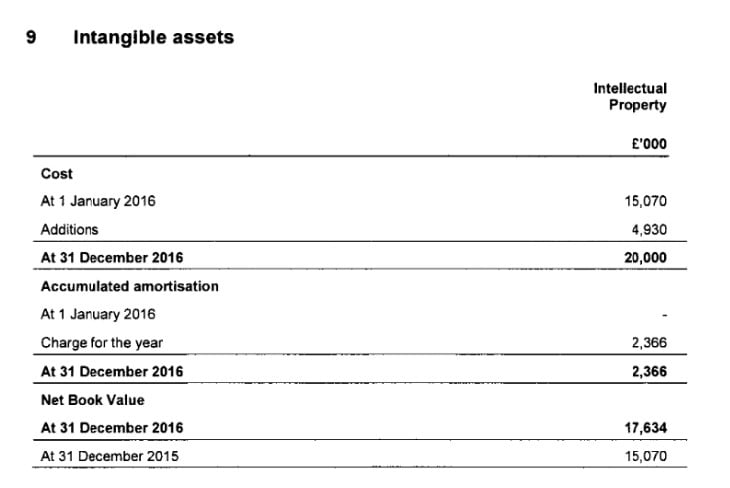

IQE transferred intangible assets to CSC, which were valued at £20.0 million. In the ShadowFall response, IQE once again tells us that the valuation was supported by a third-party report. It would be far more difficult for us to sanity check this type of valuation report, but we certainly think that releasing it would serve the public interest, given the government money invested. Regardless, given the totality of accounting issues we observe, we believe it prudent to disregard these gains.

Accounting Issue 1 – CSC’s accounts call into question IQE’s revenue recognition and gross profit

IQE recognized IP licensing revenue from CSC of £7.7 million and £4.9 million, respectively, in 2015 and 2016. CSC’s accounts do not appear to support this treatment because CSC capitalized these payments as investments in intangible assets, and amortizes them over seven years on a straight-line basis. This divergent accounting treatment benefitted IQE’s 2015 and 2016 reported revenue and gross margins. It simultaneously benefitted CSC by decreasing its reported loss through less aggressive expensing (i.e., seven-year amortization). Had IQE’s treatment reflected that of CSC, it would have instead recognized gains on sale, which would not have improved top-line revenue and gross margin. The fact that such closely-connected entities are engaging in having one’s cake and eating it too accounting is one reason we believe the gains are non-substantive and should be disregarded.

CSC’s capitalizes the IP transactions as purchases of intangible assets – see CSC’s 2016 AR, p. 26:

Article by Muddy Waters

See the full PDF below.

{kind=link}