Lululemon (NASDAQ:LULU) rallies after topping estimates for the holiday quarter, posting strong guidance”. This was one of the headlines that broke shortly after the athleisure company released its fiscal Q4 earnings on Tuesday evening and which summed it up nicely. They reported that comparable sales rose 23% which was well ahead of the consensus, while revenue was in-line with year-on-year growth of 23%. The two-year revenue comparisons were also in focus as these skip the volatility of the pandemic, and showed 50% revenue growth and 46% net income growth. Lulu’s earnings per share comfortably beat analyst expectations as well, to round off what can only be called a solid report.

Q4 2021 hedge fund letters, conferences and more

After trading up nearly 4% in Tuesday’s session in anticipation of the release, their shares jumped in the after-hours session and were up another 8% in Wednesday’s pre-market trading. Wall Street, while happy with the headline figures, seems to have been particularly impressed with management’s forward guidance. Lululemon reported that for the full year, they expect FY22 revenue of $7.49 billion to $7.615 billion versus $7.24 billion and EPS of $9.15 to $9.35 versus the $9.05 consensus.

Upside Surprise

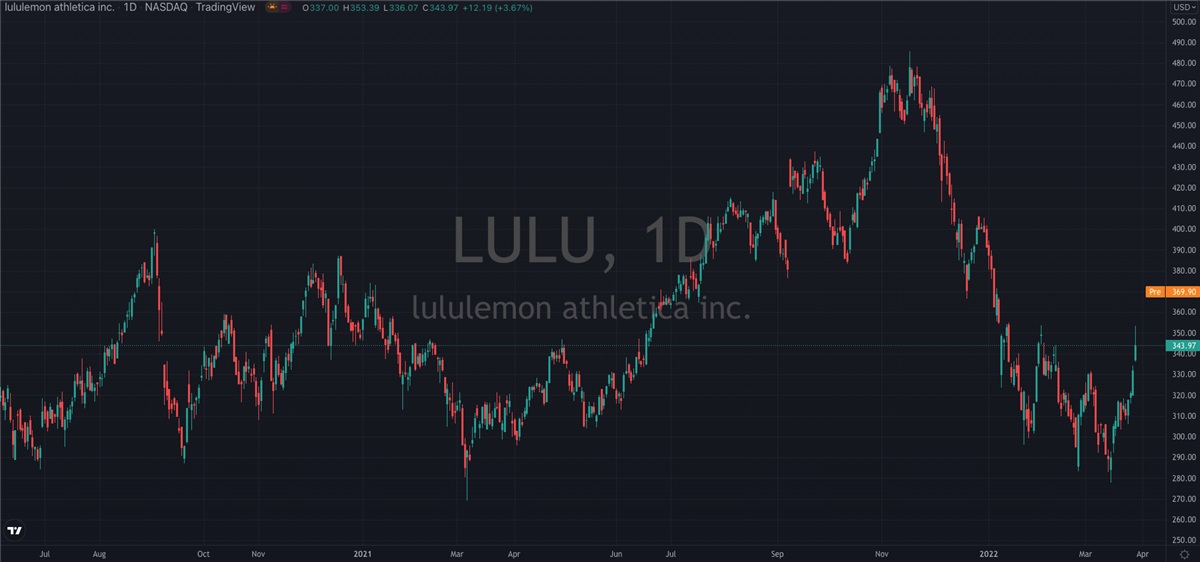

These kinds of upside surprises are exactly what bulls want to see in quarterly earnings reports, and are made all the sweeter when a company’s stock has been under pressure in the weeks leading up to the release. This is certainly true of Lulu. Coming into the middle of this month their shares were down more than 40% from last November’s all-time high. It’s fair to say we can expect the next few sessions to start eating into this downtrend given it doesn’t look like the worst-case scenarios will come to pass. In fact, they’ve already rallied as much as 25% from this month’s low, suggesting that more than a few were starting to suspect this week’s earnings report held a surprise in store.

Lululemon CFO Meghan Frank was justifiably upbeat on the company’s outlook, saying “our results were driven by consistently strong performance across our products, channels, and regions. In addition, for both the fourth quarter and full year, we delivered revenue growth above our Power of Three goals, despite the continued impact of COVID-19 and global supply chain issues. We are pleased to see our momentum continue at the start of 2022 and are optimistic about our performance for the year ahead.”

Not only do investors have impressive revenue growth acting as a tailwind, but the latest announcement of a $1 billion share buyback plan is also only going to bolster the bull’s case for the foreseeable future. Companies typically only purchase back their own shares when they think they are chronically undervalued to fair value, and it’s a signal to the market that management is willing to put its money where its mouth is.

Getting Involved

There’s a lot here for those of us on the sidelines to be considering. Lulu was one of the standout performers of the pandemic, putting even some of the high-flying tech stocks to shame with their 270% peak to trough rally. It turns out people love to wear comfortable clothes when stuck at home, who knew? While their shares have certainly suffered in recent months as market sentiment has turned away from high growth stocks and into value, Lulu is still in as strong a position as it’s ever been. Their digital business is robust, while time and time again footfall at their stores has been among the quickest to bounce back from any COVID-related bumps.

BTIG picked up on this trend earlier this quarter when they reiterated their Buy rating on Lululemon shares, and assigned a fresh price target of $489. From where shares closed on Tuesday, this suggests there’s an upside to be had in the region of 40%. This should be enough to tempt in even the more value-focused investor, as the recent sell-off has only widened the buying opportunity here. With a clear exit point below the recent low of $280, the risk-reward profile is as good as it gets in growth stocks right now.

Should you invest $1,000 in Lululemon Athletica right now?

Before you consider Lululemon Athletica, you’ll want to hear this.

MarketBeat keeps track of Wall Street’s top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on… and Lululemon Athletica wasn’t on the list.

While Lululemon Athletica currently has a “Buy” rating among analysts, top-rated analysts believe these five stocks are better buys.

Article by Sam Quirke, MarketBeat