LRT Global Opportunities commentary for the month ended February 28, 2019, cautioning investors not to buy the best companies nor the fastest growing ones, but the companies that are the most undervalued.

Dear Friends & Partners:

The value of our investment partnership continued its rapid climb during the month of February. Our performance this month was helped by strong returns from our top positions: AutoZone, Danaher, Colliers, NVR and Heico. While short term results are inherently volatile and our returns year-to-date should not be extrapolated, we continue to expect good performance from our portfolio over the remainder of the year, as many of our portfolio companies remain significantly undervalued.

[klarman]Q4 hedge fund letters, conference, scoops etc

We are invested in companies with durable competitive advantages, possessing above average growth opportunities, and led by management teams with outstanding records of capital allocation. All our portfolio companies have pricing power, high %’s of recurring revenues and are price setters. As a result, we expect the businesses that we own to perform substantially better than the average company in the event of a recession. We anticipate a slowdown in the macroeconomy and continue to be defensively positioned – as expressed by the quality and durability of the companies we own.

Our results have been volatile over the recent past, but they are a good illustration of the upside that comes from having a sound investment strategy and the disciplined execution of said strategy. Over the past three months, an investor in the S&P500 would have realized a sharp loss in December followed by a rapid recover in January and February which together added up to an approximately flat performance over the entire period. Our investment partnership, on the other hand, is far ahead over the past three months – despite suffering a sharp decline in December.

In our December letter to you we wrote:

In the current environment stocks are very attractive – because they reflect a deep pessimism about the future of the economy and corporate earnings. We believe that such pessimism is unwarranted – long term investors should be buying equities. Our Partnership is doing just that.

This is what we mean when we say that we are committed to the “disciplined and consistent” execution of our investment strategy. In late December we had no way of knowing what the next two months would bring – instead we chose to focus on company fundamentals and our steadfast commitment to our portfolio execution. While all the talking heads on TV were predicting lower stock prices, and while almost everyone was selling stocks, we were buying equities. We believe that a disciplined execution of a rigorous investment process is the best way to protect capital and generate portfolio performance. Over the past two months we have been reaping the benefits of this discipline. We are happy with the performance of our partnership but remain vigilant in identifying risks and threats to our investment process. With that we would like to give you some insight into what lies ahead.

An Economic Update

Over the past two years, the US government pumped record amounts of fiscal stimulus into the economy by taxing less and spending more. Specifically, spending on defense and US fiscal borrowing has risen. This stimulus cannot and will not repeat in 2019/2020. As the fiscal stimulus from the last two years fades, economic growth will slow, especially in the manufacturing sectors which has benefited dramatically from increased defense spending.

In recent months, Federal tax revenues have been growing at the slowest rates outside of a major recession in the past four decades according to the Monthly Treasury Statement data. It is clear, that reduced US tax rates have more than offset the impact of an expanding economy as US tax receipts fell in 2018, as compared with the prior year. This should put to rest the lie of tax cuts that pay for themselves.

Meanwhile, US government spending has continued to rise at a rate close to its long-term average. In fact, federal outlays increased by more than 4% last year as compared with 2017. Combined, this has amounted to a major fiscal stimulus to the US economy – no wonder that GDP growth has been strong. Did the US economy really need a massive fiscal stimulus eight years into an economic expansion and with unemployment already at multi-decade lows? We believe the answer is an empathetic: NO.

The US economic expansion is now well into its final inning. We continue to expect a rapid deacceleration of US economic growth in the first half of 2020 as the sugar rush of tax cuts and increase government spending dissipates and leaves us with its painful aftermath: higher inflation and higher interest rates. We believe investors should be increasingly selective in the investments they make and prepare for a recession ahead. Now is a time to seek safety, stability and simplicity in one’s investment approach. As the economy slows, corporate profitability declines and many overvalued companies fail to live to their expectations, we will finally see, in the words of Warren Buffett, “who is swimming naked”. We expect our investment strategy, which takes an active approach and focuses on analyzing company fundamentals, will be well rewarded in the months ahead, as the decline in the overall market presents us with an expanded opportunity set to invest capital at attractive valuations.

Moats, Growth and Valuation

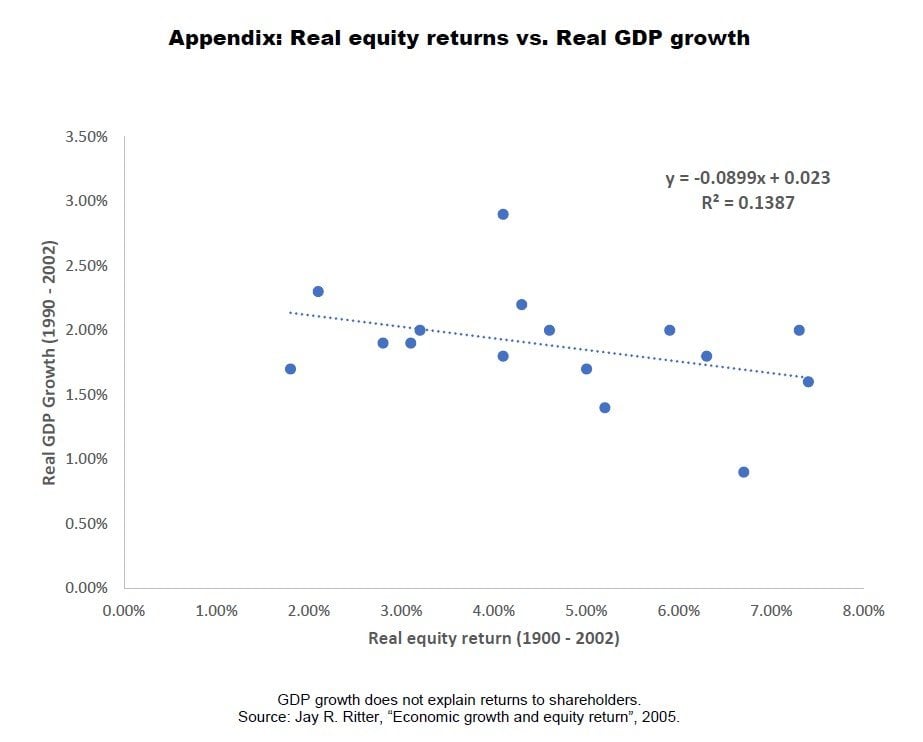

Forecasting economic growth is an obsession on Wall Street and amongst TV pundits because in the short-term, correctly calling a recession can lead to significant outperformance, yet over the longer term, stock market returns have nothing to do with economic growth. This may sound surprising and counter-intuitive, but it is supported by extensive research. A comprehensive study by Professor Jay Ritter, from the University of Florida, Gainesville, clearly shows that stock market returns are not driven by GDP growth. In his 2005 paper, “Economic growth and equity returns professor” Ritter found a small, but negative relationship between GDP growth rates and stock market returns. In the second paper, published in 2012, “Is Economic Growth Good for Investors?” Ritter shows that investors systematically overvalue stock markets of economies with high expected GDP growth rates and that this “overpayment for growth” more than offsets any gains from faster growth. This is remarkably like the well-known “glamour effect” in the stock market, where investors are known to pay unreasonably high valuations for “the best” companies – the definition of “the best” depending on the investment fad of the day.

What is true at the level of the economy at large can be translated to the level of an individual firm. Growth at the firm level benefits investors only if there are durable barriers to entry that can prevent competitors from reducing a company’s profitability. For most firms, growth leads to increased profits and increased profits attract competition which in turn leads to lower profits. Some firms, however, have beaten the odds – they have been able to sustain high profitability for many decades. These firms have something unique about them – they have a sustainable competitive advantage, or what others sometimes refer to as a moat. Absent a moat, high profits will be competed away, and growth is unlikely to benefit investors.

In today’s letter, we hope to give you some insights in the relationship between a firm’s moat, its growth rate and its valuation. We see persistent market inefficiencies in how investors assign value to companies in at least three broad areas: companies with a moat and no growth, companies with growth and no moat, and companies with a moat and fast growth but priced to perfection (overpriced). While the degree of inefficiency varies with the changing market mood, all three of these areas are fertile hunting grounds for active managers looking to add value.

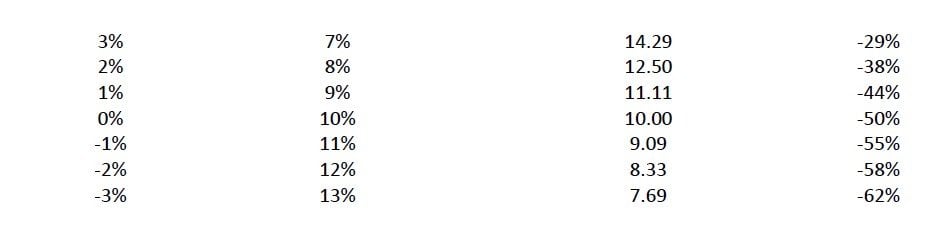

Most consumer staple companies in the United States have “legacy moats”, but no growth. Despite this they remain valued very highly as a group. We believe this is a mistake, as their moats are eroding and barriers to entry are declining, leaving them overvalued as a group. In previous letters, we have discussed the declining value of brands, the erosion of some of these legacy moats, and how we expect most companies in this category to have downsides of 30-50%. The erosion of these legacy moats will not mean a sudden collapse, but rather a slowdown in growth which should translate into a lower valuation. For a mature, slow growing company, even a small change in the rate of growth means a big change in valuation. Let us look at some math.

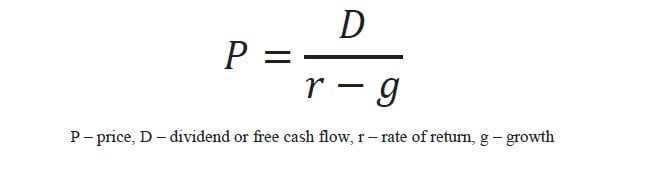

One of the most basic valuation formulas in finance is the Gordon Growth Model. This model is appropriate for valuing slow and steady companies like most consumer staples with limited reinvestment opportunities. The formula is as follows:

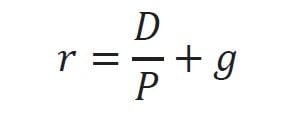

We can rearrange the formula to solve for the rate of return.

Hence, the return to investors is the current free cash flow yield (free cash flow divided by price) plus growth. Historically, the nominal return on US stocks has been approximately 10%. The rate of return investors demand for holding stocks fluctuates with market sentiment, but if we assume that over the long-term historic patterns repeat themselves we can set r = 10%. Since, D (the current free cash flow) is known, there are only two variables left to deal with. The lower the growth rate (g) is the lower price (P) must become (since D/P must rise). We can therefore calculate the fair value for a company and its change as we change the expected growth rate.

Careful readers of our investment letters will note that we have been warning about the danger of “safe” consumer staple stocks for quite some time now. We believe that our predictions are finally coming true. Over the past three months, Budweiser cut its dividend in half in a bid to help the company reduce its debt burden. Kraft-Heinz wrote down billions from the value of some of its best-known brands and reduced its dividend, in order to, “…provide greater balance sheet flexibility,” per management’s comments. Dean Foods suspended its dividend completely. Coca-Cola missed earnings expectations and said it expects no growth in earnings-per-share in 2019. We expect more such news over the coming months. “Safe” consumer staples have become a dangerous minefield.

For more on the topic of legacy moats lacking growth, please see the excellent blog post by Sean Stockton from Ensemble Capital, available here: https://intrinsicinvesting.com/2019/02/22/the-risk-of-low-growth-stocks/. We also encourage you to visit our YouTube channel and see some of the videos we have produce on this topic, specifically: Yesterday’s Home Runs Don’t Win Today’s Games and Reaching For An Aspirin.

The second area of persistent inefficiency that we see are stocks that are growing but have no moat. These companies are often highly valued as if they will soon take over the world and become sustainably profitable. Most investors either don’t understand the concept of a sustainable competitive advantage, don’t care about profitability beyond the immediate few quarters, or are “hoping” that a company will develop a competitive advantage as it grows. This issue is best illustrated with an example.

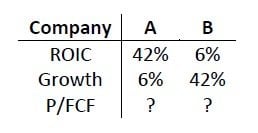

Imagine two companies: the first with high and stable returns on invested capital (ROIC), a pretty good indicator of a sustainable competitive advantage, but with low growth; the second company with low ROIC but high growth. Furthermore, assume that both companies can reinvest at the stated ROIC and growth rates for the foreseeable future. How would you value these two companies?

A few things stand out when looking at this table. First, Company B needs external financing to grow – its internal returns are too low to finance all its growth opportunities. Company A on the other hand can grow and return cash to shareholders because of its very high profitability relative to its limited growth opportunities. Which company would you rather own? This should be obvious, but to many investors it is

not. Let us dispel any illusions you may have: in the case of Company B, growth creates no value. Investors are WORSE off when the company grows. A six-percent return is terribly low for an equity investor. If you take as given the assumptions we laid out, that both growth and ROIC are stable, then Company B is actively destroying value by growing. A business earnings 6% on tangible capital should trade below book value.

Company A, on the other hand creates enormous value for shareholders when it grows. At LRT we are only interested in companies whose growth creates value. You can justify paying a price of more than 10 times the tangible invested capital that Company A employs. Often, markets work efficiently and value Company A very highly and Company B much lower. However, often does not imply always. On more than one occasion in the past, a business similar to Company B, has received a very high valuation in the marketplace as investors seemingly only focus on the company’s growth rate.

We said, “imagine two companies”. You don’t have to imagine. While facts and time periods are stylized, the companies are real. Company A is Spirax-Sarco PLC, a manufacturer of industrial boilers and related steam management products. The industrial boiler market is not particularly big, exciting or fast growing – but it is a market that delivers Spirax-Sarco PLC an exceedingly high return on invested capital. Company B is Groupon, the worldwide e-commerce company. Spirax-Sarco PLC, has been around since 1888 and publicly listed for over thirty years. Groupon is a newer company, having gone public a little over seven years ago. Did the market asses the future growth and value creation of these two companies correctly? We contend that it did not. If it did, the return earned by the shareholders of both companies should have been similar over a long-time period.

Spirax-Sarco PLC delivered a compounded annual return of 32%, 21% and 19% over the past 3, 4, and 5 years, respectively. Groupon delivered -7%, -20% and -17% over the same respective time periods. There has been no meaningful change in either company’s business model over that time period or a significant recession in either company’s end markets. We believe that market participants simply fail to account for the significant value creation that comes from a high and stable return on capital combined with slow but steady growth. Similarly, investors overpay for the growth opportunities presented by companies such as Groupon, despite their lack of sustainable competitive advantages. Careful readers will assert that the return on equity should also reflect a company’s riskiness. Taking this into account makes the gap between reality and theory even wider as Groupon is by far the riskier company and should have therefore delivered a higher return than Spirax-Sarco PLC. Spirax-Sarco PLC has had a beta of 0.54 over the past five years. Groupon’s beta over the same time has been 1.18.

Each individual company is different making a rigorous “study” impossible, but the pattern is persistent: slow and steady growing companies with high return on invested capital tend to be undervalued by market participants, while super-fast-growing companies lacking competitive advantages tend to be overvalued. It is a pattern we see over and over again in the market at large. Note, that we say “tend to” as there are many cases where the market does get it right. There are also cases where we believe things go too far – when market participants assign such a high value to a company that all future “abnormal returns” appear to be priced in.

This brings us to the third category: companies with moats (strong and durable competitive advantages), strong growth, but absurd overvaluations. As investors, we caution not to buy the “best” companies nor the fastest growing ones, but the companies that are the most undervalued. While we believe that many high return and slow growth companies remain undervalued today (even though they may look “optically” expensive), the same cannot be said for wide-moat and high growth companies. The supply of companies that combine having of a wide-moat and fast growth is very limited. Investor appetite on the other hand is so high for companies with said characteristics that we believe many investors are consciously overpaying for these businesses, disregarding fundamental valuation or simply chasing momentum. Anyone investing

in an obviously overvalued company, in the hopes of selling it on to another person at an even higher valuations, the so called “greater fool” investment strategy, is one himself.

If a company’s starting valuation is high enough, a business can perform perfectly and still deliver poor returns to shareholders. Investors chasing profitable growth must not overpay or they may find themselves chasing a bubble. When the bubble bursts, many shareholders will become “bagholders” – nursing heavy losses. Fundamentally oriented investors should avoid investing in such companies – no matter how lucrative short-term, momentum driven gains, may appear. We believe that most public Software-as-a- service (SaaS) companies meet this definition today.

Let me demonstrate my point with a concrete example. Consider what we call a “Bubble Basket” consisting of thirty-four (34) popular publicly traded SaaS companies. The full list of names in our Bubble Basket is included at the end of this letter. The companies in this index have delivered handsome results to shareholders over the past few years. Many are still unprofitable on a GAAP basis but are growing quickly and as a result are valued very highly by investors. We believe that many of these companies will deliver excellent profitability in the future, but that investors will fare poorly over the next three years because the current nose-bleed valuations make it almost impossible for the companies in question to meet the expectations embedded in their stock prices. Since many of these businesses are not yet profitable, they tend to be valued on a price-to-sales basis (P/S). Our Bubble Basket has a min, max, mean and median P/S of 3.52, 24.21, 11.84 and 10.23 respectively.

Each of the companies in our basket has a compelling story, high growth, and meaningful opportunities to reinvest capital and create value. Some of these companies will exceed expectations and deliver strong returns to shareholders, but as a group we expect them to be a disappointment. Collectively, these companies are so highly valued that there is little to no chance that they will outperform the market. Because the starting valuations are so high, even if everything goes according to plan, returns to shareholders are likely to be mediocre at best over the next three years. We believe that many investors own these stocks simply because of the strong recent price performance – they are classic momentum stocks. We expect that these stocks will collapse the fastest and collapse the most in the event of a true bear market. Investors holding these stocks will fail to protect their capital. Prudent investors should steer clear – which is exactly what are we doing.

In summary: we expect a recession and a bear market sometime in the next eighteen (18) months, driven by a sharp slowdown in US GDP growth (caused partially by the decline in fiscal stimulus and rising interest rates) and an associated sharp decline in corporate profitability. Furthermore, we see a high probability of further declines across the consumer staples sector, as investors adjust to the new (read: much lower) growth rates and associated low valuations for most companies in this group. Finally, we are warning anyone who will listen that the valuations of most SaaS business are extremely stretched – even if the businesses grow as expected, investors may not profit due to their very high valuations.

As always, I look forward to answering your questions.

Lukasz Tomicki

Appendix: The Bubble Basket

The companies in the Bubble Basket are: Benefitfocus, Inc. (BNFT), Box, Inc. (BOX), Coupa Software Incorporated (COUP), salesforce.com, inc. (CRM), Cornerstone OnDemand, Inc. (CSOD), Tableau Software, Inc. (DATA), DocuSign, Inc. (DOCU), Domo, Inc. (DOMO), Eventbrite, Inc. (EB), HubSpot, Inc. (HUBS), Instructure, Inc. (INST), LogMeIn, Inc. (LOGM), Medidata Solutions, Inc. (MDSO), ServiceNow, Inc. (NOW), Anaplan, Inc. (PLAN), Qualys, Inc. (QLYS), RingCentral, Inc. (RNG), RealPage, Inc. (RP), Rapid7, Inc. (RPD), Splunk Inc. (SPLK), SVMK Inc. (SVMK), Atlassian Corporation Plc (TEAM), The Trade Desk, Inc. (TTD), Twilio Inc. (TWLO), 2U, Inc. (TWOU), The Ultimate Software Group, Inc. (ULTI), Veeva Systems Inc. (VEEV), Workday, Inc. (WDAY), Wix.com Ltd. (WIX), Zendesk, Inc. (ZEN).

We began our Bubble Basket experiment on 3/1/2019. We assume an equally weighted portfolio and will update the portfolio’s hypothetical performance each month. We expect the portfolio to underperform the S&P 500 over the next three years, with significantly higher volatility.

Further Reading

Economic Growth and Equity Returns, Jay R. Ritter, EFA 2005 Moscow Meetings Paper

Is Economic Growth Good for Investors?, Jay R. Ritter, Journal of Applied Corporate Finance, Vol. 24, Issue 3, pp. 8-18, 2012