For weekend reading, Louis Navellier offers the following commentary:

This week marked the 60th anniversary of Dr. Martin Luther King’s “I Have a Dream” speech, delivered in Washington, DC. I remember it well. It was a Wednesday. It also marked the first day I set foot on my college campus. Dr. King’s speech was inspiring to me, delivered from the heart, and it marked the start of a major, long-overdue reform in civil rights.

On a less personal but equally overdue challenge, we need to address the runaway deficit spending that could bankrupt our nation, but nobody seems to be willing to start the dialogue. Politicians aren’t ready to promise less pork to the people. It’s a job for a money man.

Jerome Powell’s Statements From The Jackson Hole

Jerome Powell’s term lasts almost three more years, until May of 2026. By then, the 2024 election will be long gone. Powell has already seen enough politics to last a lifetime, so he may be ready to tell the truth by 2025. At Jackson Hole this year, Powell delivered 2,046 words, but if he took some truth serum and spoke from his heart, he might deliver a 2025 valedictory address of only one-third that length, like this:

“My fellow central bankers, investors, and all politicians with an ear to hear, I will not seek, neither will I accept, another term as your Federal Reserve Chairman next year. It has been a very educational eight years, which – like our Presidents – should mark the term limit for Fed Chairs. I have learned from my many mistakes, but it’s time for someone else to learn from their own mistakes.

Before I share what’s most on my mind today, let me look in the mirror and admit my own mistakes. Most recently, I and my colleagues helped cause high inflation by printing too much electronic money in late 2020 and 2021; then we mislabeled that high inflation as ‘transitory’ for nearly all of the remainder of 2021.

Then, we waited too long to end Quantitative Easing (QE) while failing to raise rates above their unsustainable zero-level until April of 2022. Then we raised them too far, too fast, at the fastest rate in history, to well above 5%.

“I could spend the rest of my allotted time going over our other past mistakes, but it’s time to look at what the Fed can and cannot do. We have been assigned two mandates – low inflation and low unemployment rates. Some want us to add a third mandate – lower global temperatures, but I made it clear in early 2023 that we will not add a third mandate as ‘climate controller.’

In fact, I would also question our initial two mandates, which are based on the outdated and disproved “Phillips Curve,” concerning the alleged trade-off between inflation and employment. We have no control over the job market, nor can we force those who won’t work to accept jobs when politicians pay them more to remain idle.

I would simply revert to our two founding mandates – (1) to keep the U.S. dollar reliable and strong through slow money creation tied to population and economic growth, and (2) to supervise bank stability through our 12 Fed Districts.

“The part of my job I will miss the least is appearing before Congressional committees way too often and there to be lectured by spendthrift blowhards on how we should manage the nation’s money, or to be told that we are not doing enough to create new jobs in their district. How long will these elected officials fail to do their Constitutional duty and then put someone else in the proverbial ‘hot seat’ to take the blame?

“As a central banker, we can raise or lower short-term interest rates, or add to our balance sheet, but we cannot do what our frequent Inquisitors in Congress keep demanding of us in their open hearings – tasks which are really their mandate, not ours. We cannot stop the profligate spending of the President and the majority of Congress. We cannot address fiscal policy – spending – we can only address monetary policy.

“We are nearing the point of no return in our national debt, at $35 trillion and growing by $2 trillion per year in times of relative peace and prosperity, which is unprecedented in our history. We have abandoned all caution in spending for at least 25 years ago, after 9/11. Few politicians of either major party take this threat seriously. At an average 5.7% interest, we are spending $2 trillion a year on debt service alone.

“For a way to put our budget where my mouth is, I volunteer to cut our central bank payroll by 90%, including any future pay, severance package, benefits, or pension I may have earned. We don’t need 400 PhD economists to keep turning out failed forecasts based on our faulty Keynesian template.

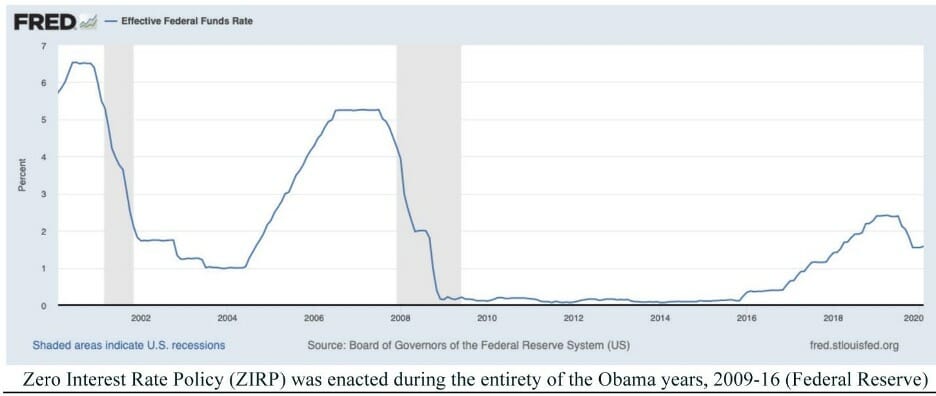

We don’t need to offer any future President ‘training wheels’ of zero-percent interest rates for eight years, as my predecessors did for President Obama, on the theory that the greatest economy in the history of the world was too fragile to recover from the 2008 financial crisis by returning to normal monetary policies. We don’t need committees and economic models to figure out how much money we need to match population and GDP growth. As Milton Friedman said years ago, we could be replaced by a few good algorithms.

“So, I’ve thrown down the gauntlet for you, Mr. President and Congress. I’m willing to cut 90% of our personnel and serve without pay or benefits. Who will follow me – to return our nation to fiscal sanity?”

What Powell Actually Said on August 25, 2023

Please realize that everything above was my imagination of a truth-serum “dream speech,” not reality.

Here’s how Mr. Powell actually concluded his Jackson Hole talk last Friday – through a glass darkly.

“As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical. At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We need price stability to achieve a sustained period of strong labor market conditions that benefit all. We will keep at it until the job is done.”

The debt data is not so cloudy, sir, unless you’re a man speaking in code…Maybe two years from now, you will take that truth serum and deliver a dream speech for the ages. We can always hope for miracles.