10 new stocks make our Safest Dividend Yield Model Portfolio this month. January’s Safest Dividend Yield Model Portfolio was made available to members on 1/20/17.

Recap from December’s Picks

Our Safest Dividend Yield Model Portfolio (+2.0%) outperformed the S&P 500 (+0.6%) last month. The best performing stocks in the portfolio were large cap stock China Mobile Limited (CHL) which was up 7%, and small cap stock, Costamare Inc. (CMRE), which was up 7%. Overall, 13 out of the 20 Safest Dividend Yield stocks outperformed the S&P in December.

The success of the Safest Dividend Yield Model Portfolio highlights the value of our forensic accounting (featured in Barron’s). Companies with strong free cash flow provide higher quality and safer dividend yields because we know they have the cash to support the dividend. By analyzing footnotes in SEC filings, we are able to calculate cash flow more accurately and diligently for 3000+ companies under coverage.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating, have positive free cash flow and economic earnings, and offer a dividend yield greater than 3%. We think this combination provides a uniquely well-screened group of stocks that can deliver returns greater than the market.

Highway Holdings (HIHO), metal and plastic OEM parts manufacturer, is one of the additions to our Safest Dividend Yield Model Portfolio in January.

Since 2012, Highway Holdings has grown after-tax profit (NOPAT) by over 50% compounded annually while NOPAT margins have improved from 1% in 2012 to 6% in 2016, per Figure 1. Highway Holdings’ return on invested capital (ROIC) has improved from 2% in 2012 to a top-quintile 17% in 2016. Such strong fundamentals and an 11% dividend yield earn HIHO a spot on this month’s Safest Dividend Yields Model Portfolio.

Figure 1: Highway Holdings’ Improving Profitability

Sources: New Constructs, LLC and company filings

Free Cash Flow Supports Dividend Payments

Highway Holdings has increased its dividend payment from $0.03/quarter in 2012 to $0.10/quarter in 2016, per Figure 2. The increase in dividend payment has been facilitated by HIHO’s positive free cash flow (FCF). Over the past five years, Highway Holdings has generated a cumulative $8 million in FCF (62% of market cap). Companies with strong free cash flow provide higher quality dividend yields because we know the firm has the cash to support its dividend. On the flip side, dividend yields from companies with low or negative free cash flow cannot be trusted as much because the company may not be able to sustain such a high dividend for much longer.

Figure 2: Increasing Dividend Payment Since 2012

Sources: New Constructs, LLC and company filings

Despite Strong Fundamentals, HIHO Remains Undervalued

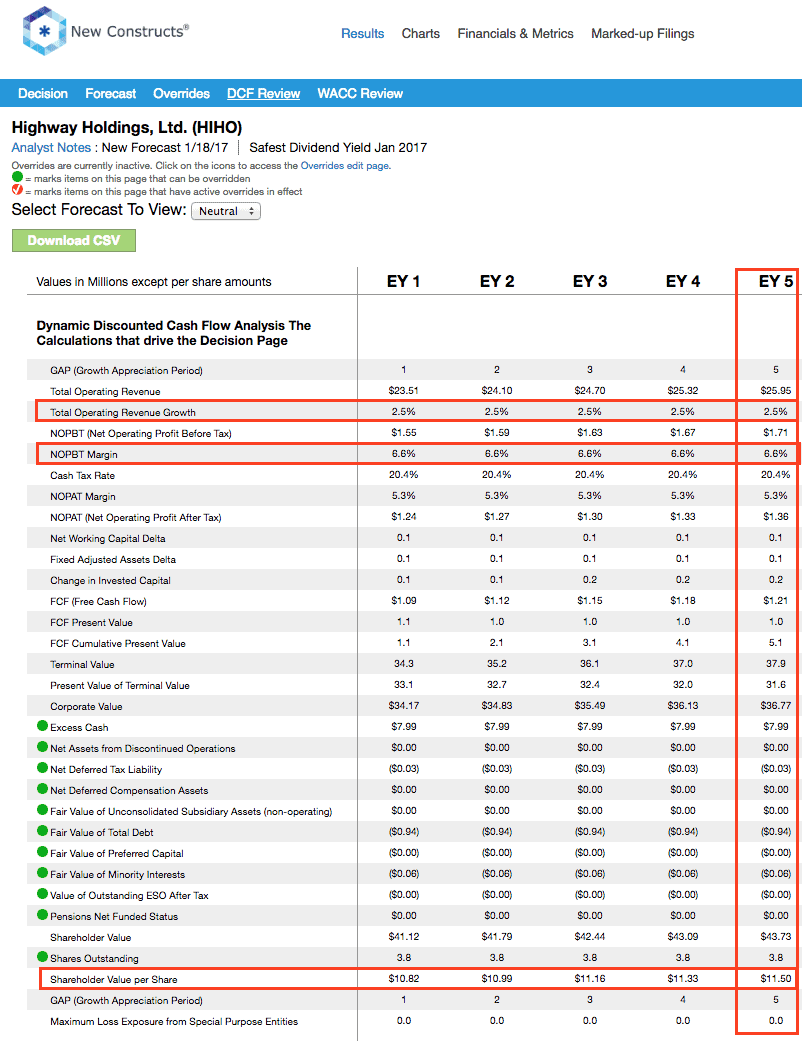

Despite Highway Holdings’ share price increasing nearly 30% over the past five years, shares remain undervalued. At its current price of $4/share, HIHO has a price-to-economic book value (PEBV) ratio of 0.3. This ratio means the market expects HIHO’s NOPAT to permanently decline by 70% from current levels. Such expectations seem overly pessimistic for a firm that has grown NOPAT by 17% compounded annually since 2003.

However, if Highway Holdings can grow NOPAT by just 1% compounded annually for the next five years, the stock is worth $12/share today – a 300% upside. Such upside potential coupled with HIHO’s 11% dividend yield provide investors a great low risk/high reward opportunity.

Impacts of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Highway Holdings’ 2016 10-K:

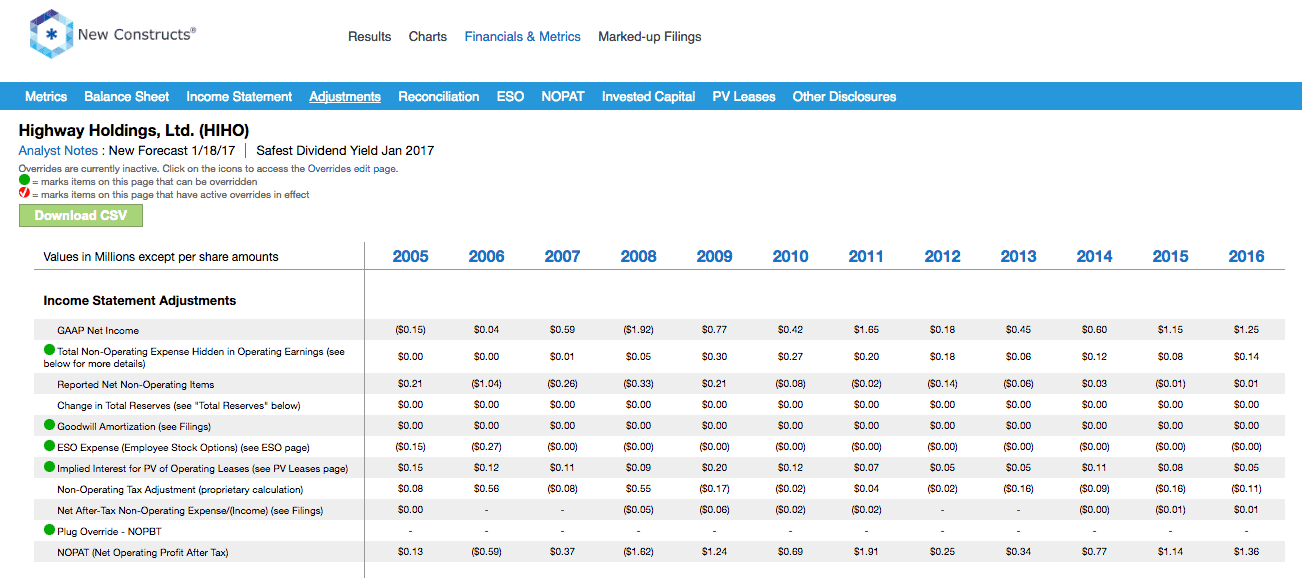

Income Statement: we made less than $2 million of adjustments with a net effect of removing less than $1 million in non-operating expense (<1% of revenue). We removed <$1 million related to non-operating expenses and <$1 million related to non-operating income. See all adjustments made to HIHO’s income statement here.

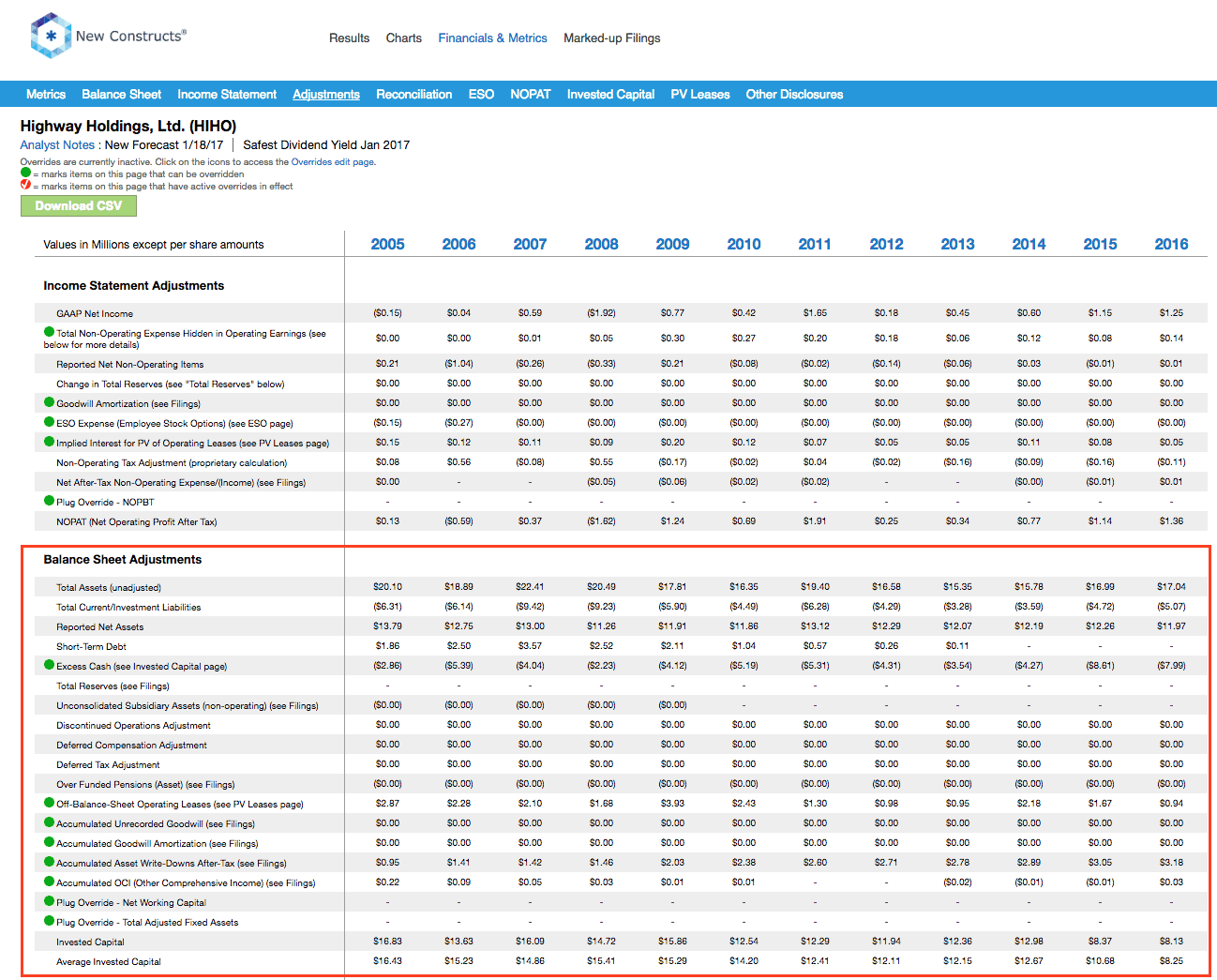

Balance Sheet: we made $12 million of adjustments to calculate invested capital with a net increase of $4 million. The most notable adjustment was $3 million (27% of reported net assets) related to asset write-downs. See all adjustments to HIHO’s balance sheet here.

Valuation: we made $9 million of adjustments with a net effect of increasing shareholder value by $7 million. The largest adjustment to shareholder value was $8 million in excess cash. This adjustment represents 62% of HIHO’s market value.

This article originally published here on January 26, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kyle Martone receive no compensation to write about any specific stock, style, or theme.

Article by Kyle Guske II, New Constructs

{kind=link}

{kind=link}

{kind=link}