Hedge funds successfully traded their way around an overwhelming month in April and were up 0.56% while underlying markets as represented by the MSCI World Index gained 1.18% during the month. Investors’ risk appetite improved in April amid waning concerns over trade war, bolstered by the ‘soft’ tone of Xi Jinping in response to US trade sanctions. Developed markets outperformed their emerging market counterparts during the month, as the latter still remained rather volatile with the region’s equity markets posting a slightly negative return during the month on the back of a strengthening US dollar and concerns over US-China trade spat. Equity markets rebounded in April with strength led by European and North American markets with mixed to flat performance across Asian equity markets. Economic data for Q1 2018 was largely encouraging albeit recovery was at a slower pace with indicators pointing towards global economic expansion. Meanwhile 60% of the underlying constituent funds for the Eurekahedge Hedge Fund Index were in positive territory during the month, with nearly 4% of them reporting gains in excess of 5%. European hedge funds led performance among regional mandates this month, up 1.14% while distressed debt managers topped the table across strategies, gaining 1.24% over the same period.

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

On a year-to-date basis, hedge funds were up 0.24% while underlying markets declined 1.08%. Eastern Europe & Russia hedge fund managers led the table on a year-to-date basis, up 5.41% followed by their Latin American and emerging markets counterparts with gains of 4.27% and 1.45% respectively.

Below are the key highlights for the month of April 2018:

- Hedge funds gained 0.56% in April with underlying markets, as represented by the MSCI AC World Index (Local) up 1.18% over the same period. On a year-to-date basis, managers gained 0.24% with 10% of them posting returns in excess of 5%.

- European hedge fund managers led the performance among developed mandates, gaining 1.14% during the month followed by North American hedge funds which were up 0.27% while Japanese hedge funds languished, down 0.63% over the same period. On a year-to-date basis, European hedge fund managers were up 0.85% beating their North American and Japanese counterparts who lost 0.71% and 2.20% respectively.

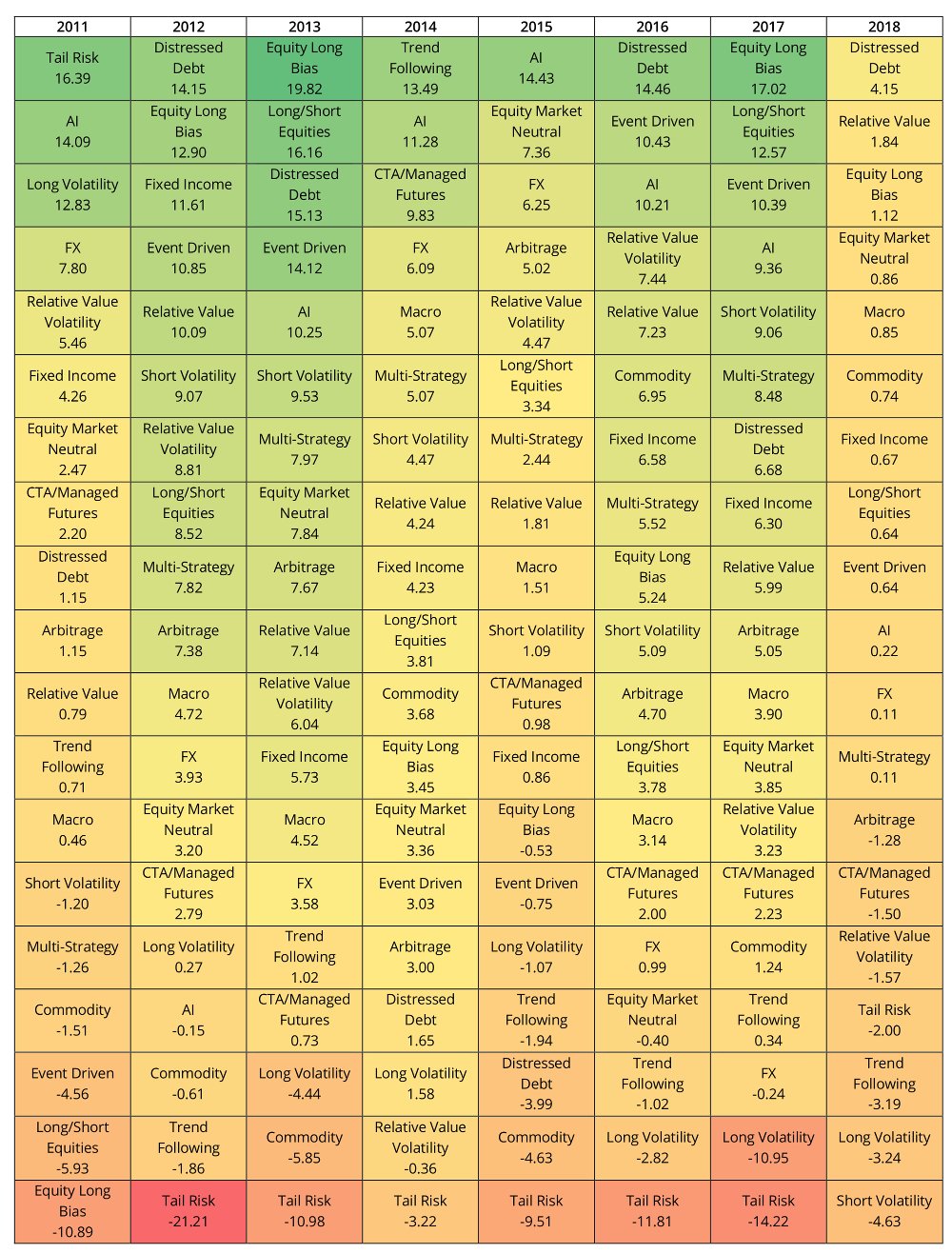

- All strategic mandates were up this month with the Eurekahedge Distressed Debt Hedge Fund Index posting the best returns, up 1.24% during the month – the only strategy to post four consecutive month of gains since the start of the year. Managers also posted impressive April 2018 year-to-date gains, up 4.15% – the best April year-to-date returns for the strategy since 2013.

- CTA/managed futures hedge fund managers gained 0.25% in April with underlying commodity focused hedge funds gaining 1.60% during the month. On a year-to-date basis, CTA/managed futures hedge fund managers declined 1.50% with trend following-focused hedge funds retracting 3.19% while commodity focused funds are up 0.74%.

- Asian hedge funds posted their third consecutive month of losses in April, down 0.27%. On a year-to-date basis, Asian managers are down 0.19%, with weaknesses led by Japan and India mandated hedge funds losing 2.20% and 2.02% respectively.

- The Eurekahedge Crypto-Currency Hedge Fund Index rebounded to positive territory in April with gains of 83.86%, while its 2018 year-to-date figure is still in the red, down 1.22%. In contrast, bitcoin has lost over 33% over the same year-to-date period.

| Main Indices | April 20181 | Last 3 Months | 2018 Returns | 2017 Returns | Annualised Returns | Constituents | Weighting |

| Eurekahedge Hedge Fund Index | 0.56 | -1.74 | 0.24 | 8.37 | 8.73% | 2,693 | Equal |

| Eurekahedge 50 | 0.77 | -0.38 | 1.72 | 6.96 | 5.58% | 50 | Equal |

| Eurekahedge North American Hedge Fund Index | 0.27 | -2.15 | -0.71 | 7.86 | 9.34% | 601 | Equal |

| Eurekahedge European Hedge Fund Index | 1.14 | -0.48 | 0.85 | 7.09 | 7.17% | 294 | Equal |

| Index of the Month | April 20181 | Last 3 Months | 2018 Returns | 2017 Returns | Annualised Returns | Constituents | Weighting |

| CBOE Short Volatility Hedge Fund Index | 3.60 | -2.48 | -4.63 | 9.06 | 8.18% | 13 | Equal |

Main Indices

| Eurekahedge Main Indices | April 20181 | 2018 Returns | 2017 Returns |

| Eurekahedge Hedge Fund Index | 0.56 | 0.24 | 8.37 |

| Eurekahedge Fund of Funds Index | 0.56 | 0.60 | 7.19 |

| Eurekahedge Long-only Absolute Return Fund Index | 0.90 | 0.59 | 21.04 |

| Eurekahedge Islamic Fund Index | 0.39 | 0.48 | 6.47 |

Regional Indices

Performance was a mixed bag across regional mandates with European hedge funds in the lead this month, gaining 1.14% as equity performance in the market showed fair strength, with European equities posting a relief rally at the outcome of ECB’s recent meeting to change its monetary policy in a more gradual pace. The CAC Index ended the month up 6.84% and the DAX Index was up 4.26% over the same period. Asia ex-Japan mandates also bounced back in positive territory, up 0.32% during the month. Chinese equity markets came under pressure in April as tech firms in the mainland faced pressure amid the ZTE ban imposed by US earlier in the month with the CSI 300 Index down 3.63% and down 6.80% year-to-date. Moreover, economic indicators coming out of China indicate that growth in the economy was staying steady and in line with expectations. Over in North America, risk appetite improved as US-China trade sanctions eased somewhat during the month. US treasury yields edged up higher backed by solid corporate Q1 earnings coupled with reduced trade worries and higher US inflation numbers. This has lifted US dollar to a record high since the start of the year and supported gains in US equities with the NYSE Composite and S&P 500 up 0.51% and 0.27% respectively. The Eurekahedge North America Hedge Fund Index was up 0.27% in April, with underlying equity long/short strategies being positive contributors with gains of 0.96%. On the other hand, political uncertainty plaguing the Latin American region particularly in Brazil, led to considerable losses during the month – breaking its three consecutive month of gains since the start of the year. Despite these concerns, the region’s equity markets were in the green during the month with the Ibovespa Index up 0.88% in April. Mexico’s equity markets also gained 4.84% over the same period. The Eurekahedge Latin American Hedge Fund Index declined 0.71% in April. Japanese hedge fund managers also languished into negative territory during the month, down 0.63% despite a pickup in USD sentiment led to weaker yen which lent some support to underlying equity markets with the Nikkei 225 Index up 4.72%.

On a year-to-date basis, Eastern Europe and Russian managers topped the tables and were up 5.41%, followed by Latin American and emerging markets hedge fund managers with gains of 4.27% and 1.45% respectively. Asia ex-Japan and European hedge fund managers were also up year-to-date gaining 0.85% each while Japanese and North American managers languished into negative territory year-to-date, down of 2.20% and 0.71% respectively.

| Eurekahedge Regional Indices | April 20181 | 2018 Returns | 2017 Returns |

| Eurekahedge North American Hedge Fund Index | 0.27 | -0.71 | 7.86 |

| Eurekahedge European Hedge Fund Index | 1.14 | 0.85 | 7.09 |

| Eurekahedge Eastern Europe & Russia Hedge Fund Index | 0.56 | 5.41 | 10.56 |

| Eurekahedge Japan Hedge Fund Index | -0.63 | -2.20 | 13.11 |

| Eurekahedge Emerging Markets Hedge Fund Index | -0.54 | 1.45 | 16.71 |

| Eurekahedge Asia ex Japan Hedge Fund Index | 0.32 | 0.85 | 20.66 |

| Eurekahedge Latin American Hedge Fund Index | -0.71 | 4.27 | 13.51 |

Strategy Indices

All strategic mandates ended the month in positive territory with distressed debt managers leading the pack up 1.24% with the help from a strong showing in the US and European high yield sector during the month. Macro hedge fund managers gained 0.97%, and some macro funds with short exposure into the yen reaping gains during the month as higher US interest rates saw the yen weaken relative to US dollar. Long/short equities managers also rebounded in April and were up 0.69% as average fund performance across the globe was largely positive amid reduced trade war concerns. Strength in equity market performance was led by European and North American markets with mixed to flat performance across Asian equity markets. Event driven managers gained 0.66% in April, as managers with exposure into Europe posted good gains during the month with deal activity within the telecommunication services (supported by M&A activity) and energy space among performance contributors. Relative value hedge funds also posted good gains during the month and were up 0.45% with performance led by underlying relative value volatility strategy (+1.12%). Among volatility-focused hedge funds, short volatility hedge fund managers topped the tables with gains of 3.60% in April whereas long volatility hedge fund managers posted the steepest decline, down 2.63% as volatility levels represented by the CBOE VIX Index fell during the month after its unstoppable uptrend since the start of the year.

CTA/managed futures hedge funds were up 0.25% in April with underlying trend following-focused hedge funds leading much of the weakness, down a modest 0.09% as trading conditions in currencies and metals were rather choppy. The greenback gained ground during the month with the US Dollar Index up 2.08% as 10 year yields hit the psychologically important 3% mark. Managers reported losses on short USD positions against the basket of emerging currencies. The short USD position against GBP was the biggest performance detractor to most managers as the sterling weakened during the month amid weaker than expected economic data, casting some doubts over the probability of interest rate hike by the BOE in May. Long exposure into precious metals was also among performance detractors for CTA/managed futures funds as the rebound in US dollar led precious metals, particularly gold, to trade lower during the course of the month. On the contrary, long exposure to energy remained to be profitable for managers. Oil prices climbed above US$74 a barrel amid robust demand and OPEC production cuts. However, the expectations of sanctions against Iran, triggered by President Trump’s threats to withdraw from the Iran nuclear deal. The rise came on the back of increasing expectations of sanctions against Iran, triggered by President Trump’s threats to withdraw from the Iran nuclear deal. The rise came on the back of increasing expectations of sanctions against Iran, triggered by President Trump’s threats to withdraw from the Iran nuclear deal. The rise came on the back of increasing expectations of sanctions against Iran, triggered by President Trump’s threats to withdraw from the Iran nuclear deal affected much of the outlook on the oil industry. Managers also posted gains on long exposure into base metals, particularly in aluminium as it rallied sharply during the month backed by the US new sanctions on Russian metals producer which led to supply concerns. Arbitrage and multi-strategy hedge funds followed next gaining 0.19% and 0.17%. Fixed income mandated hedge funds posted a modest gain of 0.09% during the month, with gains realised from long exposure into German and US fixed income instruments which traded higher during the month.

On a year-to-date basis, distressed debt hedge fund managers were up 4.15% followed by relative value hedge fund managers which gained 1.84%. Macro and fixed income managers were also up 0.85% and 0.67% respectively, followed by long/short equities and event driven managers which trail closely behind, up 0.64% each over the same period. On the other hand, CTA/managed futures hedge fund managers were down 1.50% with weakness lead by underlying trend-following-focused strategies, declining 3.19% year-to-date.

Table 1: Index Flash Strategy Return Map

| Eurekahedge Strategy Indices | April 20181 | 2018 Returns | 2017 Returns |

| Eurekahedge Arbitrage Hedge Fund Index | 0.19 | -1.28 | 5.05 |

| Eurekahedge CTA/Managed Futures Hedge Fund Index | 0.25 | -1.50 | 2.23 |

| Eurekahedge Distressed Debt Hedge Fund Index | 1.24 | 4.15 | 6.68 |

| Eurekahedge Event Driven Hedge Fund Index | 0.66 | 0.64 | 10.39 |

| Eurekahedge Fixed Income Hedge Fund Index | 0.09 | 0.67 | 6.30 |

| Eurekahedge Long Short Equities Hedge Fund Index | 0.69 | 0.64 | 12.57 |

| Eurekahedge Macro Hedge Fund Index | 0.97 | 0.85 | 3.90 |

| Eurekahedge Multi-Strategy Hedge Fund Index | 0.17 | 0.11 | 8.48 |

| Eurekahedge Relative Value Hedge Fund Index | 0.45 | 1.84 | 5.99 |

| CBOE Eurekahedge Long Volatility Hedge Fund Index | -2.63 | -3.24 | -10.95 |

| CBOE Eurekahedge Relative Value Volatility Hedge Fund Index | 1.12 | -1.57 | 3.23 |

| CBOE Eurekahedge Short Volatility Hedge Fund Index | 3.60 | -4.63 | 9.06 |

| CBOE Eurekahedge Tail Risk Hedge Fund Index | -1.19 | -2.00 | -14.22 |

| Eurekahedge Equity Long Bias Hedge Fund Index | 1.11 | 1.12 | 17.02 |

| Eurekahedge Equity Market Neutral Hedge Fund Index | -0.08 | 0.86 | 3.85 |

| Eurekahedge Trend Following Index | -0.09 | -3.19 | 0.34 |

| Eurekahedge FX Hedge Fund Index | 0.47 | 0.11 | -0.24 |

| Eurekahedge Commodity Hedge Fund Index | 1.60 | 0.74 | 1.24 |

| Eurekahedge Global Hedge Fund Indices by Fund Size | April 20181 | 2018 Returns | 2017 Returns |

| Eurekahedge Small Hedge Fund Index (< US$100m) | 0.41 | -0.25 | 8.60 |

| Eurekahedge Medium Hedge Fund Index (US$100m – US$500m) | 0.63 | 1.02 | 8.43 |

| Eurekahedge Large Hedge Fund Index (> US$500m) | 0.82 | 0.48 | 6.43 |

| Eurekahedge Billion Dollar Hedge Fund Index | 0.85 | 0.09 | 5.88 |

| Mizuho-Eurekahedge Indices | April 20181 | 2018 Returns | 2017 Returns |

| Mizuho-Eurekahedge Index – USD | -0.44 | -0.17 | 8.69 |

| Mizuho-Eurekahedge TOP 100 Index – USD | -0.58 | -0.44 | 6.76 |

| Mizuho-Eurekahedge TOP 300 Index – USD | -0.44 | -0.31 | 7.75 |

| Asia-Eurekahedge Indices | April 20181 | 2018 Returns | 2017 Returns |

| Eurekahedge Greater China Hedge Fund Index | -2.12 | -0.18 | 29.61 |

| Eurekahedge India Hedge Fund Index | 1.73 | -2.02 | 28.96 |

1 Based on 25.21% of funds which have reported April 2018 returns as at 8 May 2018

Article by Eurekahedge

{kind=link}