Fund Structure

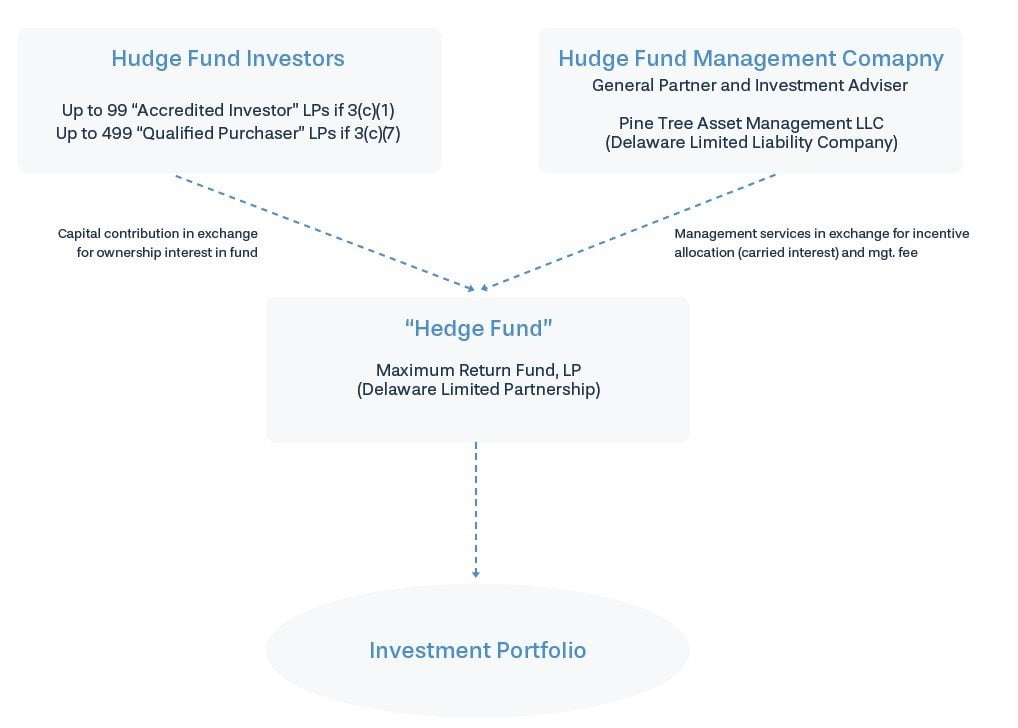

The traditional hedge fund structure for most US-based domestic funds is depicted below. The structure consists of a management company (typically a limited liability corporation, but can also be a limited partnership or S corporation) and a hedge fund (typically a limited partnership, with the management company as general partner and the investors as limited partners).

Q3 hedge fund letters, conference, scoops etc

This structure and entity types are chosen to limit tax and legal liability for the fund’s managers and investors. The owners and any employees or seed investors who receive equity have a stake in the management company, which in turn has a stake in the hedge fund.

Since hedge fund managers are selling ownership interests in the hedge fund (securities) they would typically be required to register the offering with the Securities and Exchange Commission (SEC) and be considered an “investment company” (mutual fund), placing an undue compliance burden on the fund. However, they are exempted from this requirement if they meet certain qualifications under SEC Regulation D Rule 506:

1. No public offering of securities

- This means that no advertising or general solicitation may be made

- Articles, interviews, internet websites and listing in hedge-fund databases may violate this requirement (hence the reason hedge funds are notoriously private)

- As a rule of thumb, the fund should only raise capital from those with whom the management company or its agents have a pre-existing business or personal relationship

2. Limits on the number of investors in the fund

- There are two different rules under which funds can qualify for this exemption:

- Section 3(c)(1) Funds are limited to 99 “accredited investors” (>$1 million in assets or >$250,000 in income)

- Section 3(c)(7) Funds are limited to 499 “qualified purchasers” (>$5 million in liquid net worth)

- There are additional nuances to these limits which a qualified legal professional should advise

3. Must file Form D with the SEC within 15 days of the first sale of securities

Hedge fund management companies may be required to register as an “investment advisor” with the SEC or with state regulatory bodies depending on the state and the fund’s “assets under management.” Additionally, it might make sense to adopt a more complex fund structure with more than one management company and/or an offshore fund structure for tax exempt US-based investors and international investors. These increase legal and adminstrative complexity. We recommend consulting a hedge fund lawyer or reading a more thorough consideration of these matters from our legal references.

As technology has brought down administrative costs, it has become more common for smaller funds to manage separately managed accounts. In this structure, the manager directly manages the client’s money in their account, avoiding the complications of pooling the money in one account. Leigh Drogen of Estimize has written on why this structure may be preferable to the traditional limited partnership model. Smaller funds may manage separately managed accounts in addition to funds in the limited partnership structure.

Our advice for a startup fund is to keep the fund structure as simple as possible and stick to the established industry norms. This will typically simplify the process of marketing the fund to raise capital and reduce legal costs.

Fees

The fee structure for hedge funds and similar alternative asset managers have traditionally followed a “two and twenty” model, with two percent of fund assets being paid to the management company to cover the expenses of running the fund and 20% of profits being paid as an incentive to earn higher returns. However, in recent years as the alternative asset management has become more competitive that fee structure has come under attack. 70+% of funds have retained the 20% incentive fee, but the majority of funds now charge less than 2% as a management fee according to Preqin.

Expect to charge somewhere between 1.5-2% of AUM. Unfortunately, since hedge funds tend to have high fixed costs but can have relatively low variable costs as fund size scales, this model is not advantageous for startup funds. The management fees are typically not enough to cover costs in the early stages, leaving a significant working capital need for startup funds. Emerging managers often cover this by not taking a salary, raising seed money from investors in exchange for an equity stake in the management company, and running a lean operation to cut costs.

The 20% incentive fee is actually not a fee but a profit allocation in the form of increased ownership in the fund, also known as carried interest. It is structured that way to avoid being taxed as income. Instead the allocation is taxed as a capital gain when redeemed.

Access the full whitepaper by Sentieo on Quick Tips For Starting A Hedge Fund here.

{kind=link}